White House Does the Math: How Much More Could Banks Lend if Stablecoin Interest Were Banned?

Last summer, as the U.S. Congress debated the GENIUS Act, economist Andrew Nigrinis threw out a figure—if stablecoins could pay interest, bank lending could evaporate by $1.5 trillion.

That number spread quickly in Washington. Banking lobbyists used it as an argument, some lawmakers used it as a rationale, and the final bill included an explicit prohibition: no stablecoin issuer shall pay interest or yield to holders. The logic was straightforward—if you can earn more money on-chain, who would keep money in a bank? With fewer deposits, banks have less ammunition, and borrowers suffer.

Sounds reasonable, right?

However, the GENIUS Act did not explicitly restrict third-party platforms from offering interest-like yields. But parts of the currently proposed CLARITY Act seek to close this loophole.

In April of this year, the White House Council of Economic Advisers (CEA) released a research report saying: wait, that claim might be a bit overblown. The CEA directly addressed this logic using a full equilibrium model and arrived at a potentially surprising conclusion: prohibiting stablecoin yield payments has a very small effect on protecting bank lending.

The number they calculated: $2.1 billion, not $1.5 trillion—a difference of nearly 700 times.

Where Does a Dollar Go When It Enters a Stablecoin?

The notion that “stablecoins suck deposits away” paints a vivid picture, but it skips a crucial step—what does the issuer do with that money after it’s used to buy the stablecoin?

The CEA breaks it down into three scenarios:

Scenario 1: The issuer buys Treasury bonds with the reserves:

A user withdraws $1 from Bank A to buy a stablecoin. The issuer receives that $1 and immediately buys a Treasury bond from a dealer. The dealer sells the bond and deposits the received $1 into Bank B. Final result: Bank A loses one deposit, Bank B gains one deposit. The total amount of deposits in the banking system remains unchanged; it just changes ownership between banks.

Scenario 2: The issuer deposits the reserves as cash in a bank, but the bank is required to hold 100% reserves against it:

Again, $1 enters the stablecoin system, and the issuer deposits it into Bank C. Bank C’s on-book deposits don’t change, but regulations require Bank C to back this deposit with 100% central bank reserves—meaning that $1 is “locked up” and cannot be multiplied into loans through the credit multiplier. This is the true “loss of bank lending capacity.”

Scenario 3: Reserves flow into a money market fund:

If the fund buys Treasuries, the logic reverts to Scenario 1.

If the fund deposits the cash into the Fed’s Overnight Reverse Repo Facility (ON RRP), that money becomes a Fed liability, no longer a commercial bank deposit—but the CEA points out this phenomenon is common to the entire non-bank financial system, not unique to stablecoins.

Therefore, the core issue isn’t the total amount of deposits, but the structure of deposits—what proportion of stablecoin reserves actually ends up in that “100% reserved, non-lendable” pocket?

The CEA breaks this down. The two largest issuers in the market today, Tether and Circle, together account for over 80% of the stablecoin market share. What they do with the dollars they receive from users is essentially one thing: buy U.S. short-term Treasury bonds. Circle’s reserve report from the end of 2025 shows that 88% of USDC reserves are held in Treasury bonds and repurchase agreements, with only 12% held as bank deposits. Tether is even more extreme; out of its $147.2 billion in reserves, bank deposits amount to only $34 million, not even a rounding error.

The only scenario that truly affects bank lending capacity is when an issuer deposits reserves in a bank and regulations require that bank to hold 100% reserves against that money. In other words, only 12% of Circle’s USDC reserves follow this path. The remaining 88% continues to circulate within the banking system.

Even If It Leaks Out, It’s Caught by Three Nets

Assuming stablecoins no longer pay interest, users start moving money back to banks. But for that capital to become actual bank loans, it must pass through three barriers.

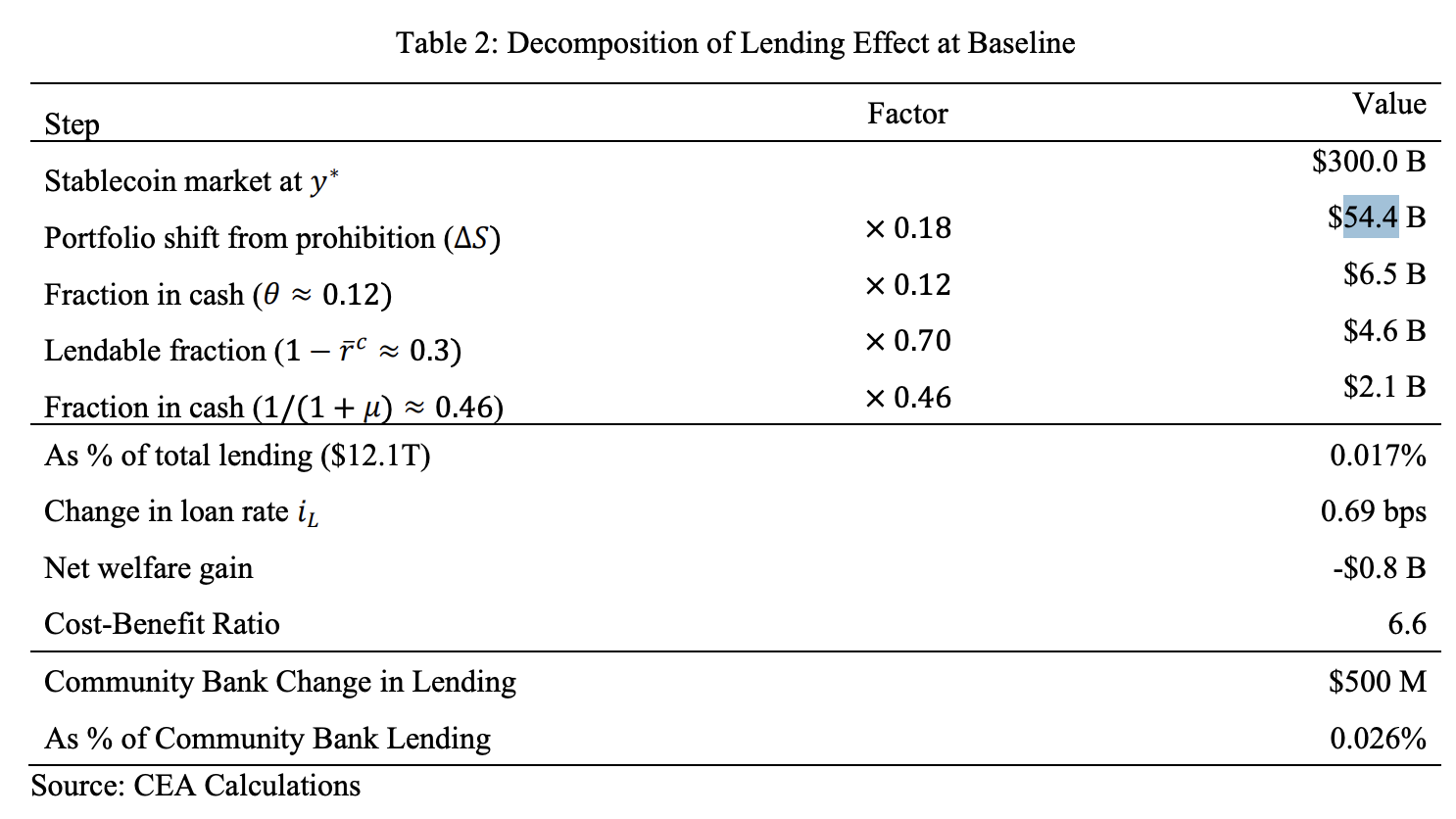

First barrier: How much capital would actually flow back to banks? The report, referencing historical elasticity data from money market funds, estimates that under a baseline scenario, approximately $54.4 billion would shift from stablecoins back to traditional deposits due to yields dropping to zero. This figure itself is already high—a significant portion of stablecoin holders aren’t in it for the yield at all; they want the speed of cross-border transfers or a dollar account independent of their domestic banking system. Whether they earn interest has little impact on their decision.

Second barrier: Out of that $54.4 billion, how much actually changes bank lending capacity? Only the 12% portion (in the case of USDC), which is about $6.5 billion. The other 88% circulates in the Treasury market both before and after the ban, having no net impact on bank lending capacity.

Third barrier: Can the $6.5 billion entering banks be fully lent out? No. Banks need to hold reserves. The current effective reserve ratio in the U.S. banking system is about 30%, leaving 70% as lendable funds. Furthermore, the Fed currently maintains an “ample reserves” framework, with banks already holding over $1 trillion in excess liquidity buffers—for every new dollar of lending capacity, less than 50 cents ultimately becomes a real loan, with the rest being actively absorbed by banks into their liquidity buffers.

After passing through these three barriers, $54.4 billion becomes $2.1 billion, representing only 0.02% of total loans (approximately $12 trillion).

Then, calculate the cost on the other side: stablecoin holders lose the roughly 3.5% annualized yield they could have earned, resulting in a net welfare loss of about $800 million per year.

In the CEA’s words, the cost-benefit ratio of this prohibition is 6.6, meaning the cost is 6.6 times the benefit—a very poor trade-off.

How Was That $1.5 Trillion Calculated?

Since the White House model yields $2.1 billion, where did the original $1.5 trillion figure come from?

The CEA traces its origins in the report. Nigrinis’s (2025) estimate directly borrowed the model established by Whited, Wu, and Xiao (2023) for Central Bank Digital Currency (CBDC)—where CBDC, as a Fed liability, directly withdraws deposits from the commercial banking system, reducing bank loans by about 20 cents for every dollar entering. Nigrinis directly applied this multiplier to the stablecoin scenario, while also assuming stablecoins would expand massively after offering competitive yields, ultimately deriving the $1.5 trillion loan contraction.

The problem lies in a fundamental difference between CBDC and stablecoins: CBDC is a central bank liability; deposits entering it leave the commercial banking system. Stablecoin reserves, for the most part, flow back to commercial banks through the Treasury market. Nigrinis’s model didn’t track where that money went; it only saw deposits decreasing at one bank, not increasing at another.

This is the fundamental difference between partial equilibrium and general equilibrium. Treating one bank’s loss as the entire system’s loss naturally results in an error of orders of magnitude.

Another Overlooked Account

The report specifically highlights an effect not covered by the model but pointing in the opposite direction: stablecoin-driven foreign demand for U.S. Treasury bonds.

Over 80% of stablecoin transactions occur outside the U.S., driven by ordinary users in countries with unstable currencies using dollar stablecoins as savings tools. This group underpins real demand for U.S. Treasuries. IMF data shows that the scale of U.S. Treasury holdings by stablecoin issuers already exceeds that of Saudi Arabia. BIS research indicates that every $3.5 billion inflow into stablecoins can depress the 3-month Treasury yield by 5 to 8 basis points. If a prohibition suppresses stablecoin adoption, this foreign demand channel contracts, raising U.S. Treasury financing costs—a cost that could directly offset the marginal gains on the bank lending side.

So, what does all this actually demonstrate?

It’s not that stablecoins have no impact on banks, but rather that the source of that impact, to a very large extent, is not “whether they can pay interest.” The truly critical factor is what proportion of a stablecoin issuer’s reserves are placed in that 100%-reserved safe. If regulations push that proportion higher in the future, the impact would start to become significant.

Regarding the interest payment prohibition: for bank lending, the cost-benefit ratio is 6.6; for the stablecoin ecosystem, it removes its ability to offer competitive yields to ordinary users; for U.S. Treasury financing, it might even be counterproductive.

A piece of legislation with no clear beneficiaries, but with clear losers. That is the real point for reflection in this report.

This article is sourced from the internet: White House Does the Math: How Much More Could Banks Lend if Stablecoin Interest Were Banned?

The next day, as soon as the Asian market opened, crude oil prices dropped by about 15%, with WTI falling below $100. According to Reuters citing LSEG transaction data, the scale of this short position was “completely atypical for that time period.” Representative Ritchie Torres wrote to the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) on April 8, requesting an investigation. This was not the first time. More precisely, it was the second recorded instance of the same “playbook” since the current US-Iran conflict began. The Same Trading Signature, Two Precise Hits The one on the morning of Monday, March 22, 2026, was not as famous as the April 7 event because it did not trigger a sharp drop in oil prices. However, in…