Original article by: Pascal Hügli, Brick Towers

Original translation: Lucy, BlockBeats

Editors note: With the maturity of the Bitcoin market and the emergence of various income products, people have begun to think about how to promote the financialization of Bitcoin while maintaining its native characteristics. From Bitcoins native consensus, assets to income, this article discusses different categories of Bitcoin income products and emphasizes the importance of localized design in reducing trust dependence and counterparty risk.

While analyzing existing solutions, Pascal Hügli shows how to achieve a near-perfect Bitcoin fit by combining native Bitcoin consensus, assets, and returns, using the Brick Towers project as an example. This article highlights the importance of balancing innovation and risk management in the financialization of digital currencies. Despite many challenges and unknowns, Bitcoin, as an open and decentralized protocol, will continue to lead the development of financial technology with its native design and fundamental characteristics.

Bitcoin is undergoing a remarkable evolution, with multiple views on its nature. Some see it as a currency for daily transactions, others as a modern gold for storing value, and still others as a decentralized global platform that secures and verifies off-chain transactions. While each of these views has merit, Bitcoin is increasingly being viewed as a digital base currency.

Bitcoin functions similarly to physical gold, as a holding asset, inflation hedge, and provides a dollar-like monetary denomination, Bitcoin is reinventing the concept of a monetary base asset. Its transparent algorithm and fixed supply of 21 million units ensure a non-discretionary monetary policy. In contrast, traditional fiat currencies such as the US dollar rely on central authorities to manage their supply, raising questions about their predictability and effectiveness in an era of volatility, uncertainty, complexity, and ambiguity (VUCA).

This contrast is particularly prominent in Nobel Prize winner Friedrich August von Hayek’s critique of centralized monetary decision-making in his book The Prepense of Knowledge. Bitcoin’s transparent and predictable monetary policy stands in stark contrast to the opaque and potentially unpredictable nature of traditional fiat currency management.

Should I use Bitcoin?

For staunch Bitcoin supporters, the 21 million supply cap is sacrosanct. Changing this cap would fundamentally change the nature of Bitcoin and make it something completely different. As a result, the Bitcoin community is generally skeptical of leveraging Bitcoin. Many believe that any form of leveraged operations is similar to the practices of fiat currencies and undermines the core principles of Bitcoin.

This skepticism about leveraged Bitcoin is rooted in the distinction between commodity credit and circulation credit outlined by Ludwig von Mises. Commodity credit is based on real savings, while circulation credit has no such backing and is similar to an unsecured IOU. Bitcoin supporters believe that leveraging to create paper Bitcoin is economically risky and unstable.

Even some of the more nuanced views within the community remain cautious about leveraged Bitcoin, in line with the stance of Caitlin Long and others, who have been warning about the dangers of leveraged Bitcoin. The collapse of some leveraged Bitcoin lending companies such as Celsius and BlockFi in 2022 further reinforced the concerns of Long and others about the risks of leveraged Bitcoin.

Celsius and others have proven this

The crypto markets experienced a major turmoil similar to the collapse of Lehman Brothers in 2022, triggering a widespread credit crunch that affected multiple players in the crypto lending space. Contrary to assumptions, most crypto lending activity is not peer-to-peer and carries considerable counterparty risk, as clients lend funds directly to platforms, which then invest those funds in speculative strategies without adequate risk management.

During the DeFi Summer of 2020, the rise of major DeFi protocols provided promising avenues for yield generation. However, many of these protocols lacked sustainable business models and token economics. They relied heavily on inflation of protocol tokens to maintain attractive yields, resulting in an unsustainable ecosystem divorced from fundamental economic principles.

The 2022 crypto credit crunch exposed a variety of issues with centralized yield instruments, highlighting concerns about transparency, trust, and liquidity, market, and counterparty risk. In addition, it highlighted the shortcomings of centralized and off-chain risk management processes, which, when applied to blockchain-based “banking services,” mimic the shortcomings of traditional banks.

Despite the optimism brought about by the bull run in 2020 and 2021, many institutions such as Voyager, Three Arrows Capital, Celsius, BlockFi, and FTX have collapsed due to the lack of these necessary processes. The inability to transparently and independently implement the necessary checks and balances often leads to over-regulation and ongoing failures and fraud, reflecting the historical challenges of the traditional banking system. However, lack of regulation is not the solution either.

Bitcoin income is not an option

So how do we respond? In light of this event in 2022, a growing number of Bitcoin supporters are asking the question: should we embrace Bitcoin yield products, or are they too risky, similar to the fiat currency system? While these concerns are legitimate, it is unrealistic to expect Bitcoin yield products to disappear entirely.

This question becomes more and more prominent as the emerging Bitcoin ecosystem develops. More and more projects are building or claiming to develop financial infrastructure and applications directly on Bitcoin. Will this once again cause problems that we have already seen in the wider crypto space?

Most likely. Because that’s the nature of the game. Since Bitcoin is a permissionless protocol, anyone can build on it, including those who wish to build a Bitcoin-powered financial system. And a financial system inevitably requires credit and leverage.

It is a historical fact that in any prosperous society, the need for credit and earnings naturally emerges as a catalyst for economic growth. Without credit, underdeveloped economies struggle to survive. Only through access to credit can more complex and efficient economic structures be formed.

In order to realize the vision of a Bitcoin-based economy, supporters recognize the need to develop credit and yield mechanisms on top of the Bitcoin protocol. While Bitcoin is often praised for its role as a currency, the reality is that in order to function effectively as a currency, it requires a native economy to support it.

This highlights the importance of Bitcoin-based yield products in promoting the growth of a Bitcoin-centric economy. Such an ecosystem would utilize Bitcoin as its digital base currency while using yield products to drive its adoption and usage.

This is all a trust range, anonymous

The financial system powered by Bitcoin will necessarily be built in layers. From a systemic perspective, this is not much different from the current financial system, and there are inherent layers in assets like money. In order to properly understand these inevitable trade-offs, we need a high-level framework to distinguish between different layers of Bitcoin implementation.

When offering Bitcoin yields, it is important to understand that these options can be structured along a three-fold trust spectrum. The main ones to focus on are:

-

consensus

-

assets

-

income

Assessing Bitcoin-like assets and Bitcoin income products based on their degree of Bitcoin nativeness provides a valuable framework to evaluate their alignment with the ethos of Bitcoin. Assets and products that score higher on this spectrum are generally trust-minimized, reducing reliance on intermediaries and instead relying on transparent and resilient code.

This shift reduces counterparty risk because reliance shifts from off-chain intermediaries to code. The transparency of code increases resilience compared to trusting intermediaries.

This is a development direction worth exploring, and creating native yield options for Bitcoin should be the gold standard and ultimate goal of the Bitcoin community.

Consensus angle

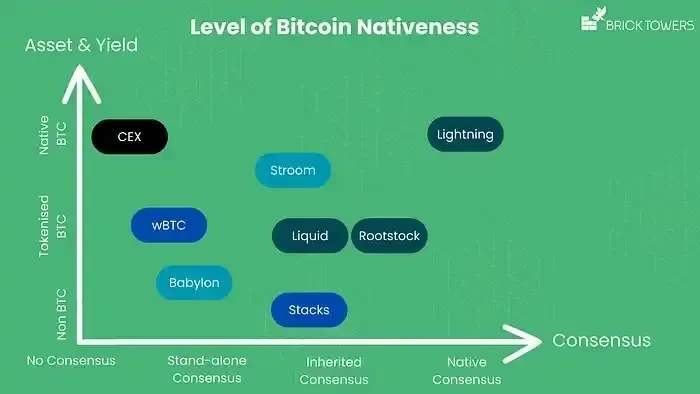

Based on the consensus consistency of the Bitcoin blockchain, Bitcoin income products can be divided into four categories.

No Consensus: This category refers to centralized platforms where the infrastructure remains off-chain. Examples include centralized platforms such as Celsius or BlockFi, which fully control the users assets, exposing users to counterparty risk and dependence on intermediaries. Although these platforms use Bitcoin, their revenue strategies are mainly executed off-chain through traditional financial mechanisms. While these platforms are a step towards Bitcoin adoption, they are still highly centralized and resemble traditional financial institutions, but often lack regulation.

Independent consensus: In this category, the infrastructure is decentralized and represented by public blockchains such as Ethereum, BNB Chain, Solana, and others. These blockchains have their own consensus mechanisms independent of Bitcoin and are not explicitly tied to Bitcoin’s consensus.

Inherited consensus: In this category, the infrastructure is decentralized and represented by distributed consensus on Bitcoin sidechains or Layer-2 solutions. While these sidechains have their own consensus mechanisms, they are designed to align more closely with the Bitcoin blockchain. Examples include federated sidechains like Rootstock, Liquid Network, or Stacks.

Native consensus: This category relies on Bitcoin’s own consensus mechanism as the underlying security model. It does not use a separate blockchain or sidechain, but instead leverages off-chain state channels that are cryptographically linked to the Bitcoin blockchain. The Lightning Network is an important example of this approach, providing a high degree of trust minimization by relying entirely on Bitcoin’s consensus.

The closer a Bitcoin yield product is to Bitcoin’s native consensus, the better it fits with Bitcoin and is generally considered to be more trust-minimized. However, there are subtle differences in the degree of decentralization and security of the infrastructure within the two categories of independent consensus and inherited consensus.

Overall, no consensus offers the lowest levels of decentralization and trust minimization, while native consensus is considered to offer the highest level of trust minimization, although considerations of consensus security and decentralization require further analysis.

Source: Brick Towers

Asset perspective

When considering the assets used in Bitcoin income products, their compatibility with Bitcoin can be divided into three categories.

Non-BTC: This category includes solutions that use assets other than BTC, resulting in a lower alignment with Bitcoin. An example is Stack’s overlay option, where Stack’s native token STX is used to generate yield in BTC.

Tokenized BTC: Here, the asset used is a tokenized version of BTC, which improves the alignment with Bitcoin compared to non-BTC assets. Tokenized BTC can be found on public blockchains such as Ethereum (WBTC, renBTC, tBTC), BNB Chain (wBTC), Solana (tBTC), etc. In addition, tokenized BTC is hosted on Bitcoin sidechains with inherited consensus mechanisms, such as sBTC, XBTC, aBTC, L-BTC, and RBTC.

Native BTC: The asset in this category is Bitcoin (BTC) on-chain, without any tokenized version involved, providing the highest level of Bitcoin fit. Various CEX solutions and Babylons Bitcoin staking protocol directly utilize BTC. Babylon aims to expand Bitcoins security by adapting the Proof of Stake mechanism for Bitcoin staking. In addition, projects like Stroom Network use the Lightning Network to achieve liquid staking, where users can earn Lightning Network income by depositing BTC and minting wrapped tokens such as stBTC and bstBTC on EVM-based blockchains for use in the broader DeFi ecosystem.

Source: Brick Towers

Revenue Perspective

When looking at the yield aspect of Bitcoin income products, the question of compatibility with Bitcoin comes up, leading to a similar categorization as on the asset side: non-BTC, tokenized BTC, and native BTC.

Non-BTC Yield: Babylon provides yield through the native assets of its Proof-of-Stake (PoS) blockchain, which enhances the security of the blockchain through Babylon’s staking mechanism.

Tokenized BTC yield: Stroom Network offers yield in the form of lnBTC tokens. Sovryn, running on Rootstock, facilitates Bitcoin lending by using tokenized BTC (RBTC) as yield. On Liquid Network, Blockstream Mining Note (BMN) offers yield in BTC or L-BTC upon maturity, providing qualified investors with access to Bitcoin hashrate through EU-compliant USDT security tokens.

Native BTC Yield: Stacks offers various options, including yield paid in tokenized BTC in certain yield applications, leveraging sBTC. However, for Stacks’ stacking options, yield accumulates in native BTC. Similarly, some CEXs offer centralized yield products that distribute native BTC as yield to users.

Source: Brick Towers

Bitcoin’s Gold Standard: Localization Throughout

Considering the ideal Bitcoin-based yield product, a gold standard product would combine the following three features: native Bitcoin consensus, native Bitcoin assets, and native Bitcoin yields. Such a product would mimic a near-perfect Bitcoin fit.

Currently, such solutions are only beginning to be built. One project that is actively developing is Brick Towers. Their vision of an ideal Bitcoin-based yield product encompasses achieving a near-perfect Bitcoin fit by incorporating native Bitcoin consensus, assets, and yields. Brick Towers focuses on Bitcoin as a long-term savings solution and aims to provide customers with a minimal trust dependency and native approach to leveraging Bitcoin.

Their planned solution revolves around generating native yield in Bitcoin, leveraging Brick Towers’ automated services for other nodes in the Lightning Network. Solving economics through optimization algorithms, capital is strategically deployed to meet the liquidity needs of other network participants, thereby optimizing capital efficiency while minimizing counterparty risk.

This approach not only facilitates the growth of the Lightning Network, but also increases the utility of Bitcoin as an asset, while providing customers with a seamless and secure way to earn yield on their Bitcoin holdings. Importantly, Brick Towers’ solution avoids the use of wrapped coins, further reducing counterparty risk and reinforcing their commitment to the Bitcoin native ecosystem.

This article is sourced from the internet: Can Bitcoin Be a Productive Asset?

Related: WSJ exposes DWF Labs for suspected market manipulation, Binance denies the allegation

Original article: Binance denies reports of DWF Labs market manipulation By Zoltan Vardai Compiled by: Odaily Planet Daily Husband On May 9, the Wall Street Journal reported that an anonymous source claiming to be a former Binance insider said that Binance investigators discovered that DWF Labs had conducted $30 billion worth of fake transactions during 2023. When asked about instances of market manipulation, Binance denied the reports. A Binance spokesperson told Cointelegraph: “Binance strongly denies any suggestion that its market surveillance procedures allow for market manipulation on our platform. We have a robust market surveillance framework that identifies and takes action against market abuse. Any user who violates our Terms of Use will be removed; we do not tolerate market abuse.” According to the Wall Street Journal, DWF Labs manipulated…