Aave is ceding its DeFi lending throne due to its own folly

Author: Azuma (@azuma_eth)

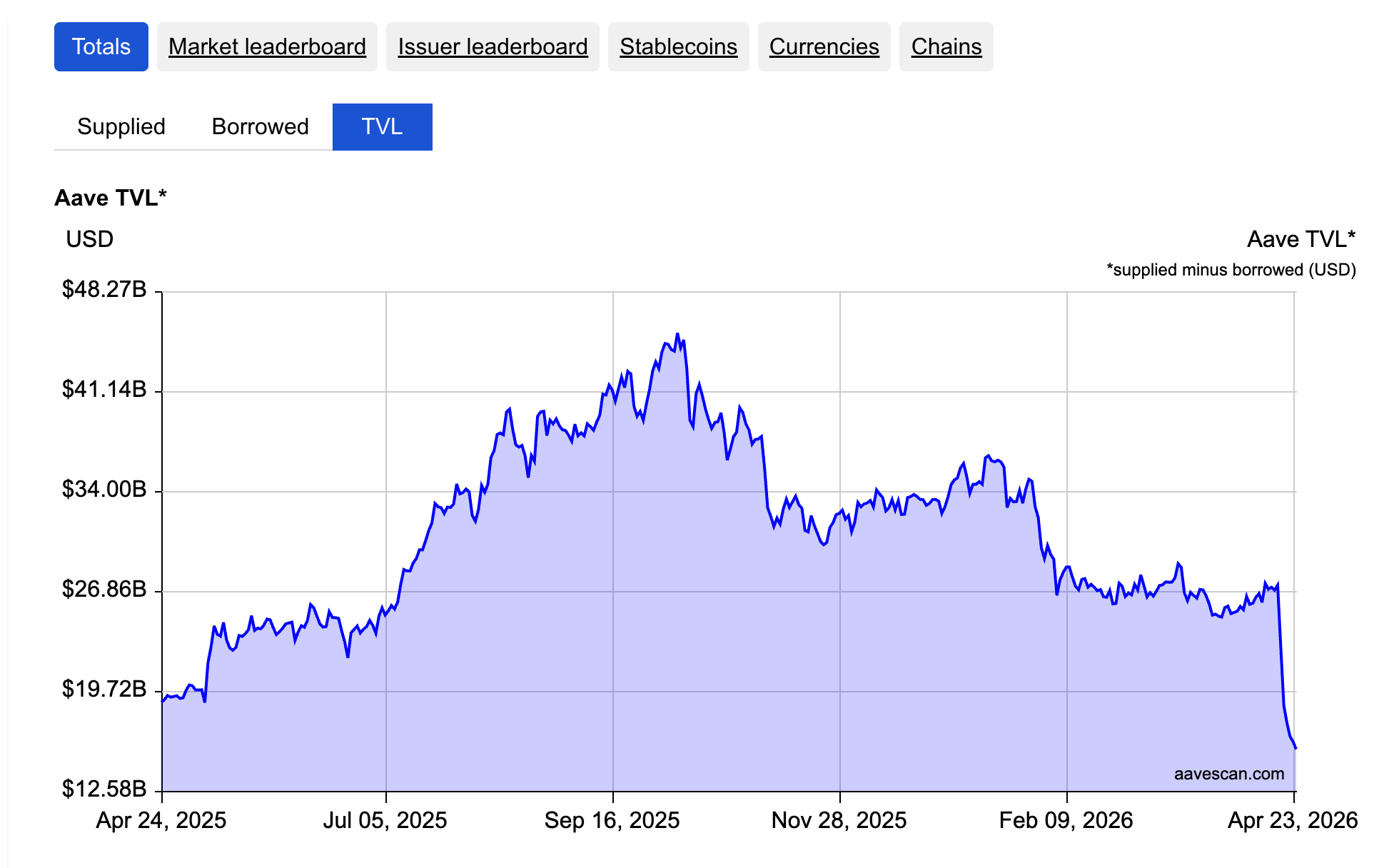

$292 million – that’s the total amount of rsETH stolen from Kelp DAO; $17.2 billion – that’s the volume of funds withdrawn from Aave since the incident.

Aave is now watching community panic fester for days due to its remarkably poor crisis management strategy, thereby forfeiting its greatest advantages in the lending track: hundreds of billions in locked funds and the “safest DeFi” user perception.

- Odaily Note: For background, please refer to DeFi lost $292 million again. Is even Aave no longer safe? and The three-way game under a $290 million hole: Who will foot the bill—Aave, LayerZero, or Kelp?.

What did Aave do wrong?

There’s no need to rehash the details of the Kelp DAO hack. Blaming Aave for granting such a high LTV to rsETH is pointless now. This article aims to discuss Aave’s response strategy from the perspective of a long-term AAVE user.

First, there’s the issue of the bad debt scale. Aave itself has crunched the numbers. Depending on how rsETH is handled, two potential bad debt scenarios exist: If the stolen loss is deducted from all circulating rsETH, estimated bad debt would be $123.7 million. If the value of mainnet rsETH is guaranteed, attributing all losses to the mapped rsETH on Layer 2 would result in estimated bad debt of $230.1 million.

In either case, Aave has the financial capacity to cover it, leveraging Umbrella, the DAO treasury, and team reserves. I understand that Aave may be unwilling to bear this cost alone, hoping the primary responsible party, Kelp DAO, and the secondary party, LayerZero, would contribute more. But the problem is the other parties think the same: “Aave is so well-funded and in such an awkward position, they should shoulder more.” So, short-term negotiations among the three parties are unlikely to reach a consensus, meaning there’s no immediate win-win solution.

But users can’t wait that long. Aave’s yield has never been particularly competitive, and users deposit funds based on reputation, security, and liquidity. Yet, during the most critical days after the incident, Aave never offered users any kind of backstop commitment. Instead, it repeatedly emphasized “our code is fine” and “Aave has no control over how rsETH is accounted for,” shifting blame.

This allowed panic to fester in the community. Users scrambled to escape—those who could withdraw did, and those who couldn’t would borrow from other pools, amplifying the impact. Now, Aave faces a situation where it is simultaneously experiencing continuous capital outflows and liquidity dry-ups in multiple pools due to maxed-out utilization rates.

This awkward situation could have been avoided (or at least mitigated). Since Aave has the financial means, why didn’t it reassure the community early on to prevent a bank run? It’s just a potential $230 million in bad debt (or less), and Aave wouldn’t need to foot the entire bill alone; they could argue with LayerZero and Kelp DAO later.

Now, to avoid promising up to $230 million in relief, Aave watched $17.2 billion in locked funds exit (and the number may grow), not to mention the days of AAVE token price declines. No matter how you calculate it, it’s a terrible deal.

Worse still for Aave, the worse its situation gets, the more relaxed LayerZero, Kelp DAO, and other counterparties become. They will assume Aave has more incentive to resolve the issue quickly, putting Aave at a disadvantage in negotiations.

Having reached this point, Aave has only itself to blame.

Behind Aave, Spark is watching closely

While Aave scrambles, its competitor Spark is thriving. What’s more ironic is that Spark was effectively “incubated” by Aave.

Spark, originally a lending protocol forked from Sky (formerly MakerDAO) using the open-source code of Aave V3, shares the same underlying code logic. In return, Spark had a profit-sharing agreement with Aave. However, Aave later accused Spark of breaching the agreement, and due to differing roadmaps, the two are now purely competitive.

Three months before the Kelp DAO hack, Spark had already removed support for rsETH (details in Same day, different fates: Aave embraces rsETH, losing nearly $200 million; Spark exits unscathed). Call it strategic conservatism, rigorous risk control, or even sheer luck, but Spark emerged from this incident completely unscathed. On this point alone, Spark can freely attack Aave’s “safest DeFi” label.

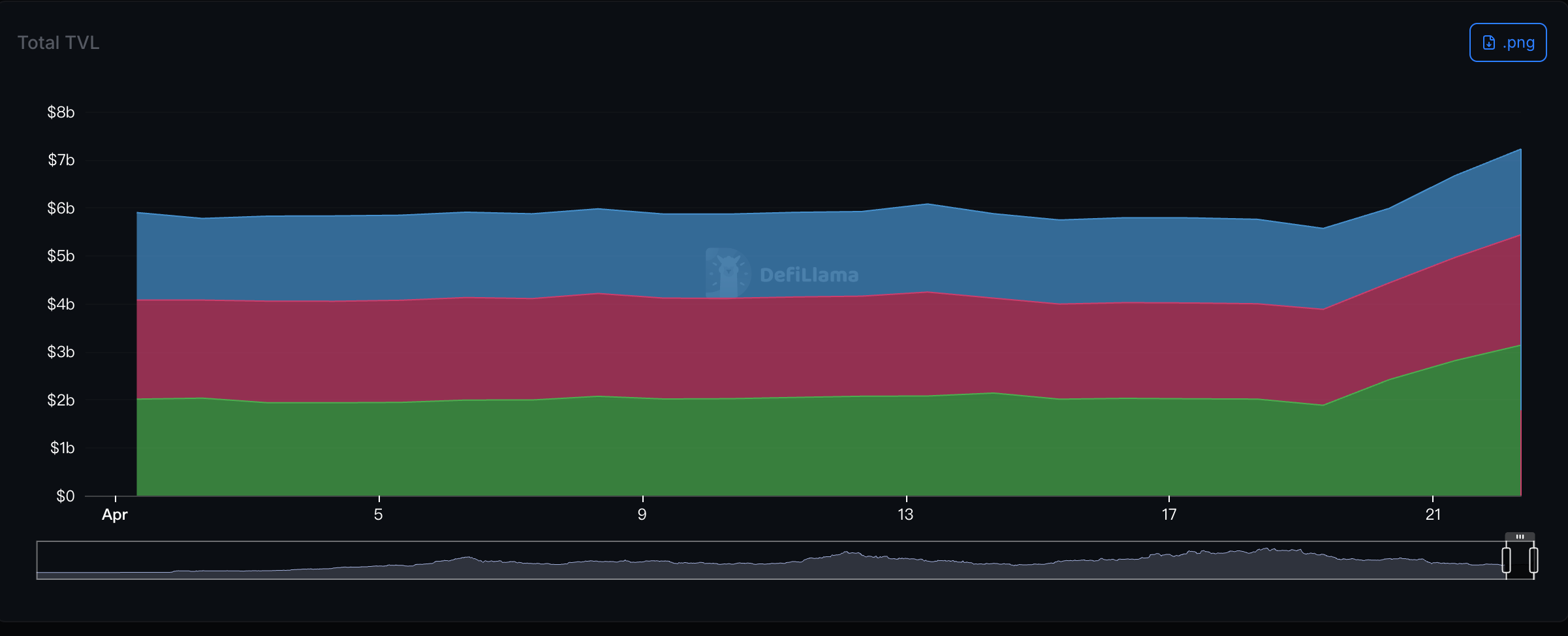

Consequently, Spark has become a safe haven for funds fleeing Aave. Since the incident, Spark’s TVL has grown by nearly $2 billion (green section in the chart below). On the day of the incident, Justin Sun withdrew 53,665 ETH (worth $124 million) from Aave and deposited it into Spark, and has continued to accumulate, bringing his deposits to $1.3 billion. In DeFi, one must learn from Sun’s moves.

On April 23, Upbit officially listed Spark (SPK) on its Korean won trading market. SPK surged over 80% in a single day, significantly narrowing its market cap gap with AAVE.

Even F2Pool founder Wang Chun reflected on X: “In the past year, I received 83.7 million SPK rewards from Spark and sold them on CoWSwap for 663 ETH and $1.4 million. Now, I kind of regret it.“

Spark clearly recognized this as a golden opportunity to capture market share from Aave. Since the incident, Spark’s strategy lead, MonetSupply, has become the most vocal KOL on the matter, posting dozens of times a day. While his statements have indeed helped the public understand what’s happening, they’ve also objectively fueled panic surrounding Aave.

But this is pure business competition. MonetSupply simply made the most correct choice.

Aave is losing its DeFi lending throne

In the early hours of April 24, perhaps aware of the dire situation, Aave founder Stani announced on X the launch of a relief plan called DeFi United. Cooperation partners include LayerZero, Ethena, ether.fi, Ink Foundation, Golem Foundation, Trydo, and more. Stani personally will donate 5,000 ETH to address the current issues.

But the funds have already fled, and user trust is severely damaged. With this belated statement alone, Aave will struggle to regain locked funds and user trust anytime soon.

The DeFi lending track has long seen a “one dominant player, many strong contenders” landscape, with Aave holding what seemed to be a very stable lead. Now, Aave has voluntarily given up that throne. Behind it, challengers are formidable. Besides the surging Spark, other competitors like Morpho and Jupiter Lend are also vying to take a share from Aave.

Last year, Stani purchased a five-story mansion in London for about $30 million, one of the most expensive transactions in the UK’s sluggish luxury real estate market that year. I don’t know if there’s some kind of “jinx” at play, but following examples like Su Zhu, it seems big spenders in the crypto circle often stumble into bad luck.

I can only guess what Stani is thinking now in his five-story mansion.

This article is sourced from the internet: Aave is ceding its DeFi lending throne due to its own folly

Related: Matrixport Research: Why Is the Altcoin Bull Market Absent? Supply Pressure and Token Unlocks Emerge as Key Variables

Sustained Supply Pressure: Altcoin Upside Momentum Remains Constrained Since October 2025, although Bitcoin has experienced periodic pullbacks, its market dominance has not declined significantly and has recently trended higher again. This market movement appears more like a Bitcoin-led rally, with altcoins following intermittently. Meanwhile, an increasing number of companies adopting treasury allocation strategies continue to accumulate Bitcoin, maintaining its structural demand. In contrast, altcoins face more pronounced supply pressure. Continuous selling by early investors, coupled with new circulating supply from token unlocks, frequently caps price rebounds with selling pressure. Since August 2024, approximately $99 billion worth of tokens have been unlocked and entered circulation, creating a persistent supply shock for the market. As retail enthusiasm cools, the impact of supply-side factors has gradually become a key variable dominating price trends.…