Earning $2.7 Billion in Revenue Yet Net Loss: Is Circle Essentially ‘Working for’ Coinbase?

Original Compilation: TechFlow

소개: Circle has been listed on the NYSE under the ticker symbol CRCL. But what exactly is this company’s business? This article, based on its FY2025 annual report, dissects Circle’s revenue structure, reserve model, revenue-sharing arrangement with Coinbase, and the growth status of USDC and EURC layer by layer.

The author’s core conclusion: Circle is essentially an interest rate-sensitive financial infrastructure company, earning revenue from reserve interest, not from software platform subscriptions or transaction fees. This conclusion directly impacts its valuation logic.

Full text is as follows:

The understanding of Circle should first position it as a “reserve revenue company,” not a scaled software or payment fee platform. Its profit model is highly dependent on stablecoin balances, short-term interest rates, and the portion of reserve revenue actually retained after paying substantial distributions.

FY2025 data makes this very clear: Total Revenue and Reserve Revenue combined were $2.747 billion, with Reserve Revenue contributing $2.637 billion and other revenue only $110 million. Therefore, Circle’s recent financial performance primarily depends on three variables: average USDC circulation, actual reserve yield, and the economic structure of partner distribution arrangements (especially the contract with Coinbase).

FY2025 Total Revenue and Reserve Revenue grew strongly from $1.676 billion in FY2024 to $2.747 billion. Reserve Revenue increased from $1.661 billion to $2.637 billion, while other revenue rose from $15 million to $110 million. Despite this, Circle’s FY2025 net loss attributable to common shareholders still reached $70 million, and operating expenses also increased significantly, with compensation expenses as high as $845 million.

Figure: Circle FY2025 Key Financial Metrics

The core debate for 2026 is not whether Circle is expanding its footprint, but whether this expansion can truly be reflected in the financial data. The key variables remain: whether USDC balances can continue to grow, how reserve yields evolve in a declining interest rate environment, whether distribution costs will remain high long-term, and whether the scaling speed of new revenue sources like CCTP, CPN, and USYC can keep up with the growth rate of the reserve revenue base.

At the current stage, Circle’s strategic boundaries are clearly expanding, but the core investment framework remains unchanged: it is still a financial infrastructure company whose earnings are dominated by reserve revenue, not driven by diversified platform monetization, and is highly sensitive to interest rates and balance scale.

Circle Business Overview

Circle is a fintech company listed on the NYSE under the ticker CRCL. The company filed its FY2025 annual report (Form 10-K) for the year ended December 31, 2025, on March 9, 2026. Circle’s FY2025 balance sheet shows “stablecoin holder deposits” of $74.9 billion, a figure that directly indicates: the company’s economic core remains the scale management of reserve-backed stablecoins, not a traditional pure software model.

From an analytical framework, Circle can be broken down into four layers:

First, a stablecoin issuer, with main products being USDC and EURC, where the liability side corresponds to stablecoins in circulation, and the asset side is reserve assets segregated and held for users. Second, the reserve revenue business, which monetizes reserve assets through interest and dividend income. Third, the developer, payment, and infrastructure layer, dedicated to enhancing stablecoin use cases and transaction density. Fourth, a broader strategic layout built around the “Internet Financial System,” including Arc, the Circle Payments Network (CPN), and tokenized asset infrastructure.

However, disclosed data indicates that what truly matters financially at present is still the reserve revenue model, not a scaled software or transaction fee business. FY2025 Total Revenue and Reserve Revenue combined were $2.747 billion, with Reserve Revenue contributing $2.6368 billion, while the non-reserve portion is relatively limited.

This distinction is crucial for valuation. Circle’s strategic narrative is broadening, but the revenue structure still does not support viewing it as a “software platform re-rating” story. Previously disclosed data showed that “other products” revenue accounted for only 1% of total revenue in 2024, though management separately noted that other revenue accelerated growth in 2025, with Q4 2025 other revenue at $37 million, an increase of $34 million year-over-year. This is a positive directional signal but not yet sufficient to shake the core position of reserve balances, reserve yields, and partner economic structure in driving profitability.

Another strategic pillar is regulatory positioning. Circle disclosed that in December 2025, it received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish a national trust bank, tentatively named First National Digital Currency Bank, N.A. Management characterizes this as a significant step to strengthen USDC infrastructure and potentially expand regulated custody and reserve management capabilities. This may enhance regulatory sustainability and institutional confidence in reserve governance, but it should not yet be considered a disclosed profit driver.

Business Model and Economic Structure

Circle’s business model is determined by two variables: the scale of stablecoins in circulation and the yield on reserve assets. The company explicitly 디파이nes reserve revenue as a function of reserve balances and reserve return rates.

FY2025 Reserve Revenue was $2.6368 billion, higher than FY2024’s $1.6611 billion. In contrast, FY2025 other revenue was only $109.8 million (FY2024: $15.2 million), with subscription and service revenue of $84.8 million being the largest non-reserve item. This confirms that Circle’s profit structure is extremely sensitive to interest rates and balance growth, even as auxiliary revenue has begun to grow from a low base.

Reserve management is conservative. Circle disclosed that as of June 30, 2025, approximately 87% of USDC reserves were held in the Circle Reserve Fund—a government money market fund compliant with Rule 2a-7, managed by BlackRock and custodied by BNY Mellon. The remainder is held as cash in accounts serving USDC holders, primarily at global systemically important banks. The logic of reserve construction prioritizes liquidity, capital preservation, transparency, and compliance, not maximizing returns.

Circle’s economic structure is also profoundly influenced by distribution arrangements, especially the agreement with Coinbase. Reserve revenue is recognized on a gross basis, but the company makes substantial downstream payments through distribution and transaction costs. This means a significant portion of gross reserve earnings is distributed through the distribution layer per contract before reaching operating expenses.

This is reflected in the data: FY2025 Revenue Less Distribution Costs (RLDC) was $1.083 billion, while Total Revenue and Reserve Revenue combined were $2.747 billion. The difference indicates that a large portion of gross monetization is paid out through the distribution layer.

This is crucial for modeling. Circle is not a pure beneficiary of rising interest rates or USDC balance growth—growth in reserve monetization does not translate one-to-one into retained profitability. According to Circle’s earlier sensitivity disclosure, using the average reserve yield of 4.26% as of June 30, 2025, as a baseline, a 100 basis point change would result in an estimated change in reserve revenue of approximately $618 million, but distribution and transaction costs would also change by approximately $315 million. This means a significant portion of the upside in reserve revenue is shared away, with only the remainder flowing into RLDC before deducting operating expenses. For institutional analysis, RLDC is a more useful intermediate profitability measure than simple reserve revenue.

FY2025 reported earnings quality was also significantly impacted by non-core and non-cash items. Circle disclosed a FY2025 net loss from continuing operations of $70 million, but Adjusted EBITDA was $582 million. The gap is primarily due to high equity incentives tied to IPO-related vesting conditions—Circle explained upon the FY2025 earnings release that results were significantly impacted by $424 million in IPO-vesting equity incentives, specifically $423.8 million in stock-based compensation expense recorded upon the satisfaction of RSU performance conditions when NYSE trading commenced. Therefore, GAAP net income is not the best lens for assessing underlying unit economics or profitability.

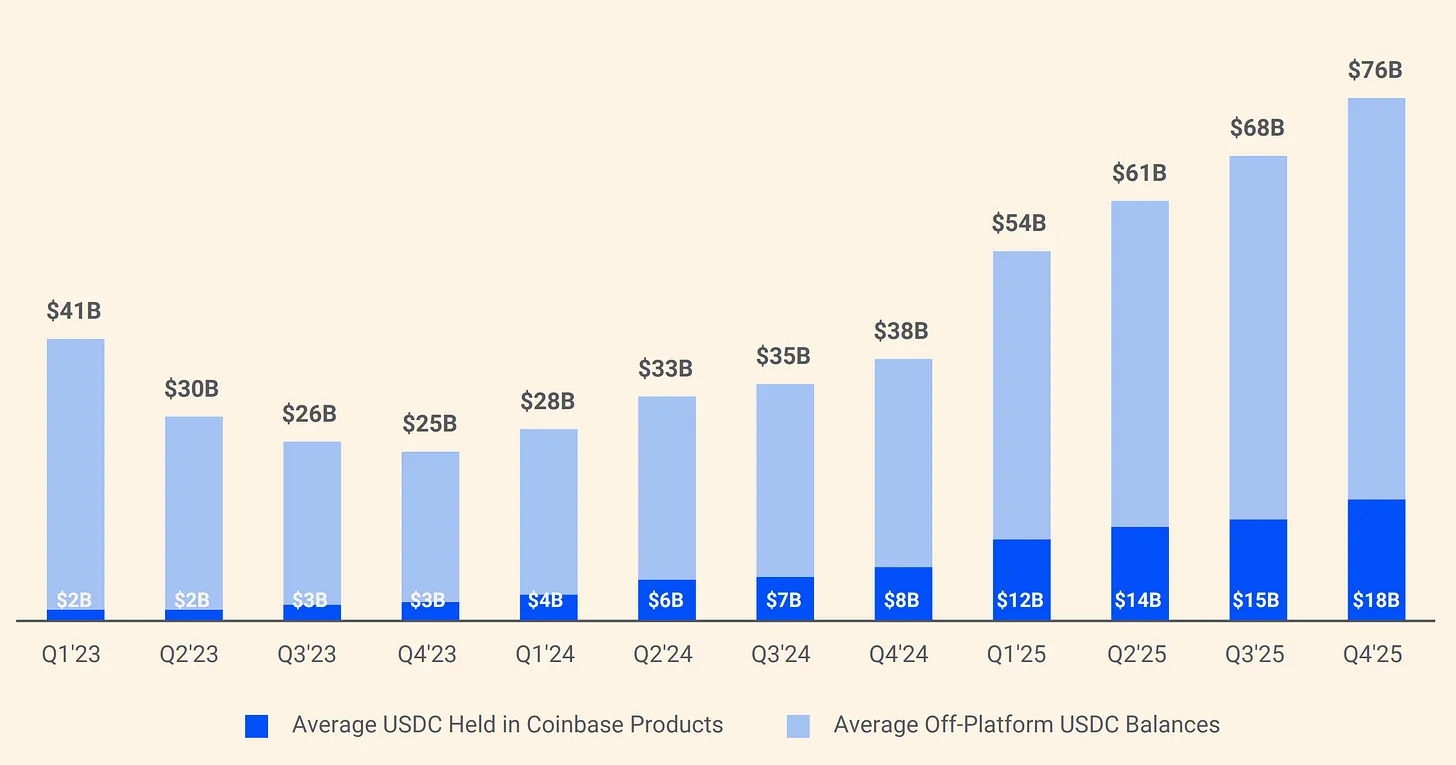

The most important reason is Circle’s arrangement with Coinbase, which is the most significant and often underestimated aspect of its business model.

When USDC launched in 2018, Circle and Coinbase jointly formed a consortium to govern the stablecoin. This structure was dissolved in 2023, with Circle taking sole control of issuance. However, Coinbase retained an extremely favorable revenue-sharing agreement.

Figure: Circle and Coinbase’s USDC Reserve Revenue Sharing Structure

According to the agreement, 100% of reserve revenue generated from USDC held on the Coinbase platform goes to Coinbase; for reserve revenue generated through other channels, 50% goes to Coinbase. In 2024, of Circle’s total distribution costs of $1.010 billion, $908 million was paid to Coinbase. In other words, for every dollar Circle earns, approximately $0.54 flows to a company that neither issues USDC nor manages its reserves. By early 2025, Coinbase held 22% of total USDC supply, up from just 5% in 2022. As USDC becomes increasingly concentrated on Coinbase, Circle’s payment burden rises accordingly.

In summary, at the current stage, Circle should be viewed as a stablecoin-centric, reserve revenue engine-driven, interest rate-sensitive financial infrastructure company, not a software platform whose economic structure is primarily driven by subscription or transaction revenue. The platform’s optionality value is becoming increasingly clear, especially with the expansion of Arc, CPN, and non-reserve revenue streams. However, Circle’s disclosed FY2025 revenue structure still supports an analytical framework centered on reserve balances, reserve yields, and distribution sharing mechanisms. Until the proportion of non-reserve revenue significantly increases, the reserve revenue model will remain the primary driver of Circle’s earnings sensitivity and the core of its valuation debate.

Deep Dive into USDC and EURC

USDC

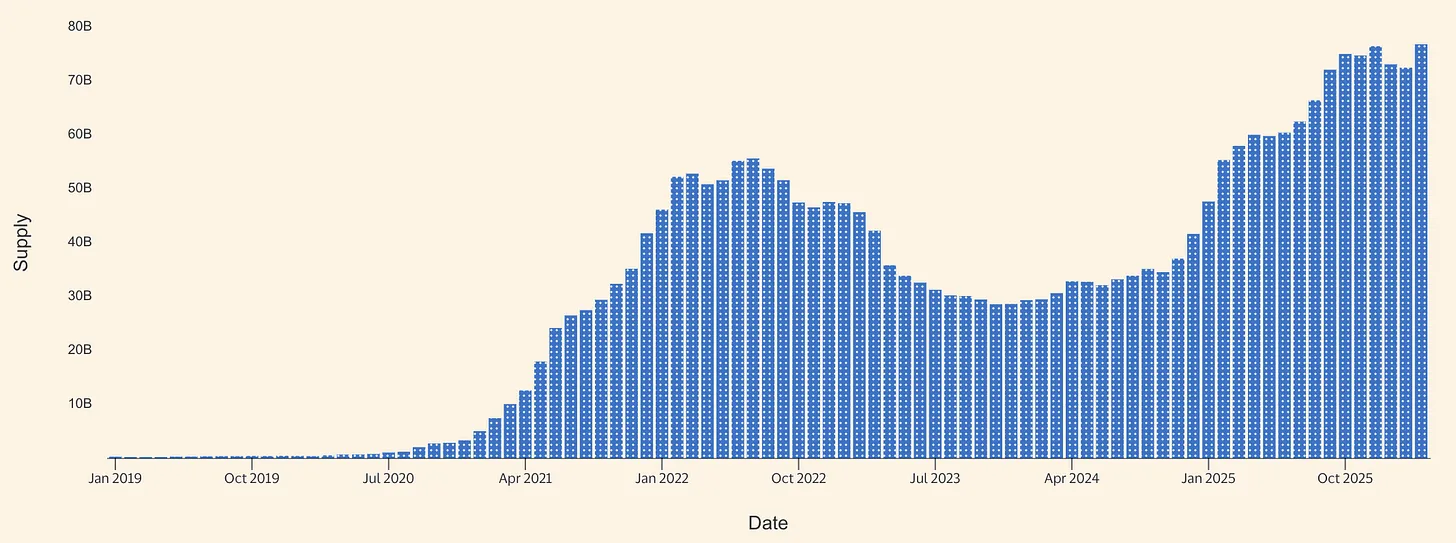

USDC is Circle’s core economic engine entering 2026. Circle disclosed in its FY2025 annual report that as of December 31, 2025, USDC circulation was $75.266 billion. Circle’s USDC product page subsequently showed circulation of $79.2 billion as of March 16, 2026. Based on this calculation, from year-end to mid-March, USDC circulation increased by approximately $3.9 billion, a growth of about 5.2%. This is not explosive growth but does indicate that net expansion continues on top of a strong foundation already established in 2025.

Figure: USDC Stablecoin Supply (Source: Allium)

Circle’s FY2025 disclosures point to a strong growth year for USDC. In Q4 2025, USDC circulation grew 72% year-over-year to $75.3 billion, and USDC on-chain transaction volume grew 247% year-over-year to $11.9 trillion. The full-year average USDC circulation was $64.870 billion, higher than FY2024’s $33.342 billion, but the FY2025 reserve return rate was 4.1%, lower than FY2024’s 5.0%. The core inference is: 2025’s revenue expansion relied on balance growth, not a yield tailwind, as the reserve return rate declined year-over-year.

Circle also disclosed some operational metrics indicating that USDC is a high-velocity monetary instrument, not static collateral. FY2025 USDC minting volume was $257.5 billion, and redemption volume was $226.1 billion; year-end stablecoin market share was 28% (based on third-party market cap data); year-end active wallets numbered 6.8 million (per Circle’s own definition). The large minting/redemption volume relative to the ending stock suggests significant transaction turnover, likely from exchange settlements, liquidity routing, collateral management, and DeFi-related capital flows, not a simple buy-and-hold reserve asset logic. Circle does not publicly provide clear breakdown data for these use cases.

The payment narrative for USDC is becoming more credible but remains in its early stages relative to the reserve revenue model. Visa has formally launched USDC settlement functionality in the US for specific issuing and acquiring partners, supporting the settlement of certain VisaNet obligations on specific blockchains, even outside traditional banking hours. Circle views this as proof that USDC can function as a continuous settlement asset, not just a 암호화폐-native trading tool. Even though the current scale is still small relative to Visa’s overall network volume, the analytical significance should not be underestimated: this is one of the clearest public signals that USDC is being positioned as part of real-world back-end payment infrastructure.

Partner distribution for consumer and SME ecosystems is also expanding. On December 18, 2025, Circle announced a partnership with Intuit to integrate USDC functionality into TurboTax, QuickBooks, and Credit Karma. Strategically, this strengthens the argument that Circle is pushing USDC out of trading venues and crypto-native users into mainstream financial workflows. However, the monetization path remains opaque—Circle has not disclosed pricing, commission rates, or revenue-sharing structures for this integration, so progress at the distribution level should not be misinterpreted as proof of high-margin payment revenue.

At the market structure level, Circle and Polymarket announced on February 5, 2026, that Polymarket would migrate from bridged USDC (USDC.e) on Polygon to native USDC over the coming months. This development indicates that Circle is more broadly pushing to reduce reliance on bridged liquidity and increase the coverage of natively issued USDC across chains. Native issuance can enhance redemption transparency, reduce operational complexity from cross-chain bridging, and better align with a regulatory-first positioning. Simultaneously, the need for such migration itself reveals a structural challenge for stablecoins: fragmented cross-bridge, cross-chain liquidity remains an adoption friction, not just a technical footnote.

In summary, USDC is a hybrid instrument: first, a primary exchange and venue settlement asset; second, high-velocity on-chain dollars for collateral, liquidity routing, and crypto market infrastructure; third, an emerging institutional settlement rail in specific integrations. Evidence for payment rail growth is improving, especially with Visa settlement, Intuit integration, and Circle’s broader infrastructure build-out. However, Circle’s disclosed primary economic driver remains reserve revenue on USDC reserves, not explicit transaction fee monetization from payment activities.

EURC

EURC is strategically important, though still limited in direct economic contribution. The European regulatory context is particularly relevant here. MiCA (EU Regulation 2023/1114) came into effect in 2023, with rules for asset-referenced tokens and e-money tokens applicable from June 30, 2024, and the broader regime fully effective from December 30, 2024. The significance of this timeline is: euro-denominated stablecoins gain a “regulatory compliant and rateable” status earlier than many adjacent crypto asset services, boosting institutional confidence for regulated issuers and exchanges to support compliant euro stablecoin products.

Circle disclosed that as of December 31, 2025, EURC circulation was 309,608,590 tokens. By March 16, 2026, Circle’s EURC page showed circulation of €382.8 million. Based on this calculation, from year-end to mid-March, EURC grew by approximately €73 million, an increase of about 23.6%. The absolute amount is still small relative to USDC, but the growth rate is meaningful, indicating EURC is gaining traction from a lower base.

The overall euro stablecoin market remains small. In September 2025, Reuters cited Italian central bank data reporting total euro-denominated stablecoin volume at only about $620 million, while global stablecoin issuance was around $300 billion at the time. Even with subsequent growth, Circle’s reported €382.8 million EURC circulation in March 2026 suggests EURC is likely one of the top euro stablecoins by supply.

Circle positions EURC as MiCA-compliant, supporting Avalanche, Base, Ethereum, Solana, and Stellar, with a commitment to monthly attestation reports. Strategically, EURC

이 글은 인터넷에서 퍼왔습니다: Earning $2.7 Billion in Revenue Yet Net Loss: Is Circle Essentially ‘Working for’ Coinbase?

Related: A Century-Old S&P, First Time On-Chain: Who’s Taking CME’s Weekend Business?

The key difference is that this time, S&P proactively sought out and licensed its brand to a decentralized protocol. The contracts use USDC as margin, are targeted at non-U.S. investors, trade 24/7, and have no expiration date. According to the S&P Global press release, over $1 trillion in S&P 500-linked exposure is traded daily in traditional markets. Now, a small portion of that access point has moved on-chain. But the significance of this event isn’t about compliance. It’s about traditional finance actively seeking out on-chain infrastructure to reach users and timeframes it previously couldn’t. The reason S&P chose Hyperliquid is hidden in the data from the past six months. HIP-3 is a permissionless perpetual contract deployment protocol launched by Hyperliquid in 2025, allowing anyone to create new trading markets on…