Tiger Research: A 10,000-Word Analysis of Crypto’s Most Profitable Business and Its Models

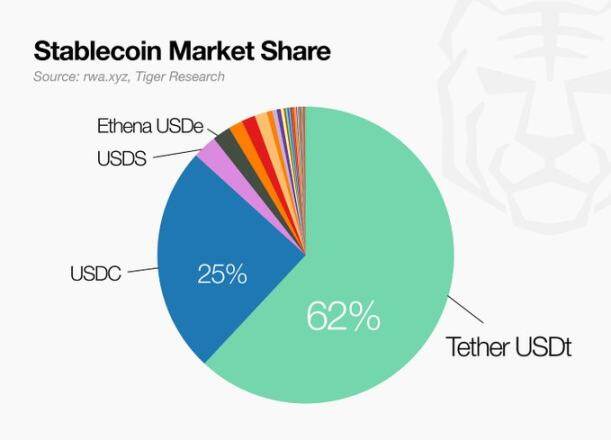

However, with Tether (USDT) and USDC collectively holding over 85% of the market share, it is unrealistic for new entrants to compete on the same reserve interest model.

This report analyzes four issuers who have each carved out a unique position within this landscape.

Tether leads with approximately 62% market share. Building on the core reserve yield model, the company is rebuilding trust and diversifying revenue by introducing audits from a Big Four accounting firm and deploying $20 billion into new business investments.

StraitsX does not rely on reserve interest as its primary revenue source, focusing instead on payment processing fees. Its integrations with Alipay+, GrabPay, and Visa demonstrate real-world utility, while monthly transfer volumes reaching 2.5 times its market capitalization validate the model’s viability. Obtaining a Major Payment Institution license from the Monetary Authority of Singapore earlier than competitors has turned regulatory requirements into a competitive moat.

M0 does not directly issue stablecoins. Instead, it provides shared infrastructure enabling other companies to launch their own stablecoins. MetaMask and Exodus already operate stablecoins on the platform. As more issuers and builders join, the model strengthens through network effects.

KRWQ operates in the absence of a domestic regulatory framework, first capturing offshore demand from the already-functioning Korean won non-deliverable forward market. Once a regulatory framework is established, the company plans to leverage its pre-built offshore liquidity to enter the Korean domestic market, subsequently replicating the model for other major Asian NDF currencies.

The stablecoin issuance market is not converging on a single business model but is instead fragmenting. Fundamentally different revenue strategies can coexist based on each issuer’s scale and positioning.

Stablecoin Issuance سوق

Stablecoin issuance is one of the most profitable businesses in the تشفير space, attracting an increasing number of institutional participants.

Tether pioneered and dominated this field, taking a leading position as the primary liquidity provider in early trading markets. Circle followed, prioritizing regulatory compliance and expanding its influence into traditional finance with its listing on the New York Stock تبادل in June 2025.

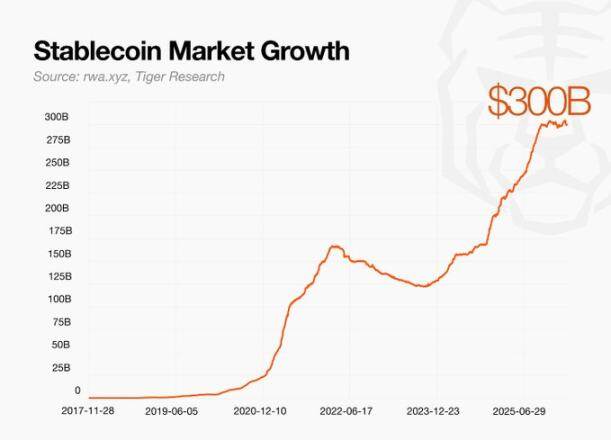

This institutionalization has pushed the total stablecoin market capitalization to approximately $300 billion and prompted major jurisdictions to formalize regulatory frameworks. The US signed the GENIUS Act in July 2025, establishing the first federal regulatory framework for payment stablecoins. The EU implemented the Markets in Crypto-Assets Regulation, and Hong Kong enacted its Stablecoin Ordinance, marking the full launch of global regulatory competition.

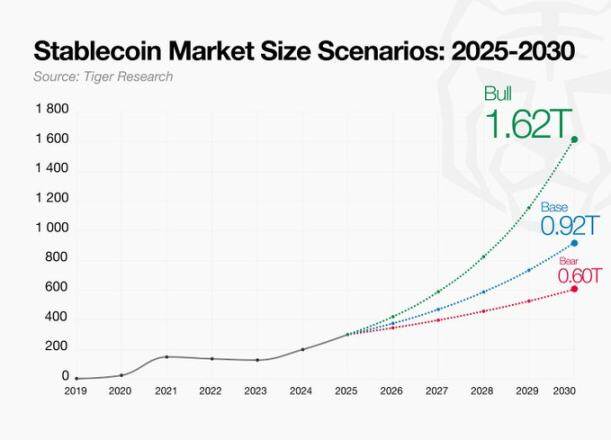

This growth momentum is expected to accelerate further. Tiger Research analysis shows the annual net supply increase of stablecoins nearly doubled from $55 billion in 2024 to $101 billion in 2025. If major jurisdictions complete relevant legislation and institutional demand materializes, the market size is projected to exceed $600 billion by 2030, even under a conservative 15% annual growth assumption.

The core revenue model for stablecoins lies in reserve management, not the issuance act itself. When a user deposits $1, the issuer mints 1 USDT or USDC and allocates that dollar to low-risk assets like US Treasuries or money market funds. As issuance scales, the reserve base and its generated interest income grow.

This model is inherently a scale game. Generating meaningful revenue from reserve interest requires tens of billions in circulation. Currently, USDT (~62%) and USDC (~25%) collectively hold over 85% market share, with the remaining 15% fragmented among dozens of smaller issuers. For latecomers, competing solely on the reserve interest model is unrealistic.

New entrants are responding by designing alternative revenue models or fundamentally reتحديning the business. Some focus on payment fees and integration with the real economy as primary income; others provide issuance infrastructure rather than issuing directly, earning network service fees; some choose to first capture offshore demand in less regulated currency areas before entering the domestic market once frameworks mature.

The stablecoin issuance market is not converging but diverging. Fundamentally different revenue strategies can coexist based on each issuer’s scale and positioning. The following sections analyze how these models operate in practice, based on interviews with key players.

Tether: The Market Benchmark for Stablecoins

Tether first issued the USD-pegged stablecoin USDT in 2014 and now holds about 62% of the stablecoin market share, effectively serving as the industry pioneer.

Tether’s ability to maintain market leadership for a decade is not solely due to first-mover advantage. What built Tether today is a series of proactive, deliberate structural shifts: overhauling reserve composition from commercial paper to US Treasuries; establishing quarterly external attestations; and transitioning to a diversified business model, reinvesting profits from stablecoin operations into areas like AI, energy, education, and communications.

نموذج الأعمال

Tether’s revenue sources are diverse, but reserve management remains its core.

Each time Tether issues USDT, it receives an equivalent amount of USD and invests it in safe assets like US Treasuries, reverse repos, and money market funds. As issuance grows, assets under management expand, and interest income accumulates. Additionally, part of the reserves is held in gold and Bitcoin, with price appreciation of these assets generating additional mark-to-market gains. Based on public information, reserve management income constitutes the vast majority of its total profit.

Secondary revenue sources include protocol integration fees and transaction fees. Furthermore, Tether maintains a strategic investment portfolio separate from USDT reserves, covering areas like AI, energy, and communications.

Regulatory Engagement

Since Q1 2025, Tether has held a stablecoin issuer license under El Salvador’s Digital Assets Law and operates under the supervision of the National Digital Assets Commission. However, some view this structure as limiting transparency. S&P has cited this as one reason for giving USDT a lower transparency score.

Tether is addressing this by entering the US market separately. Under the GENIUS Act framework, the company launched USAT, a product line specifically designed for the US regulatory environment, while USDT continues as the general-purpose product for the global market. These two markets are structurally independent and progressing in parallel.

Tether is also actively responding to transparency controversies. While quarterly reserve attestation reports verified by BDO have been its baseline practice, Tether formally engaged a Big Four accounting firm in March 2026 to conduct a full audit of USDT reserves. Unlike attestations that confirm reserve composition at a point in time, a full audit covers assets, liabilities, and internal control systems to a higher scrutiny standard.

The market has reacted. As Tether’s regulatory compliance improved, Circle’s stock price fell by approximately 20%. This indicates Tether is addressing what was previously its main competitive weakness, reshaping the competitive landscape.

Growth Strategy

Tether’s growth strategy focuses on real-world asset expansion, technological innovation, and new business development. Its flagship real-world asset product is Tether Gold, a token backed 1:1 by physical gold stored in Swiss vaults. This product holds over half of the total market capitalization for gold-backed stablecoins, and its underlying asset size continues to grow.

New business expansion is also progressing. Tether’s proprietary investment portfolio exceeds $20 billion, widely distributed across AI, energy, media, and communications. This portfolio is entirely separate from USDT reserves, serving as a growth engine for surplus capital, reinvesting profits from stablecoin issuance into long-term growth drivers.

الماخذ الرئيسية

Tether’s case offers several structural insights for any entity considering entering the stablecoin business.

First, stablecoin issuance is a scale business. Each issued USDT corresponds to an investment in US Treasuries. As issuance grows, Treasury holdings increase, and interest income rises. Understanding this direct link between issuance and assets under management is the starting point for analyzing any stablecoin business model.

Second, regulatory compliance is a prerequisite, not an option. Even Tether must operate within a regulatory framework. Regardless of how unclear current frameworks are, business structure design must factor in eventual regulatory inclusion from the start. Stablecoins are inherently an industry that operates within regulation.

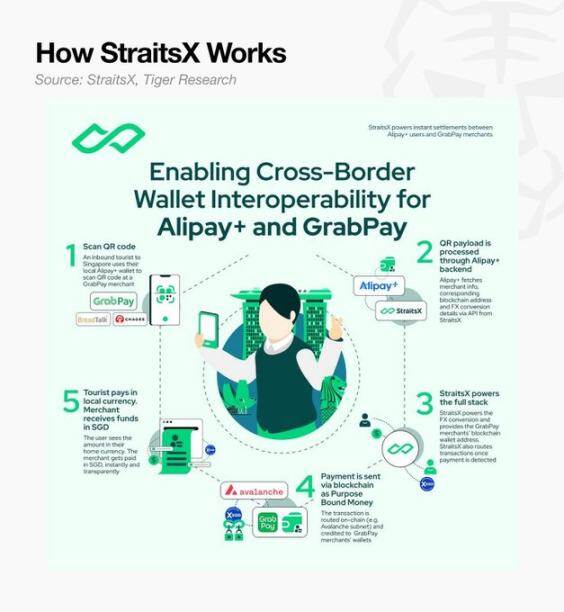

StraitsX: A Stablecoin Issuer for the ASEAN Real Economy

StraitsX is a Singapore-based stablecoin issuer. Its core products are XSGD (pegged to the Singapore Dollar) and XUSD (pegged to the US Dollar), and it has expanded to other major ASEAN currencies like the Indonesian Rupiah.

What’s noteworthy is not just its digital asset issuance: StraitsX is building payment infrastructure directly connected to the ASEAN real economy. According to on-chain data platform rwa.xyz, XSGD’s monthly transfer volume (~$39.9M) is about 2.5 times its market capitalization (~$15.8M).

Compared to global mainstream stablecoins like USDT and USDC, StraitsX’s absolute asset size and turnover are still smaller, but its use case is fundamentally different. Mainstream stablecoins are primarily used for investment trading on crypto exchanges, while StraitsX’s tokens are used for daily real commercial activities. The data indicates its issued tokens are not idle in investor wallets but are continuously circulating in the market.

StraitsX is seen as specialized payment infrastructure for ASEAN not just due to on-chain metrics, but more importantly, its strong capability to integrate with enterprise B2B payment networks.

نموذج الأعمال

StraitsX’s revenue model centers on payment processing fees. Reserve interest income is constrained by external variables like circulation and interest rates, while payment fees are tied to transaction volume, scaling directly with business growth.

Reserve Interest Income: Reserves corresponding to circulating XSGD and XUSD are held in trust accounts at DBS, Standard Chartered, and United International Bank. Per MAS regulations, interest accrues to the company, not token holders. Based on an estimated total circulation of ~$65M, annual revenue is estimated at $2.6M to $3.25M.

Payment Processing Fees: Generated each time stablecoins are used for payment or settlement. Main channels include on/off-ramps, QR code payment networks (integrations with Alipay+ and GrabPay), and card issuance (Visa BIN sponsorship). This income is tied to transaction volume, not rates.

OTC & FX Swap Spreads: Foreign exchange spreads earned from swaps between stablecoins, buy/sell trades, and bulk OTC transactions.

Among these, payment fees are primarily generated through StraitsX’s external network integrations. Major mobile payment platforms like Alipay+ and GrabPay, as well as global exchanges like Binance and Bybit, have adopted StraitsX’s system for fund settlement, covering various use cases. Notably, internal StraitsX data shows stablecoin payments linked to Visa cards grew 40x over the past year, with card issuance growing 83x in the same period.

Regulatory Positioning

The crypto industry generally views strict regulation as limiting business expansion. StraitsX has taken the opposite path, turning MAS’s regulatory framework into a competitive defense.

The foundation of this strategy is StraitsX’s MAS Major Payment Institution license. With this license, StraitsX is authorized to operate six of the seven major payment services regulated by MAS. This allows the company to legally conduct cross-border remittances, FX exchange, merchant payments, and account issuance within a single legal entity, far beyond mere token issuance. XSGD and XUSD have been recognized as stablecoins substantially compliant with MAS’s single-currency stablecoin regulatory framework.

For institutional capital to enter the blockchain ecosystem at scale, bank-grade KYC/AML systems are a basic prerequisite. Most crypto companies operating outside regulatory perimeters cannot meet this standard.

StraitsX is co-developing a next-generation cryptographic identity verification system with regulators. Its strategy is to pre-emptively meet the compliance standards required for future institutional capital inflows, ensuring it can exclusively capture that capital.

Growth Strategy

After establishing a sustainable revenue model, StraitsX’s next goal is to enter new settlement markets. Its long-term growth driver primarily comes from real-world asset settlement. As traditional assets like stocks and bonds migrate on-chain, demand for tokenized cash as a settlement medium will grow accordingly. StraitsX plans to capture institutional settlement demand by offering cross-chain interoperability across multiple blockchain environments.

الماخذ الرئيسية

StraitsX’s case shows that long-term growth drivers primarily come from real-world asset settlement. As traditional assets like stocks and bonds move on-chain, demand for tokenized cash as a settlement medium will grow in tandem. StraitsX plans to capture institutional settlement demand early by providing cross-chain compatibility across multiple blockchain environments.

First, turnover is more important than total volume. Non-USD stablecoin issuers cannot grow solely on issuance size. Prioritizing real use cases and integrating into B2B settlement networks is essential. The key metric is turnover, not market cap.

Second, regulatory compliance is a competitive moat. StraitsX secured its MAS license early, turning regulatory requirements into a structural barrier to entry. Stablecoins sit at the intersection of crypto and traditional finance, inherently a regulated industry. The speed at which an issuer achieves compliance and the closeness of its collaboration with regulators will be key variables determining competitive success.

M0: Shared Infrastructure for Stablecoin Builders & Issuers

M0 provides shared infrastructure that enables businesses to launch stablecoins and financial institutions to issue stablecoins.

M0 does not directly issue stablecoins but provides infrastructure allowing multiple builders to launch their own stablecoins on a common technical foundation.

This architecture solves two core problems. First, the stablecoin market is fragmented, with each issuer running its own independent issuance tech stack, making cross-currency compatibility structurally difficult. Second, without M0, stablecoin builders face a “cold start” problem: they must build liquidity, partnerships, and network effects for their stablecoin from zero on day one.

M0 solves both with a shared layer. Every stablecoin on the platform is built on common standards and technology, sharing existing liquidity from launch and being 1:1 exchangeable with all other M0-powered stablecoins on the platform.

Current stablecoins built on M0 infrastructure include MetaMask’s mUSD, Exodus’s XO Cash, KAST’s USDK, Noble’s USDN, Usual’s UsualM, with more in development. Issuers powered by M0’s issuance stack include Bridge (a Stripe company), MoonPay, and 1Money.

نموذج الأعمال

Issuers: Regulated entities that hold reserves as collateral, use M0 infrastructure to mint stablecoins, and pay an agreed fee to the platform from a portion of the interest earned on reserves.

Builders: Entities with specific use cases that use M0 to launch and control their own stablecoins, capturing economic benefits and directly customizing the currency’s operation into their products.

هذا المقال مصدره من الانترنت: Tiger Research: A 10,000-Word Analysis of Crypto’s Most Profitable Business and Its Models

Related: ETF Outflows $4.5 Billion: Will BTC Drop Another 30% in the Next 3 Months?

The article cross-validates using three sets of data from Glassnode, Santiment, and CryptoQuant, proposing three future scenarios, providing a suitable reference framework for judging BTC’s current trajectory. The full text is as follows: Bitcoin’s network activity has been weakening for six consecutive months, but this trend is not reflected in the core metrics that many traders first look at. The clearer signal is not trading volume—which has remained largely stable—but the breadth of participation. Even as the network continues to process a similar number of transactions, the number of active on-chain addresses has been steadily declining. In a market where price discovery increasingly occurs on ETFs and derivatives, this split is crucial. It means: Bitcoin’s on-chain footprint is narrowing, while market exposure remains active elsewhere. As the bear market persists,…