Former Coinbase CPO’s 10,000-Word Essay: In This Market, the Greatest Advantage Is “Doing Nothing”

Original Compilation: Jiahuan, ChainCatcher

I still believe in cryptocurrency and am optimistic about the direction of this industry. As I write these words, I am not someone who has lost everything, sworn off risk, and returned from a Vipassana retreat with newfound insights. I hold cryptocurrency, stocks, and some alternative assets like real estate and gold. And I’m happy with my holdings.

Having been in this space long enough, I know what I believe in and where I’ve deceived myself. The biggest lie is that better judgment can save me from poor behavior. After a decade in this industry (including recent work at Coinbase and earlier in venture capital), the most honest thing I can say after all this is: In any market—whether it’s crypto, stocks, or anything else—the biggest advantage most people can have is the willingness to do nothing.

For most people, the real risk isn’t ignorance; it’s restlessness. It’s the inability to sit still with a perfectly good position once the market starts waving something shinier and louder. It’s the desperate craving for more dopamine. That’s the core of this entire piece.

The Same Regret

If you’ve been in the market long enough, you’ll hear the same phrase repeated in slightly different forms: If only I had just held on.

Not if I had found the next perfect trade. Not if I had rotated faster. Not if I had discovered the 10x coin before everyone else. Just: if I had simply left that good thing alone. The crypto version of this regret is: selling Bitcoin to chase altcoins. The stock version is: selling Nvidia to trade doomsday call options because you suddenly thought you were a volatility expert this Tuesday. Different markets. Same regret.

This isn’t a story about me blowing myself up. I’m doing fine. But I’ve watched many smart people slowly destroy quite substantial wealth simply because they couldn’t stand the quiet. And the entire suite of products they used—from crypto exchanges to prediction markets to stock trading apps—was built around this human weakness.

If you’ve ever compulsively checked your portfolio, panic-sold on a dip, or made a trade just because you were bored on a Tuesday afternoon, this is for you.

I Entered Crypto Through the Wrong Door

In 2015, as a college freshman, I entered the crypto space and immediately fell in love with what now seems the most embarrassing part: enterprise blockchain. Private chains. Enterprise consortia. “Distributed Ledger Technology.” The entire PowerPoint industrial complex selling “serious applications.” I thought that was the real deal, and “magic internet money” was just libertarian and speculator sideshow.

I know, it’s embarrassing in hindsight. I even interned at IBM doing blockchain research, which felt like the ultimate validation at the time. The world’s premier tech giant was patting me on the head saying: yes, this is how adults play, you’re being smart.

The longer I stayed in the space, the more lifeless most of those projects felt. Many enterprise blockchains were just better-packaged databases. Meanwhile, Bitcoin (the largest digital asset) kept creeping into the mainstream, and Ethereum (a platform allowing developers to build financial apps not controlled by any company) kept attracting builders. Open systems have real pull. People show up, uninvited, in droves. It’s a bit embarrassing, mainly because it meant the “weirdos” were right.

Eventually, I dropped out in my junior year and moved to San Francisco during the early days of DeFi (short for decentralized finance, a wave of apps trying to rebuild banking and trading without banks). I was fortunate to work at a great YC-backed startup, getting deeper into the industry’s machinery: founders, funds, trading firms, DeFi apps, and everything. I ended up leading VC investments and joined a proprietary trading firm as a founding team member during the pandemic.

This cured me of the naive belief that most market participants were rational. They aren’t. Neither was I. Cycle after cycle.

Nobody Knew What They Were Buying

The early years of crypto were, charitably, “bizarre.” Sure, there were smart people around. Libertarians. College dropouts. Anonymous developers. Teenagers somehow making more than professors. In Telegram groups, people four months into the space were dispensing garbage advice packaged as insight. At conferences, people who got in a year before you were visibly rich, making you feel one trade away from changing your class.

I bought Bitcoin. I bought ETH. I had real reasons for both.

Then the ICO craze hit, and many of us got dumber. For those lucky enough to miss that era, an ICO was basically an IPO with almost no regulation and even more gibberish. Back then, almost anything could become a token. A website, a PDF whitepaper, a few grandiose statements about reinventing some massive industry, and suddenly you were doing a public offering.

It was easy to confuse splashy ambition with actual value. Like a Kickstarter campaign that was 90% vibes and 10% product, but with a money printer attached.

This video gives a more detailed timeline of when and where these companies got investment:YouTube Link

So yes, I bought Cardano because it was pitched as the academic Ethereum. I bought SpankChain because someone sold me on adult payments being a huge but broken market and this token being its payment layer. It did not, readers. I bought IOTA, and to this day, I couldn’t explain to you what it was even if you held a gun to my head. In 2017, this was normal behavior. That’s the point. This wasn’t fringe stupidity; it was mainstream crypto stupidity.

The infrastructure was also incredibly janky: Bitfinex, Bittrex, Poloniex, EtherDelta. Each felt like it could be hacked, freeze withdrawals, get sued by the SEC, disappear overnight, or sometimes all three. It was held together by duct tape and optimism, but as long as the market was going up, it felt survivable.

And most of us had no idea what we were buying.

The most common mental error was also the dumbest: People confused “low unit price” with “cheap.” A three-cent token “felt cheap,” just like a penny stock on Robinhood felt cheap. Next to a $10,000 Bitcoin, it looked like a steal. Almost nobody checked the total token supply in circulation. Almost nobody cared about dilution. Denomination bias did half the work.

Despite the chaos of the ICO era, Ethereum itself turned out to be one of the best generational investments of a lifetime. If you bought ETH in the crowdsale around $0.31 in 2014 and held, at the peak you were up about 15,000x. The irony is that most people in the ecosystem at the time traded themselves out of that kind of wealth chasing tokens that no longer exist. By early 2018, most of those tokens were down 80% to 95%. Turns out SpankChain didn’t disrupt the adult entertainment payments tech stack.

And the Bitcoin I sold to fund these adventures? Still Bitcoin. Still scarce. Still chugging along. The mistake isn’t just painful; it’s particularly insulting. Not because it was some complex, high-level operation that failed, but because it was stupid and entirely avoidable.

Bitcoin’s price chart from 2017 to today proves it. Those who held through every crash are up thousands of percent.

Early DeFi Made Greed Sound Learned

If 2017 was naive speculation, the DeFi Summer of 2020 was sophisticated speculation. It was more dangerous precisely because it felt smart.

DeFi apps offered absurdly high interest rates on deposited funds, sometimes 500% or even 1000% APY, paid not in dollars but in newly printed tokens. That was the “genius” of DeFi Summer. In hindsight, ICOs were slapdash. DeFi felt crisp and innovative. Its jargon was hardcore enough that participating felt like financial engineering, masking what it mostly was: chasing unsustainable yields that evaporated the moment incentives dried up.

- You weren’t gambling. You were “providing liquidity.”

- You weren’t chasing token inflation. You were “participating in protocol growth.”

- You weren’t greedy for absurd returns. You were “putting idle assets to work.”

Here’s a good explainer:CoinGecko Link

Much of what happened during that period was just the same old greed translated into fancier nouns. Then came NFTs. Then new Layer 1 blockchains. Then perpetuals. Then prediction markets. Then memecoins came back again, stripped down to their purest form: noise with a ticker.

In crypto, your counterparty is often: teams who know exactly when tokens unlock, funds that got in at a fraction of your price, and market participants who understand position sizing better than you. The closer you get to professional investors and traders, the more brutal the average retail experience looks.

Most people, whether on Robinhood or Coinbase, are trading with the least information and the most emotion. Narratives fill the information vacuum and get passed to retail as high-conviction bets. “This is the next Solana.” “This is the next Nvidia.” “This coin hasn’t moved yet.” Often, you’re just someone else’s exit liquidity.

Markets Change Clothes, Behavior Doesn’t

People love to act like later cycles got more sophisticated. They didn’t. The packaging got more sophisticated. But the behavior feels familiar.

Pump.fun is a platform on Solana (one of the largest blockchains, think of it as a faster, cheaper alternative to Ethereum) where anyone can create a new, tradable crypto token in seconds. It strips memecoin speculation down to its most efficient form: quick launch, quick trade, quick loss, repeat. It industrialized impulse control disorder and supercharged FOMO.

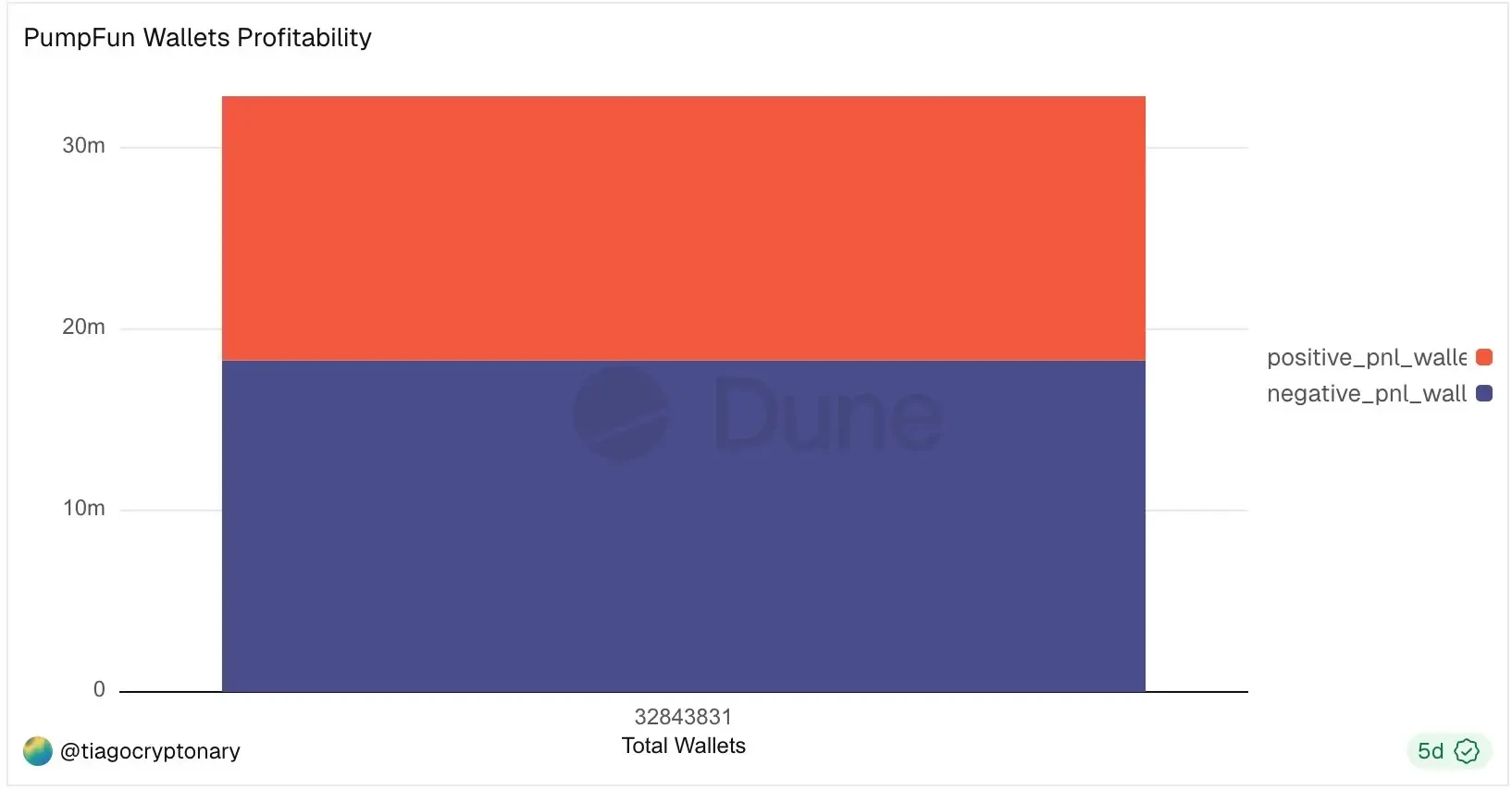

When Pump launched in January 2024, Solana’s native token SOL was trading around $84. According to Dune Analytics, of the roughly 32.8 million wallet addresses on Pump.fun, only about 139,000 (~0.4%) have ever realized over $10,000 in profit. About 55% of traders are purely in the red, and over 90% are either down or up less than $1,000. In 2025, research by Solidus Labs flagged 98% of tokens on the platform as scams or exhibiting fraudulent activity.

Data source:Dune Analytics Link

This next part might make you want to throw your phone into the ocean. If the average participant on Pump.fun had taken the principal they burned on memecoins (even just $500, the most common loss bracket) and simply bought SOL in January 2024 and held it, they could have ridden it from $84 to nearly $295 in January 2025. Doing nothing would have returned roughly 3.5x. Even at today’s price of roughly $84, they’d at least be flat, which is better than being wiped out chasing a token named after a frog with sunglasses.

The ugly truth isn’t that someone wins. Of course someone wins. The ugly part is how concentrated those winnings are and how many people waste time and money chasing upside that doesn’t exist for them. This is back-of-the-envelope, not a precise financial audit. But directionally, for millions of wallets, buying Solana and going outside would have been better.

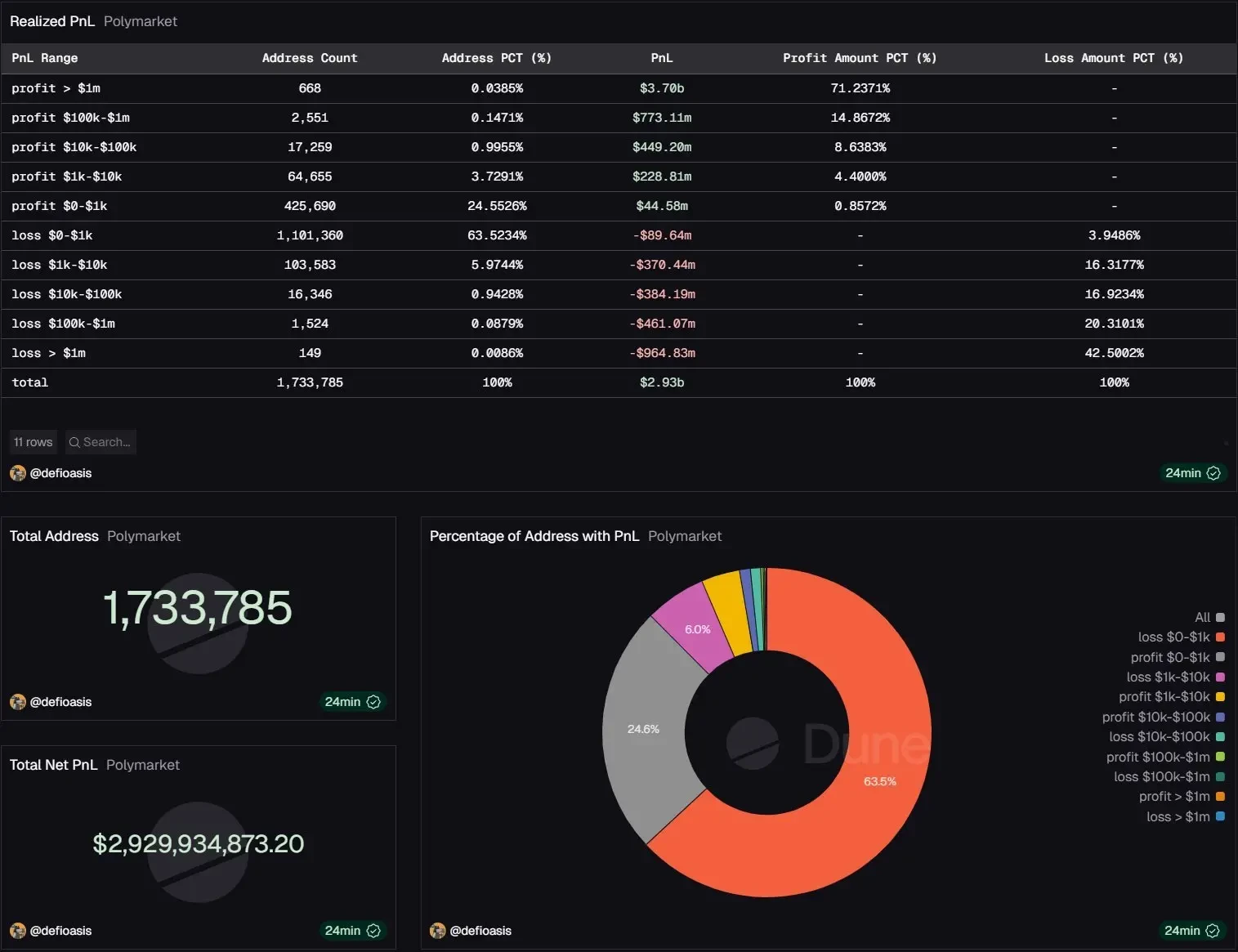

On Polymarket (think of it as a stock market for predicting events, where you buy and sell shares based on your belief about whether a real-world event will happen), roughly 70% of the over 1.7 million addresses are in the red, while less than 0.04% of addresses captured over 70% of all profits on the platform.

I haven’t personally traded on Pump.fun or Polymarket. But I’ve watched people burn quite substantial principal on both. Smart people who genuinely believed they had an edge found themselves as exit liquidity for faster, better-informed players.

I haven’t personally traded on Pump.fun or Polymarket. But I’ve watched people burn quite substantial principal on both. Smart people who genuinely believed they had an edge found themselves as exit liquidity for faster, better-informed players.

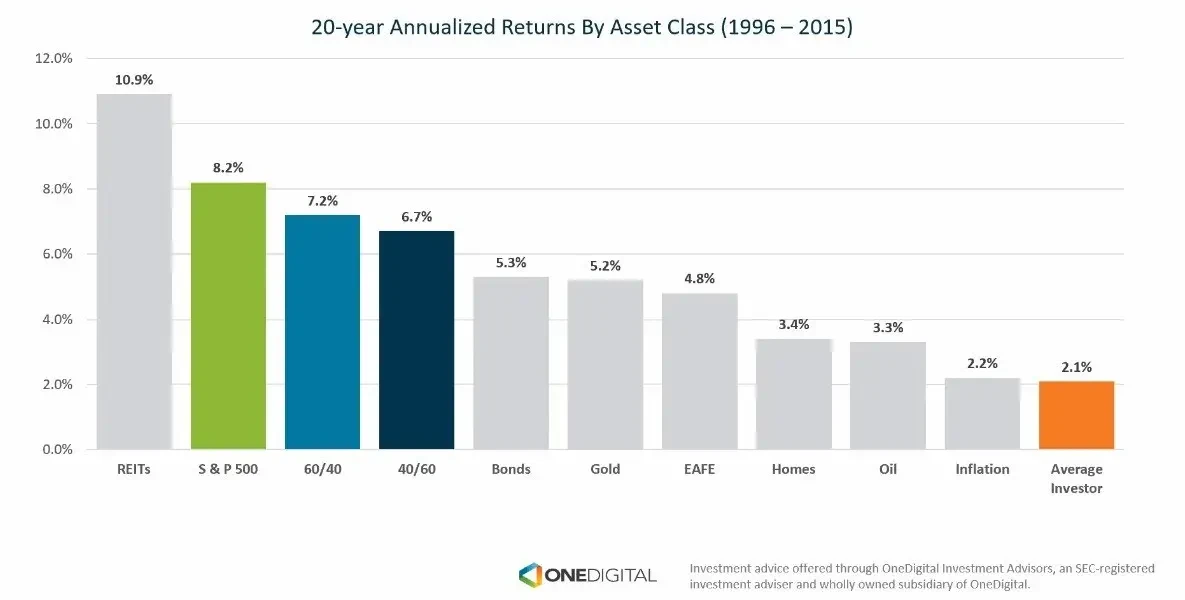

This pattern isn’t unique to crypto. The classic Barber and Odean study found the most active traders underperformed by about 11% annually versus a market return of nearly 18%; but more recent data is equally damning. A 2024 study by Dalbar Inc. found the average retail investor underperformed the S&P 500 by 5.5% in 2023, the third-largest retail performance gap in the past decade, and gaps tend to widen during bull markets as people sell on dips and miss the rebound.

Data source:Crews Bank Link

According to FINRA’s 2025 day trading statistics, 72% of day traders ended the year with a financial loss, only 13% could maintain consistent profitability over six months, and a mere 1% were successful over five years. Bloomberg found 80% of day traders quit within the first two years. If you’ve ever stared at your Robinhood or Fidelity account wondering why you’d have been better off just buying the S&P 500 and forgetting it, this is why.

For leveraged products like options or futures (borrowed money amplifies your bet, small price moves can wipe you out), the data gets uglier. India’s market regulator SEBI reported that 70% to 91% of retail traders who frequently traded derivatives lost money in recent years. This is true anywhere you give the average person a blinking interface and enough jargon to mistake gambling for an edge.

I Watched People Trade Away What Could Have Made Them Rich

In every cycle, I’ve watched the same thing happen. Veterans who survived the last crash slowly trade away the positions that made them wealthy, chasing whatever new narrative the market throws out. Then they quietly disappear. Not from some dramatic blow-up, but from death by a thousand small sector rotations. Then the next wave of retail

This article is sourced from the internet: Former Coinbase CPO’s 10,000-Word Essay: In This Market, the Greatest Advantage Is “Doing Nothing”

Related: Data Modeling: How to Improve the Quality of Polymarket Interactions?

Compiled by|Odaily(@OdailyChina);Translator|Azuma(@azuma_eth) The core message of this article is singular — how to prepare for what could be the largest airdrop in the prediction market sector. The Data Issue That Must Be Stated Before building any model, we need real, reliable data. Polymarket’s trading volume data has been widely misreported. In December 2025, Paradigm published a key research finding: most Polymarket data dashboards calculate volume by summing all “OrderFilled” events. However, this event is triggered on both the maker and taker sides of the same trade, leading to double-counting. The real volume is roughly half of what the dashboards show. Dashboard Volume vs. Single-Sided Volume — the latter is the number that truly matters for airdrop modeling. This is crucial for airdrop modeling. If Polymarket uses volume as a metric,…