A “Free Lunch” with 400% APY? The Truth Behind Trade.xyz’s Crude Oil Perpetual Negative Funding Rate

At the same time, a rare phenomenon has emerged with the WTIOIL-USDC crude oil perpetual contract on Trade.xyz: the annualized funding rate has stabilized between -300% and -400%. This means that any trader willing to go long at this moment can receive a profit equivalent to 1% of their principal daily, paid from the pockets of short sellers.

The market doesn’t give away money for no reason. To understand this anomalous negative funding rate, we need to start with the basics of futures trading.

Rollover

Crude oil futures are a series of contracts arranged by delivery month. Contracts for May delivery, June delivery, and July delivery each have their own prices. As the front-month contract approaches expiration, the market must shift from the old contract to the new one—this action is called rollover.

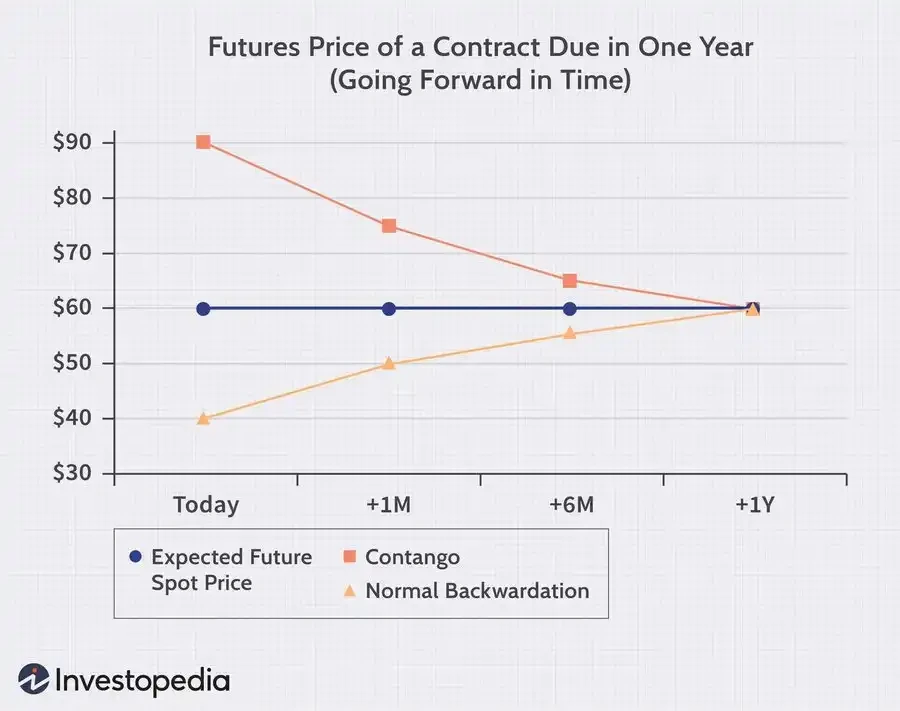

Under normal circumstances, a back-month contract implies that oil merchants will store the oil for several more months, incurring additional storage costs. Therefore, the delivery price should logically be higher. The market calls the phenomenon where future contracts are more expensive than the near-month contract “Contango.” Conversely, the situation where the near-month contract is more expensive than the back-month contract is called “backwardation.” This typically occurs when there is a current shortage and greater demand to receive oil immediately.

During this rollover period for Trade.xyz’s crude oil, the crude oil futures market exhibited precisely this near-high, far-low structure.

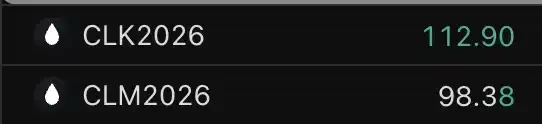

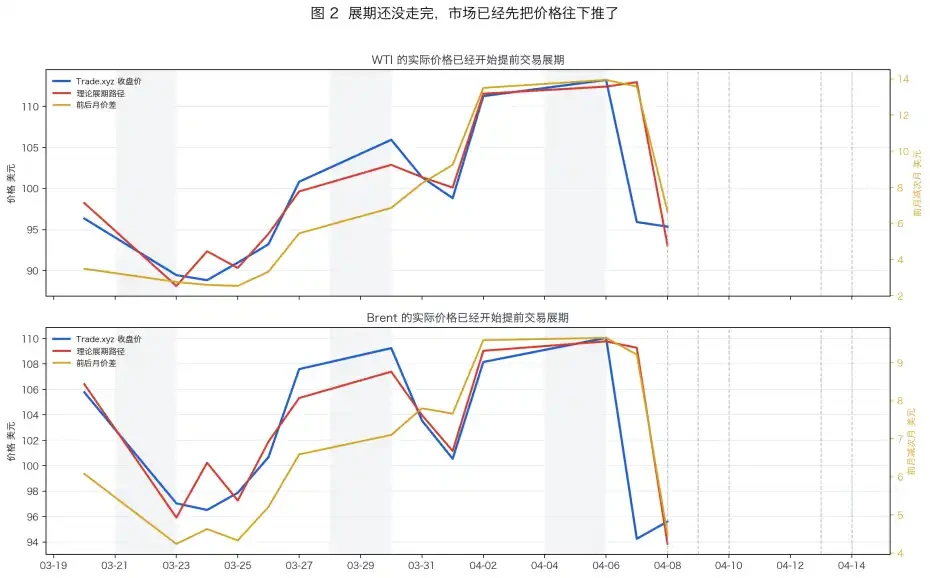

From late March to early April 2026, the WTI crude oil curve was in an extreme state of backwardation. As shown in the chart above, the price of the May contract (near-month) consistently remained significantly higher than the June contract (back-month), with the spread widening to over $14 at one point.

The WTIOIL-USDC perpetual contract on Trade.xyz is anchored by its oracle to this May near-month contract.

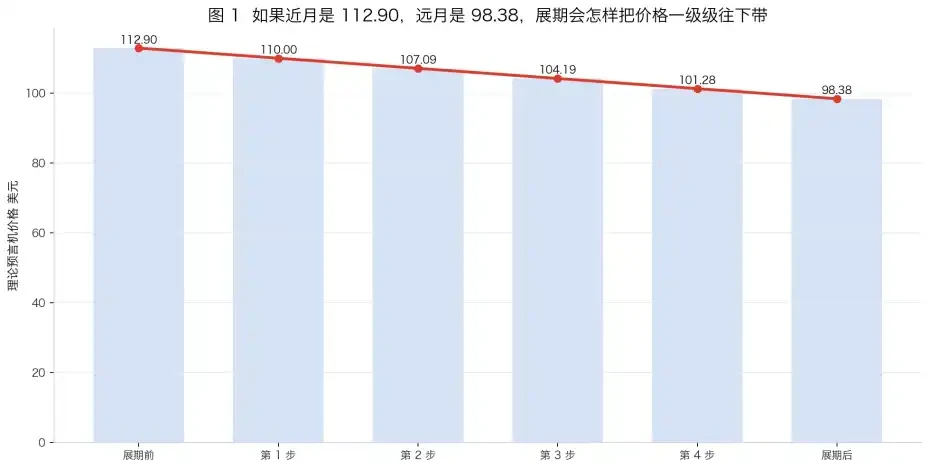

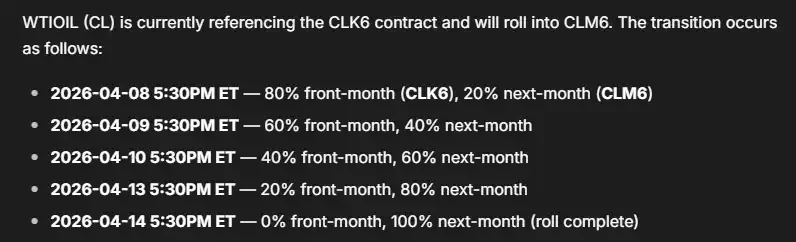

However, we won’t be trading this May contract forever. It must be rolled over to the next June contract. So, how is the rollover accomplished?

According to the Tradexyz documentation, the oracle will use a period of 5 trading days to gradually shift the price weighting from 100% near-month contract to 100% back-month contract.

Against the backdrop of “backwardation,” this means the oracle price on Tradexyz will decline from the near-month price to the back-month price over those 5 trading days.

市场 participants familiar with this mechanism have a clear expectation for the contract price post-rollover. Everyone knows the price will fall, so of course, they swarm to short. As short positions accumulate, the funding rate turns negative, and short sellers start paying long holders.

From the perspective of the no-arbitrage principle, this is normal. The spread between the near-month and back-month contracts provides a profit for short sellers. The funding fee then erodes this profit. The larger the spread, the higher the negative funding rate the market charges.

Once the negative funding fee reaches a certain level, this seemingly obvious arbitrage opportunity will be smoothed out again. The cost for short sellers will completely offset their profit.

Strategies

How can one profit in such a market environment? Here are three common strategies.

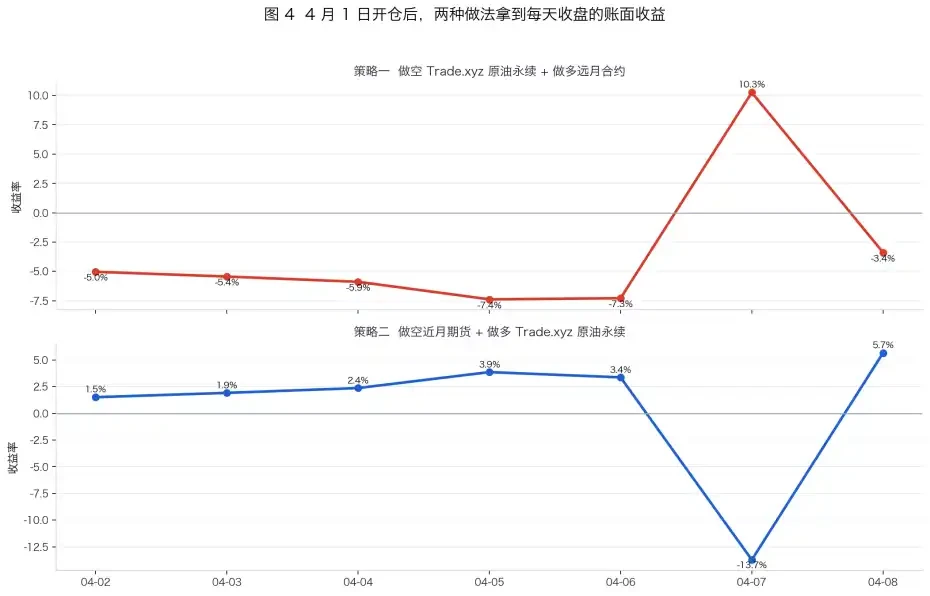

1. Short the crude oil contract on Tradexyz at the current price while going long on the back-month contract on CME.

This appears to be a risk-neutral strategy that can steadily capture the spread, but it fails to consider several factors.

Assume shorting Trade.xyz’s WTI contract at $95.352 on April 8th while going long the June futures contract at $87.75, each with a notional value of $10,000. If both sides eventually converge, theoretically, one could capture the $7.60 spread, resulting in approximately $797 in profit. However, on April 8th, the daily funding rate for the short position had already reached 1.42%. Projecting over the remaining 6 days until rollover completion, the funding fee would cost $851. At this point, the net profit calculation leaves only -$53. This doesn’t even account for trading fees and slippage.

Abraxas Capital began implementing this strategy on March 19th, after the last rollover was completed. Their Brent crude oil position on tradexyz accounted for 20% of the market’s open interest, and they achieved substantial profits early on when the funding rate remained relatively neutral. However, as more arbitrageurs flooded in, the funding fee has already consumed 80% of their arbitrage profits.

The massive position size also means they have difficulty exiting and are forced to passively pay the fees.

2. Short the back-month futures contract, go long the xyz near-month contract, and close the position before the rollover begins.

This trade is almost the counterparty to Strategy 1, betting that the market is over-arbitraged. After April 1st, this strategy could indeed yield profits.

3. Short the xyz contract funding rate on Boros before the rollover begins.

Boros is a market specifically for trading rates (fees), developed by the Pendle team. In Boros’s crude oil contract market, what’s traded is the market’s expectation for the funding fee of Trade.xyz’s crude oil contract over the coming period. If a user believes the negative funding fee will deepen further, they can short the market’s funding rate contract.

However, constrained by slippage costs, position limits, trading fees, and extremely low capital efficiency (supporting only 0.2x leverage), this trade also struggles to achieve the ideal high returns.

Conclusion

The rise of RWA trading platforms like Trade.xyz is pushing a group of “加密 traders” to become “futures traders.” DeFi players are also starting to learn the CME rollover calendar, calculate front-month and back-month spreads, and make decisions based on the rate curves on Boros.

Trading platforms are continuously iterating, and market participants are adapting to the new infrastructure.

本文来源于互联网: A “Free Lunch” with 400% APY? The Truth Behind Trade.xyz’s Crude Oil Perpetual Negative Funding Rate

Related: TAO Subnet Team Praised by Jensen Huang Has Parted Ways with Founder in a Bitter Split

Author|Azuma (@azuma_eth) Remember the story where NVIDIA CEO Jensen Huang praised Bittensor (TAO)? On March 20th, during an appearance on Chamath Palihapitiya’s All-In podcast, Huang was asked about his views on “decentralized AI systems/computing power networks.” Palihapitiya used Bittensor as an example (arguably with some self-interest), mentioning that a subnet team on Bittensor successfully trained a 4-billion-parameter (actually 72-billion-parameter) Llama model, with the entire process completed through distributed computing power collaboration. Upon hearing this, Jensen Huang commented that it was “a pretty remarkable technical achievement.” Boosted by this positive news, TAO surged against the market trend last month, briefly surpassing $370, and Bittensor was hailed by the cryptocurrency industry as “the hope of the entire village.” However, just half a month later, the situation took a sharp turn due to…