AI Triggers MLCC Super Cycle: How Long Can Samsung Electro-Mechanics Enjoy the Dividend?

Introduction

Morgan Stanley has just raised its target price for Samsung Electro-Mechanics from 920,000 KRW to 2,560,000 KRW. Analysts have rewritten the narrative for MLCCs (Multilayer Ceramic Capacitors) from a cyclical industry to one of structural prosperity. The core logic is straightforward: AI servers are 10 to 15 times more voracious for MLCCs than traditional servers.

AI Ignites ‘Volume and Price Growth’

An AI server requires 440,000 MLCCs. What about a traditional server? 30,000 units. That’s a difference of over ten times.

It’s not just a matter of quantity. The demands on MLCCs from AI are also upgrading: higher capacitance, smaller size, lower ESL and ESR. The evolution is shifting from competing on volume to competing on quality, driving up the ASP (Average Selling Price). Morgan Stanley states that Samsung Electro-Mechanics’ MLCC business will contribute 15% of revenue by 2026, and this proportion will jump directly to over 50% by 2030. Behind this lies enhanced pricing power, leading to real earnings expansion.

Supply Tightness is Structural, Not Cyclical

This round has some similarities to the MLCC super cycle of 2017-2018, but the underlying logic is completely different. That time was a short-term mismatch of inventory shortages and an order surge. This time, it’s a production capacity ceiling meeting continuously growing new demand.

Production lines for high-end MLCCs are already fully booked, and building new lines takes two years to become operational. Inventory levels in the supply chain have now spilled over from the spot market to contract prices, with distributors starting to hoard inventory, indicating they no longer see this as a temporary shortage.

Morgan Stanley expects MLCC prices to rise by 30% in the second half of 2026, and another 30% to 50% in 2027. This isn’t a prediction from a futures trader but a conclusion derived from currently observable contract prices and distributor behavior.

Why Samsung Electro-Mechanics is the Biggest Beneficiary

Samsung Electro-Mechanics benefits along three dimensions.

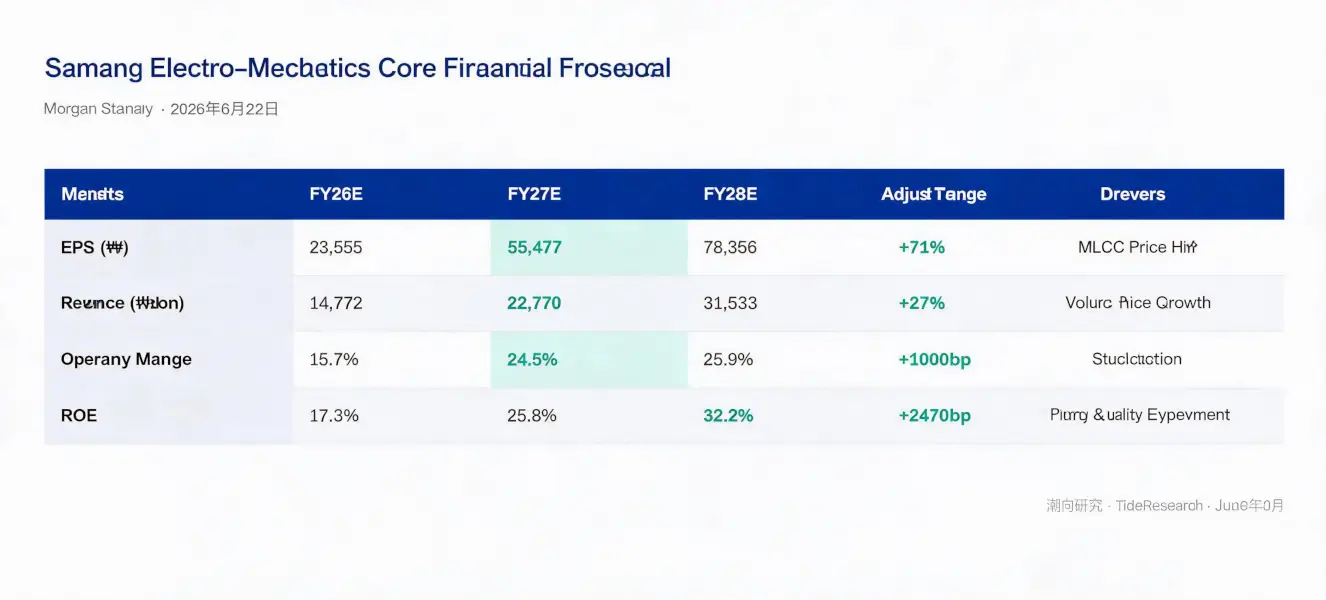

First is the direct price increase of MLCCs. MLCCs for IT are rising, MLCCs for AI are also rising, and the profit margins on the AI side are thicker. When the 1Q26 earnings are released, revenue has already exceeded expectations at 3.2 trillion KRW versus the 3.1 trillion KRW estimate. More importantly, Morgan Stanley has raised its EPS forecasts for the next three years across the board, with FY27E reaching 55,477 KRW, 71% higher than before. The operating profit margin is expected to jump from the current 15.7% to 24.5% by 2027, and further to 25.9% by 2028. This is not a numbers game; it’s real earnings expansion driven by enhanced pricing power.

Second is the ABF substrate business. Orders for ASIC chips from AI customers are already at capacity, and Samsung Electro-Mechanics’ shipments and profits in this area are growing rapidly.

Third are new product lines. Silicon capacitors have secured $1.3 billion in orders, and glass substrates have begun trial production. These won’t contribute revenue this year or next, but they lay the groundwork for the coming years.

Will ROE Really Jump from 7.5% to 32.2%?

Morgan Stanley assumes that Samsung Electro-Mechanics’ ROE (Return on Equity) will rise from 7.5% in FY25 to 17.3% in FY26, and then to 32.2% in FY28. Simultaneously, the company’s dividend payout ratio is expected to increase from the current 5% to 20%.

This means a Korean electronic components company, which already had a decent ROE, could enter a higher profitability cycle due to changes in product mix and pricing power. Currently valued at 1.4 times P/B (Price-to-Book ratio), which is lower than the historical average of 1.7 times. The target price increase from 920,000 to 2,560,000 won, a gain of nearly 178%, is driven not only by net profit growth but also by potential valuation recovery.

Identifying the Risks

Upside risks: MLCC prices are forced to rise significantly further due to genuine shortages; smartphone demand rebounds more strongly than expected; China’s consumer stimulus policies generate additional demand.

Downside risks: A significant downturn in Samsung Electronics’ flagship phone cycle (Samsung Electro-Mechanics has a substantial consumer product exposure); poor execution in expanding among Chinese smartphone customers; weak global consumer demand.

Catalysts? Further increases in contract prices, a rising Book-to-Bill ratio, production capacity utilization nearing full capacity, and confirmation of increased MLCC content from next-generation AI platforms (Rubin, VR200).

The New AI Infrastructure Play

From a supporting player to a main act, from cyclical to structural, from a traditional capacitor maker to an AI infrastructure supplier. This is the story Morgan Stanley tells for Samsung Electro-Mechanics. How long the story lasts depends on the evolution of AI chip demand, capacity construction, and the competitive landscape. But for now, supply constraints support prices, and rising prices support profits.

本文来源于互联网: AI Triggers MLCC Super Cycle: How Long Can Samsung Electro-Mechanics Enjoy the Dividend?

Some people ask, “Can I recover my wallet if I accidentally delete it or forget the password?” Others take a screenshot of their seed phrase and save it in their photo album, thinking it’s safe as long as they don’t share it with anyone. Some still struggle to understand the difference between a trading platform account and a self-downloaded wallet. These questions may seem basic, but in truth, many people who have used wallets for years don’t fully grasp them either. So, I’m planning to start a new series called “Web3 Survival Guide,” aiming to minimize jargon and focus specifically on those seemingly small but genuinely important issues, helping everyone understand and use Web3 step by step. This article is the first installment of the “Web3 Survival Guide,” starting with…