Arthur Hayes: Japanese banks selling U.S. Treasuries boosts new cryptocurrency bull market

Original title: Shikata Ga Nai

Original author: Arthur Hayes

Original translation: Ismay, BlockBeats

Editors note: Against the backdrop of global economic turmoil and financial market volatility, Hayes delves into the challenges faced by the Japanese banking system during the Feds rate hike cycle and the profound impact of U.S. fiscal and monetary policies on global markets. By analyzing in detail the foreign exchange hedging U.S. Treasury bond investment strategies of Norinchukin Bank and other Japanese commercial banks, the article reveals why these banks have to sell U.S. Treasuries as interest rate differentials widen and foreign exchange hedging costs rise. Hayes further discusses the role of the FIMA repo mechanism and its impact on U.S.-Japan financial relations, and predicts the key role of this mechanism in maintaining market stability. The article ultimately calls on investors to seize investment opportunities in the crypto market under the current circumstances.

I just finished reading Red Mars, the first book in Kim Stanley Robinson’s trilogy, and one of the characters in the book, Japanese scientist Hiroko Ai, often says “Shikata ganai,” which means “nothing can be done,” when talking about situations beyond the control of the Martian colonists.

This sentence came to my mind as I was thinking of a title for this short article. This article will focus on the Japanese banks that fell victim to Pax Americanas monetary policy. What did these banks do? In order to get a nice yield on yen deposits, they engaged in the dollar-yen carry trade. They borrowed from elderly Japanese savers at home, looked around Japan and found that all the safe government and corporate bonds were yielding almost zero, so they concluded that lending money to Pax Americana through the U.S. Treasury (UST) market was a better use of capital because these bonds would provide a higher yield even when fully hedged against exchange rate risk.

But when the US saw massive inflation due to cash bribes paid to the public to appease the public into accepting being locked in their homes and injected with experimental drugs to fight the baby boom, the Federal Reserve (Fed) had to act. The Fed raised interest rates at the fastest pace since the 1980s. The result was bad news for anyone holding US Treasuries. From 2021 to 2023, rising yields led to the worst bond rally since the War of 1812. Nothing could be done!

In March 2023, the first bank losses seeped through the underbelly of the financial system. In less than two weeks, three major banks failed, leading to the Fed’s blanket backstop of all U.S. Treasuries on the balance sheet of any U.S. bank or U.S. branch of a foreign bank. As expected, Bitcoin surged in the months following the bailout announcement.

Since the bailout was announced on March 12, 2023, Bitcoin has risen by more than 200%.

To underpin this roughly $4 trillion bailout (my estimate of the total amount of Treasuries and mortgage-backed securities held on the balance sheets of US banks), the Fed announced in March that using the discount window was no longer the “kiss of death.” If any financial institution needed a quick infusion of cash to fill an intractable hole in its balance sheet caused by a fall in the price of “safe” government bonds, it should use the window immediately. When the banking system inevitably has to be bailed out by devaluing the currency and undermining the dignity of human labor, what do we say? Nothing can be done!

The Fed did the right thing for U.S. financial institutions, but what about the foreigners who also bought large amounts of U.S. Treasuries during the global funding surge from 2020 to 2021? Which country’s bank balance sheets are most likely to be overwhelmed by the Fed? Of course, it’s the Japanese banking system.

The latest news shows that the fifth largest Japanese bank will sell $63 billion worth of foreign bonds, most of which are US Treasuries.

Japans Norinchukin Bank to sell $63 billion of U.S. and European bonds

Interest rates in the U.S. and Europe rose and bond prices fell. This reduced the value of the high-priced (low-yielding) foreign bonds that Norinchukin Bank had bought in the past, causing its paper losses to widen.

Norinchukin Bank was the first to capitulate and announce that it had to sell bonds. All the other banks were engaging in the same trade, as I will explain below. The Council on Foreign Relations gives us an idea of the size of the huge bond sales that the Japanese commercial banks may have.

Japanese commercial banks held about $850 billion in foreign bonds in 2022, according to the International Monetary Fund’s Coordinated Survey of Portfolio Investments. That included nearly $450 billion in U.S. bonds and about $75 billion in French debt — a figure far exceeding their holdings of bonds issued by other large eurozone countries.

Why is this important? Because Yellen will not allow these bonds to be sold on the open market and cause Treasury yields to spike. She will ask the Bank of Japan (BOJ), which is supervised by the Bank of Japan, to buy these bonds. The BOJ will then use the Foreign and International Monetary Authorities (FIMA) repo facility established by the Federal Reserve in March 2020. The FIMA repo facility allows central bank members to pledge U.S. Treasuries and receive newly printed dollars overnight.

The increase in FIMA repo facilities indicates an increase in USD liquidity in global currency markets. You all know what this means for Bitcoin and cryptocurrencies… That’s why I thought it was important to remind readers about another invisible money printing avenue. It was only after reading a dry Atlanta Fed report titled “Offshore Dollars and U.S. Policy” that I realized how Yellen prevented these bonds from entering the open market.

Why now?

The Fed signaled at the end of 2021 that it would start raising policy rates in March 2022, and from that point on, U.S. Treasuries (USTs) began to collapse. Its been more than two years, so why would a Japanese bank choose to recognize its losses now after two years of pain? Another strange fact is that according to the consensus view of economists, whom you should listen to: the US economy is on the verge of a recession. Therefore, the Fed is likely to cut interest rates in a few meetings. A rate cut will drive bond prices higher. Why sell now when all the smart economists tell you that relief is just around the corner?

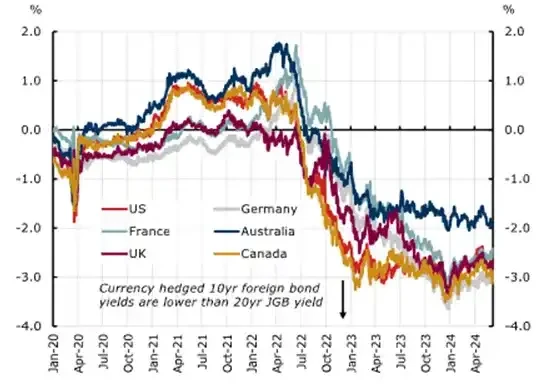

The reason is that Norinchukin Banks foreign exchange hedge purchases of US Treasuries went from slightly positive to sharply negative yields. Before 2023, the interest rate differential between the US dollar and the yen was minimal. Then the Fed parted ways with the Bank of Japan (BOJ) by raising rates, while the BOJ stuck to -0.1%. As the gap widened, the cost of hedging the dollar risk embedded in US Treasuries outweighed the higher yields.

Heres how it works. Norinchukin Bank is a Japanese bank that holds yen on deposit. If it wants to buy higher-yielding U.S. Treasuries, it has to pay in dollars. Norinchukin Bank will sell yen today and buy dollars to buy the bonds; this is done in the spot market. If Norinchukin Bank does only this and the yen appreciates before the bonds mature, Norinchukin Bank loses money when it sells the dollars back to yen. For example, you buy dollars today at USDJPY 100 and sell them tomorrow at USDJPY 99; the dollar depreciates and the yen appreciates. Therefore, Norinchukin Bank typically sells dollars and buys yen in the three-month forward market to hedge this risk. It rolls over every three months until the bonds mature.

Typically, three-month forward contracts are the most liquid. That’s why banks like Norinco use rolling three-month forward contracts to hedge 10-year currency purchases.

As the USD-JPY interest rate differential widens, the forward point becomes negative because the Feds policy rate is higher than the Bank of Japans rate. For example, if spot USDJPY is 100 and the US dollar yields 1% more than the Japanese yen in the next year, the USDJPY one-year forward price should be around 99. This is because if I borrow 10,000 yen today at 0% interest to buy 100 US dollars, and then deposit the 100 US dollars to earn 1% interest, I will have 101 US dollars in a year. What should the USDJPY one-year forward price be to offset this 1 US dollar interest income? About 99 USDJPY, which is the no-arbitrage principle. Now imagine that I did all this just to buy a US Treasury bond that yields only 0.5% more than a Japanese government bond (JGB) of similar maturity. I actually paid a negative yield of 0.5% on this transaction. If this were the case, Norinchukin or any other bank would not make this transaction.

Back to the chart, as the differential widens, the three-month forward point becomes so negative that the yield on US Treasuries FX hedged back to JPY is lower than buying JPY-denominated JGBs outright. Starting in mid-2022, youll see the red line for USD is below 0% on the X-axis. Remember, the Japanese bank buying JPY-denominated JGBs has no currency risk, so theres no reason to pay the hedging fee. The only reason to do this trade is if the yield after FX hedging is > 0%.

Norinco is in a worse situation than the long-term participants of FTX/Alameda. The US Treasuries that were likely purchased in 2020-2021 are down 20% to 30% from a market value perspective. In addition, the cost of FX hedging has increased from negligible to over 5%. Even if Norinco believes that the Fed will cut rates, a 0.25% rate cut is not enough to reduce hedging costs or boost bond prices to stop the bleeding. Therefore, they must sell US Treasuries.

Any plan that would allow Norinchukin Bank to pledge U.S. Treasuries in exchange for new dollars would not solve the cash flow problem. The only thing that would return Norinchukin Bank to profitability from a cash flow perspective would be a significant narrowing of the policy rate gap between the Fed and the Bank of Japan. Therefore, using any Fed program, such as the Standing Repo Facility, which allows U.S. branches of foreign banks to repurchase U.S. Treasuries and mortgage-backed securities in exchange for newly printed dollars, would be ineffective in this context.

As I wrote this, I racked my brain to think of any other financial means that could enable Norinco to avoid selling the bonds. But as mentioned above, the existing plans are all some form of loans and swaps. As long as Norinco holds the bonds in any form, the currency risk remains and must be hedged. Only after the bonds are sold can Norinco unwind its foreign exchange hedge, which is a huge cost for it. This is why I believe Norincos management has explored all other options and selling the bonds is a last resort.

I will explain why Yellen is unhappy about this situation, but for now, lets turn off Chat GPT and use our imaginations. Is there a Japanese public institution that can buy bonds from these banks and take on the dollar interest rate risk without fear of bankruptcy?

Ding Dong

Who is there?

Its the Bank of Japan.

Rescue Mechanism

The Bank of Japan (BOJ) is one of the few central banks that can use the FIMA repo mechanism. It can hide the price discovery of US Treasuries by:

The Bank of Japan gently suggested that any Japanese commercial banks that needed to sell US Treasuries sell them directly onto the Bank of Japans balance sheet, rather than on the open market, and settle at the current last traded price without impacting the market. Imagine you could sell all the FTT tokens at the market price because Caroline Allison was there to support the market and could provide any necessary scale of support. Obviously, this would not work well for FTX, but she is not a central bank with a printing press. Her printing press can only handle $10 billion of customer funds, while the Bank of Japan handles unlimited.

The Bank of Japan then uses the FIMA repo mechanism to exchange U.S. Treasuries for dollars printed out of thin air by the Federal Reserve.

One, two, lace up. Such an easy way to circumvent the free market. Man, thats a freedom worth fighting for!

Let’s ask a few questions to understand the impact of this policy.

Someone has to lose money here; losses on bonds due to rising rates are still there. Who is being sucked in?

The Bank of Japan will still recognize a loss for selling the bonds to the Bank of Japan at current market prices. The Bank of Japan now bears future U.S. Treasury maturity risk. If the price of these bonds falls, the Bank of Japan will have unrealized losses. However, this is the same risk the Bank of Japan currently faces on its multi-trillion yen JGB portfolio. The Bank of Japan is a quasi-governmental entity that cannot go bankrupt and is not subject to capital adequacy requirements. It also does not have a risk management department that forces a reduction in positions when its Value-at-Risk (VAR) rises due to huge DV 01 risks.

As long as the FIMA repo mechanism exists, the Bank of Japan can roll over repo every day and hold U.S. Treasuries until maturity.

How does the dollar supply increase?

The repo agreement requires the Fed to provide dollars to the Bank of Japan in exchange for U.S. Treasuries. This loan is rolled over daily. The Fed obtains these dollars through its printing press.

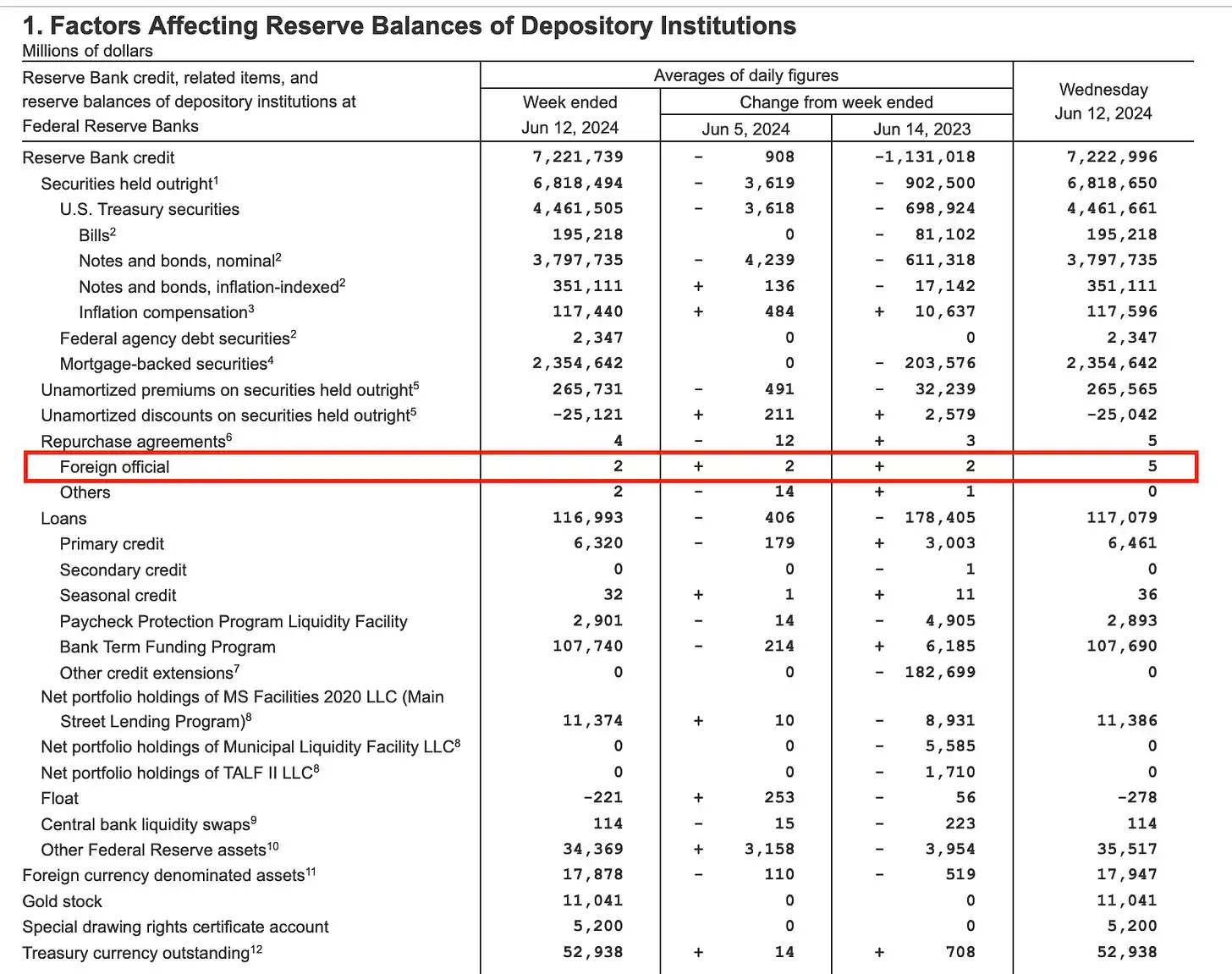

We can monitor the dollars injected into the system on a weekly basis. The name of the program is “Repurchase Agreements – Foreign Official”.

As you can see, FIMA repo is very small at the moment. But the sell-off has not started yet, and I think there will be some interesting phone calls between Yellen and BoJ Governor Ueda. If I am right, this number will increase.

Why help others?

Americans arent known for their sympathy for foreigners, especially those who dont speak English and look strange. Appearance is relative, but to those tanned, Confederate flag-waving rednecks living in the flyover states, the Japanese just dont look right. And you know what? These same vulgar people will decide who the next emperor will be this November. Its really speechless.

The reason Yellen would lend a helping hand despite the underlying xenophobia is that without new dollars to absorb these junk bonds, all the big Japanese banks would follow Norinchukin Bank’s lead and sell off their US Treasury portfolios to ease the pain. This would mean $450 billion worth of US Treasuries would quickly hit the market. This cannot be allowed because yields would soar, making financing the federal government very expensive.

This is why the FIMA repo facility was created, as the Fed’s own words put it:

“During the ‘rush for cash’ in March 2020, central banks simultaneously sold U.S. Treasuries and parked the proceeds in overnight repos at the New York Fed. In response, the Fed offered in late March to provide central banks with overnight loans using U.S. Treasuries held in custody at the New York Fed as collateral, at an interest rate above private repo rates. Such loans would allow central banks to raise cash without forcing outright sales in an already strained Treasury market.”

Remember September-October 2023? During those two months, the Treasury yield curve steepened, causing the SP 500 to fall 20%, and the yields on 10-year and 30-year Treasury bonds exceeded 5%. In response, Yellen shifted most of the debt issuance to short-term Treasury bonds to drain the cash in the Feds reverse repo program. This boosted the market, and starting on November 1, all risk assets, including cryptocurrencies, began to rise.

I am very confident that in an election year, when her boss faces the threat of being defeated by the criminal hands of the Orange Man, Yellen will fulfill her duty to democracy and ensure that yields remain low to avoid a financial market disaster. In this case, all Yellen needs to do is call Ueda and instruct him not to allow the Bank of Japan to sell US Treasuries on the open market, but to use the FIMA repo mechanism to absorb the supply.

Trading straregy

Everyone is watching closely to see when the Fed will finally start cutting rates. However, the USD-JPY interest rate differential is +5.5% or 550 basis points, which is equivalent to 22 rate cuts (assuming the Fed cuts by 0.25% per meeting). One, two, three or four rate cuts over the next twelve months will not significantly reduce this differential. Moreover, the Bank of Japan has shown no willingness to raise its policy rate. At most, the Bank of Japan may reduce the pace of its open market bond purchases. And the reason why Japanese commercial banks must sell their FX-hedged US Treasury portfolios is not addressed.

That is why I am confident that the move from Ethena-collateralized USD (sUSDe), currently earning 20-30% yield, to crypto risk assets will accelerate. Given this news, the pain has reached a point where the Bank of Japan has no choice but to exit the US Treasury market. As I mentioned, in an election year, the last thing the ruling Democratic Party needs is a sharp rise in US Treasury yields, as this will affect the main financial issues that the median voter cares about the most, namely mortgage rates, credit card and auto loan rates. If Treasury yields rise, these rates will all rise.

This is exactly why the FIMA repo facility was created. All that is needed now is for Yellen to insist that the BoJ use it.

Just when many began to wonder where the next dollar liquidity shock would come from, the Japanese banking system delivered brand new dollars made of origami cranes to crypto investors. This is just another pillar of the crypto bull market. In order to maintain the current dollar-based Pax Americana filthy financial system, the dollar supply must increase.

Say it with me, “Shikata ga nai” and buy the dips!

This article is sourced from the internet: Arthur Hayes: Japanese banks selling U.S. Treasuries boosts new cryptocurrency bull market

In recent months, the popularity of tokens with high valuations and low initial circulating supply has been a topic of discussion in the crypto community. This stems from the concern that this market structure leaves little sustainable upside for traders after the token generation event (TGE). – This is the opening sentence in the article Binance Research: Low circulation and high FDV tokens are prevalent, why has the market developed to this point? released by Binance Research this week. It seems that all of a sudden, the reasons and discussions for the prevalence of high FDV, low circulation tokens have become the headlines of the cryptocurrency media and are frequently mentioned in the hot topics of community members. On May 20, Binance announced that it will take the lead in…