OUSD’s “100-Person List” is Actually a “Letter of Intent”? Borrowing Legitimacy Through Name-Dropping Sparks Trust Crisis

On the evening of June 30, Beijing time, the emergence of a new stablecoin once again stirred the landscape of the stablecoin market.

A company named Open Standard announced the launch of a stablecoin called Open USD, featuring free minting and redemption, sharing of reserve asset returns, and joint governance by partners. These open designs directly address pain points in stablecoin distribution and appear highly attractive.

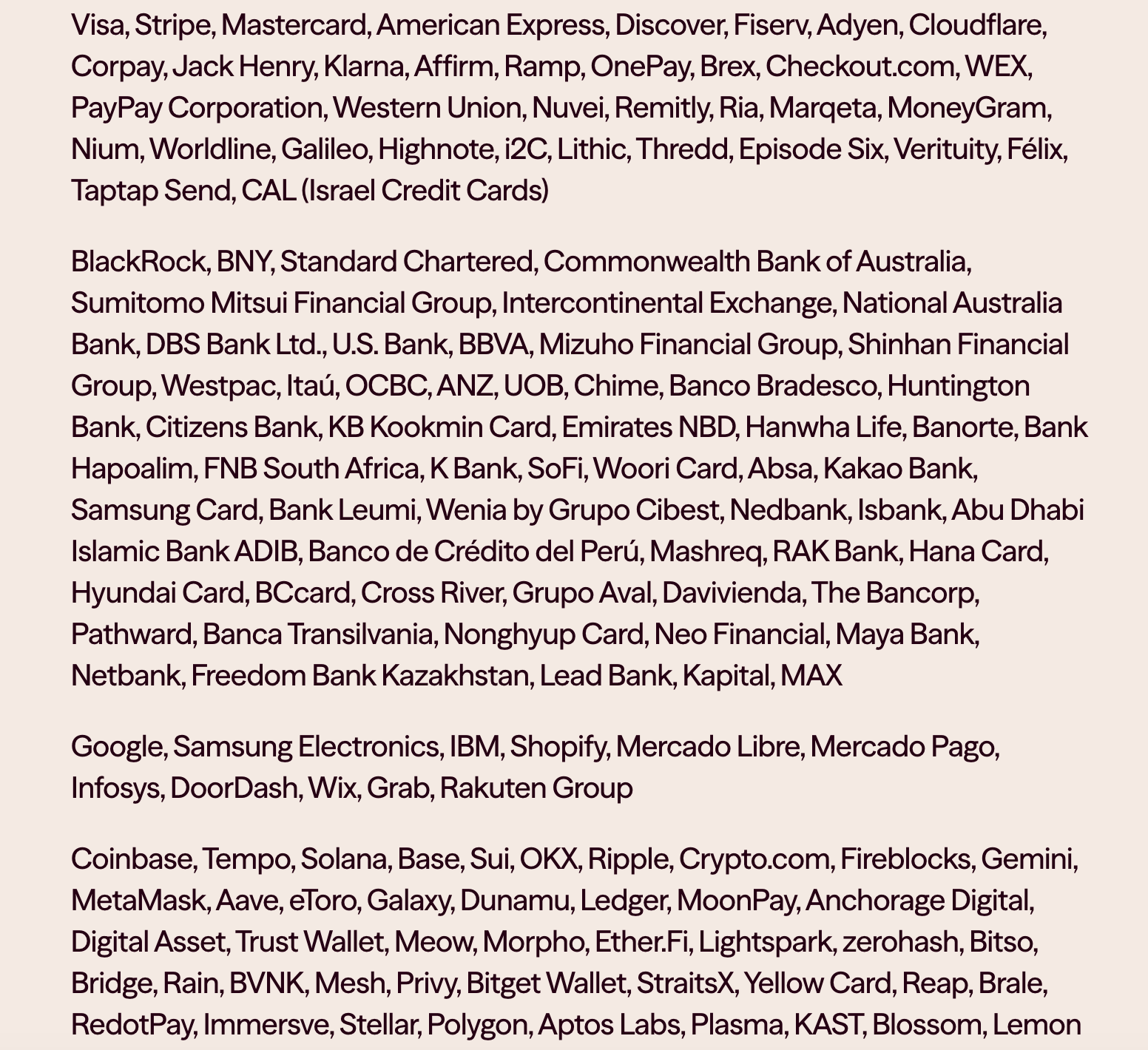

What surprised the market most was that Open Standard had already “secured” over 140 partners before the stablecoin’s launch.

This list includes several companies that have already issued stablecoins, such as Western Union, Ripple, MetaMask, and Aave. Gathering signatures from so many giants in both the Web3 and traditional finance sectors before the stablecoin’s issuance left the market both surprised and full of expectations for Open USD’s future development. The best indicator of this expectation was that Circle’s stock price, the leading stablecoin company, plummeted 17.55% on the same day, with less than 20% room before hitting a new low.

However, this explosive announcement was soon contradicted.

On July 3, according to a report by The Chosun Ilbo, companies including Samsung Electronics, Dunamu (parent company of Upbit), Shinhan Financial Group, and K Bank stated that they had never consulted on matters related to Open USD (OUSD). A Samsung Electronics official stated, “No formal consultations have taken place, and we don’t know what role we would play.” Similarly, Shinhan Financial Group, Dunamu, and K Bank said that Open Standard had inquired about their willingness to participate in OUSD, and they merely responded that they would “have a simple discussion,” but their names were included in the alliance member list.

Tony Chung, Head of BD at Korean Web3 media Blockmedia, also stated that a representative from one of the Korean companies learned they were listed through Korean media reports and was quite confused, as they had only casually replied, “If feasible, we’ll consider it.”

Founder and CEO of OpenAssets, Gabor Gurbacs, reposted Tony Chung’s tweet and stated that not only Korean companies were misled. By contacting some of OpenAssets’ clients on the list, Gabor Gurbacs received responses: “They claim they never signed or agreed to any agreement. Either the media severely misrepresented the facts, or the participant list is misleading.”

Viewed this way, Open Standard’s “hundred-list” may have included some companies that were merely contacted. In the original announcement, Open Standard stated: “Businesses across industries have signed up to use Open USD.” Perhaps in Open Standard’s view, not explicitly refusing equates to “agreeing” to use Open USD, but agreeing to use it doesn’t necessarily mean “it must be used.”

This is a classic marketing tactic of trading controversy for attention, and it certainly had some effect, though it somewhat feels like trampling on business ethics.

Facing such aggressive tactics and an “unorthodox” opponent, Circle co-founder and CEO Jeremy Allaire published a lengthy post on X questioning Open USD’s “three major features”:

Free Minting and Redemption: Attractive in the short term but potentially unsustainable at scale, leading to a lack of funds to maintain banking relationships, regulatory permits, and technical infrastructure. Circle already offers discounts to major partners through contracts, rather than making everything free.

Sharing Almost All Revenue with Partners: Could “starve” the infrastructure, leading to systemic underinvestment and limiting platform scale. Circle itself already shares most of its revenue with distribution partners.

Alliance / Multi-Company Governance: Circle previously co-founded the Centre Consortium with Coinbase but later consolidated it under Circle’s sole issuance. He believes the historical track record of scaling multi-company products is “very poor” (slow coordination, difficult decision-making).

Jeremy still expressed a welcoming attitude towards OUSD joining the “stablecoin family,” but every line of his post conveyed a viewpoint: the stablecoin business is one where time builds a winner-takes-all dynamic, and simply tweaking a few mechanisms isn’t enough to “sit at the table.”

Beyond these negative controversies, some companies on the list have clearly expressed support for Open USD’s development. Stripe stated it would set OUSD as the default stablecoin for businesses using stablecoins on its platform; Coinbase also said it would integrate OUSD onto Base and other chains, planning a launch later in 2026, to expand use cases like on-chain transactions, payments, and DeFi.

Payment network giants like Visa and Mastercard, financial institutions like BlackRock and BNY Mellon, and crypto-native projects like Aave, Solana, and Ripple, have also expressed support, though specific cooperation methods have not yet been clarified.

According to the announcement, Open Standard’s founding CEO is also the CEO of Bridge. This Bridge is the fiat on-ramp and off-ramp solution provider that once collaborated with multiple competitors in the struggle over Hyperliquid’s native stablecoin USDH issuance rights but was later acquired by Stripe—itself developing a stablecoin chain called Tempo, which has sparked controversy. Stripe also clarified its partnership immediately after Open Standard’s announcement, indicating a close relationship between the two.

A user named Bojan on X stated that Open Standard’s promotion is a typical “legitimacy-borrowing” behavior—i.e., leveraging the reputation or endorsement of other well-known, credible entities to quickly enhance its own legitimacy and credibility, without having actually obtained deep recognition or formal authorization. For a stablecoin track that requires trust as its foundation, OUSD seems to have left a somewhat negative first impression even before its launch. Written by Eric, Foresight News

On the evening of June 30, Beijing time, the emergence of a new stablecoin once again stirred the stablecoin landscape.

A company named Open Standard announced the launch of a stablecoin called Open USD, featuring free minting and redemption, sharing of reserve asset returns, and joint governance by partners. These open designs directly address pain points in stablecoin distribution and appear highly attractive.

What surprised the market most was that Open Standard had already “secured” over 140 partners before the stablecoin’s launch.

This list includes several companies that have already issued stablecoins, such as Western Union, Ripple, MetaMask, and Aave. Gathering signatures from so many giants in both Web3 and traditional finance before the stablecoin’s issuance left the market both surprised and full of expectations for Open USD’s future. The best indicator of this expectation was that Circle’s stock price, the leading stablecoin company, plummeted 17.55% on the same day, with less than 20% room before hitting a new low.

However, this explosive announcement was soon contradicted.

On July 3, according to a report by The Chosun Ilbo, companies including Samsung Electronics, Dunamu (parent company of Upbit), Shinhan Financial Group, and K Bank stated that they had never consulted about Open USD (OUSD) matters. A Samsung Electronics official stated, “No formal consultations have taken place, and we don’t know what role we would play.” Shinhan Financial Group, Dunamu, and K Bank also said that Open Standard had inquired about their willingness to participate in OUSD, and they merely indicated they “would have a simple discussion,” but their names were included in the alliance member list.

Tony Chung, Head of BD at Korean Web3 media Blockmedia, also mentioned that a representative from one of the Korean companies learned they were listed through reports in Korean media and was quite puzzled, as they had only casually replied, “If feasible, we’ll consider it.”

Founder and CEO of OpenAssets, Gabor Gurbacs, reposted Tony Chung’s tweet and stated that not only Korean companies were misled. By contacting some of OpenAssets’ clients on the list, Gabor Gurbacs received responses: “They claim they never signed or agreed to any agreement. Either the media severely misrepresented the facts, or the participant list is misleading.”

Viewed this way, Open Standard’s “hundred-list” may have included some companies that were merely contacted. In the original announcement, Open Standard stated: “Businesses across industries have signed up to use Open USD.” Perhaps in Open Standard’s view, not explicitly refusing equates to “agreeing” to use Open USD, but agreeing to use it doesn’t necessarily mean “it must be used.”

This is a classic marketing tactic of trading controversy for attention, and it certainly had some effect, though it somewhat feels like trampling on business ethics.

Facing such aggressive tactics and an “unorthodox” opponent, Circle co-founder and CEO Jeremy Allaire published a lengthy post on X questioning Open USD’s “three major features”:

Free Minting and Redemption: Attractive in the short term but potentially unsustainable at scale, leading to a lack of funds to maintain banking relationships, regulatory permits, and technical infrastructure. Circle already offers discounts to major partners through contracts, rather than making everything free.

Sharing Almost All Revenue with Partners: Could “starve” the infrastructure, leading to systemic underinvestment and limiting platform scale. Circle itself already shares most of its revenue with distribution partners.

Alliance / Multi-Company Governance: Circle previously co-founded the Centre Consortium with Coinbase but later consolidated it under Circle’s sole issuance. He believes the historical track record of scaling multi-company products is “very poor” (slow coordination, difficult decision-making).

Jeremy still expressed a welcoming attitude towards OUSD joining the “stablecoin family,” but every line of his post conveyed a viewpoint: the stablecoin business is one where time builds a winner-takes-all dynamic, and simply tweaking a few mechanisms isn’t enough to “sit at the table.”

Beyond these negative controversies, some companies on the list have clearly expressed support for Open USD’s development. Stripe stated it would set OUSD as the default stablecoin for businesses using stablecoins on its platform; Coinbase also said it would integrate OUSD onto Base and other chains, planning a launch later in 2026, to expand use cases like on-chain transactions, payments, and DeFi.

Payment network giants like Visa and Mastercard, financial institutions like BlackRock and BNY Mellon, and crypto-native projects like Aave, Solana, and Ripple have also expressed support, though specific cooperation methods have not yet been clarified.

According to the announcement, Open Standard’s founding CEO is also the CEO of Bridge. This Bridge is the fiat on-ramp and off-ramp solution provider that once collaborated with multiple competitors in the struggle over Hyperliquid’s native stablecoin USDH issuance rights but was later acquired by Stripe—itself developing a stablecoin chain called Tempo, which has sparked controversy. Stripe also clarified its partnership immediately after Open Standard’s announcement, indicating a close relationship between the two.

A user named Bojan on X stated that Open Standard’s promotion is a typical “legitimacy-borrowing” behavior—i.e., leveraging the reputation or endorsement of other well-known, credible entities to quickly enhance its own legitimacy and credibility, without having actually obtained deep recognition or formal authorization. For a stablecoin track that requires trust as its foundation, OUSD seems to have left a somewhat negative first impression even before its launch.

This article is sourced from the internet: OUSD’s “100-Person List” is Actually a “Letter of Intent”? Borrowing Legitimacy Through Name-Dropping Sparks Trust Crisis

Leading global cryptocurrency exchange BitMart announced today that bSPCX, a tokenized fund equity linked to SpaceX (NASDAQ: SPCX) launched via BitMart IPOPrime, will officially open for trading on the BitMart secondary market after meeting liquidity conditions. This follows SpaceX’s Nasdaq debut this morning at an issuance price of $135. The key factor today is “share allocation.” Market demand for SpaceX far exceeded supply, with multiple platforms having to issue full refunds after failing to secure allotments. BitMart secured primary allocation resources and distributed them to every IPOPrime subscriber—none went empty-handed. Each user’s subscription was allocated on a pro-rata basis (average actual allocation per person was approximately 40%), with the unallocated portion automatically refunded. Since bSPCX has no underlying lock-up period, holders can trade and exit immediately based on real-time Nasdaq…