著者:東(ゆーすけ)

Who understands the current state of the 暗号 primary market best? Naturally, it’s the VCs still actively operating in the market.

Over the past few days, several investors from Pantera Capital, Crucible Capital, Blockworks, and Varys Capital engaged in a small-scale discussion on X about the current state of the primary market. While their views on the market situation differed to some extent, their debate may help us gain a clearer understanding of the primary market landscape.

Counterintuitive Reality: VCs Have Plenty of Capital, but Few Worthwhile Investment Opportunities

On the evening of April 20, Meltem Demirors, Partner and GP at Crucible Capital, published a short post on X explaining why the number of financing rounds in the 暗号 industry has significantly decreased.

Demirors believes that, overall, the “supply side” of early-stage founders and projects in the crypto industry is not as large as in other high-growth sectors. Over the past four years, this gap has become increasingly apparent, which is why her VC firm has started shifting its focus beyond the crypto market.

The venture capital business in the crypto market has been developing for 10 years, but the truly validated directions capable of generating “VC-level returns” are limited to just a few — stablecoins/payments, exchanges, and financial products. For VC investors and frontline founders, there are fewer breakout hits in this industry now, the cycles are longer, and the demands for industry knowledge, resilience, and long-term vision are higher. Consequently, the bar from seed round to Series A has also risen.

Although there are still some “generational” founders in the industry building category-デフィning companies (the VC’s job is to find them and win the opportunity to invest), the reality is that there is a clear gap between “the stories founders are telling” and “what VCs can reasonably invest in.”

After Demirors’ post, many fellow VCs joined the discussion.

Several investors commented below, agreeing with Demirors’ views. Among them, Blockworks co-founder Mippo summarized, concurring with Demirors that the primary market’s current issue is a shortage of outstanding founders and projects. On the VC side, there is actually ample capital available for investment — but at the same time, early-stage VC funds are in surplus, while VC funds focused on later-stage growth are noticeably insufficient.

Partial Disagreement: Where Is the Capital Actually Concentrated?

Regarding whether VC capital is concentrated in the early discovery phase or the later growth phase, Mason Nystrom of Pantera Capital and Tom Dunleavy, Head of Venture at Varys Capital, hold completely opposing views, leading to a heated debate between them.

Dunleavy was the first to speak, disagreeing with Mippo’s view that “early-stage funds are abundant, but later-stage funds are insufficient”: “I hold the exact opposite view. There is actually a huge amount of mid-to-late-stage crypto VC capital right now — mostly from recent and currently fundraising funds like Paradigm, Multicoin, Pantera, Dragonfly, etc. This doesn’t even include traditional VCs that partially dabble in crypto. In contrast, seed-stage and earlier rounds are underfunded… As long as you haven’t completely pivoted to AI, there are plenty of interesting projects to invest in.”

However, Nystrom, an insider at Pantera Capital (one of the later-stage VCs Dunleavy listed), strongly refuted Dunleavy’s claim. He argued that VC capital in the industry is now more concentrated in the early stage, rather than in Series A, Series B, or later rounds.

Nystrom did the math: If a fund wants to focus on Series A or Series B financing, they need to invest in at least 20-25 projects, each requiring a significant amount of capital — roughly $15 million for a Series A and $40 million for a Series B. By this calculation, a fund focused on Series A would need at least $300 million in assets under management (AUM), while a Series B-focused fund would need at least $800 million. This doesn’t even account for reserves, which typically require keeping 10% to 50% of cash on hand. How many funds in the industry meet these criteria?

So the reality is that there may be at least 50 funds with AUM under $100 million in the industry, but only about 15 funds with AUM exceeding $400 million. There are very few major players in the industry capable of participating in Series B and later rounds. There might be more Series B and later-stage capital in areas like fintech (e.g., stablecoins), but these projects have largely “graduated” into the traditional VC system and can no longer be simply considered crypto market projects.

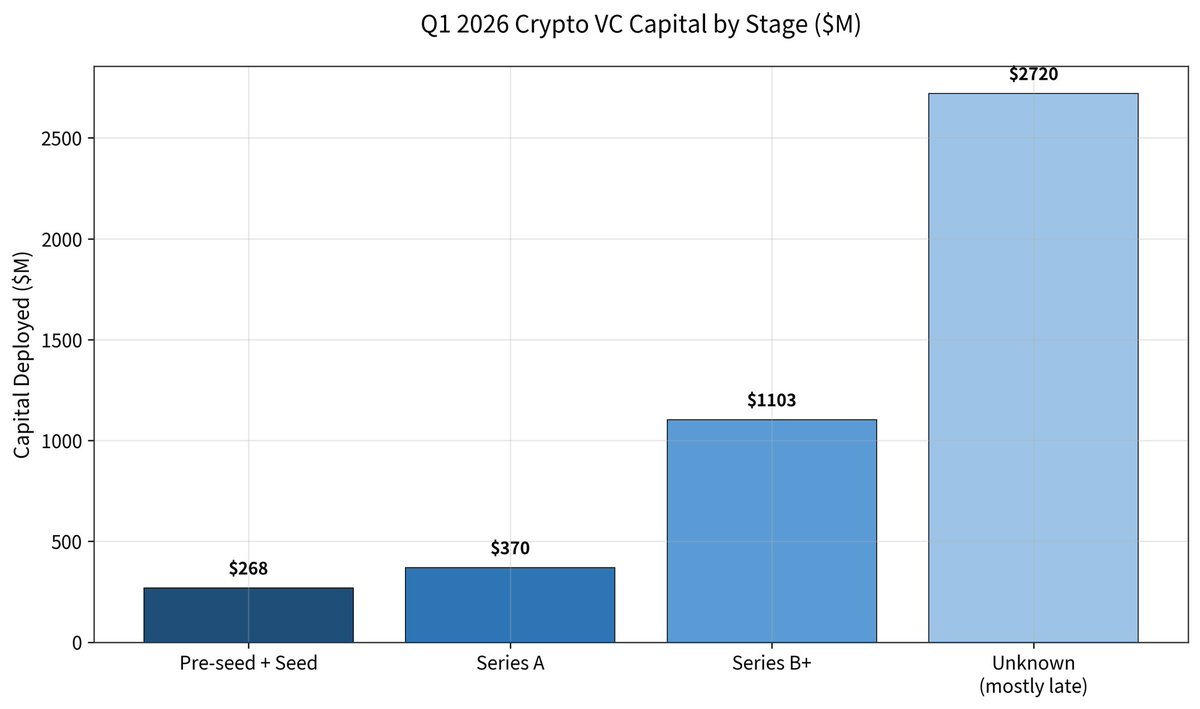

But Dunleavy was not convinced. In his response, he cited Galaxy’s Q1 primary market financing report, noting that in Q1 of this year, the total number of financing rounds across the industry dropped by 49% year-over-year, while the average round size increased by 76% (approximately $36 million). The total financing for seed and pre-seed rounds was only $268 million; Series A rounds totaled $370 million; Series B rounds reached $1.1 billion; and later-stage rounds hit $2.72 billion (mainly from Kalshi and Polymarket).

Dunleavy argued in rebuttal that the data shows in 2025, over 50% of the industry’s investment capital flowed into later stages (an all-time high), and in 2026, it has already exceeded 80%.

Dunleavy concluded by estimating the current capital situation in the primary market: Available capital for Series A and later stages is approximately $6 billion to $7 billion, concentrated in the hands of 5 to 6 large institutions. Available capital for seed and earlier stages is approximately $1 billion to $2 billion, dispersed across dozens of smaller, more fragmented funds.

Nystrom responded again, arguing that in the data Dunleavy cited, the vast majority of later-stage investments came from fintech-related projects that have already “graduated,” but these projects have long entered the traditional VC radar and secured funding, and should no longer be counted within the crypto industry.

Nystrom then continued his rebuttal based on Dunleavy’s conclusion that “only 5-6 funds can invest in Series A and beyond, but dozens of funds can invest in seed rounds”: “This means if you can’t convince one of those six funds, you’re basically out of luck. But in the early stage, if just one out of dozens of funds is willing to invest, you can survive. The ‘accessibility’ between these two is completely asymmetrical.”

Furthermore, funds like Pantera Capital, which have the capacity to invest in mid-to-late stages, also invest in seed rounds, but the reverse is not true. Combined with the fact that more and more VCs are transitioning to liquid funds, the actual scale of capital truly available for mid-to-late-stage investments in the industry is much smaller than the numbers suggest.

Beyond “Is There Capital,” the Real Question Is “Where Is the Capital, and Can You Access It”

In the end, neither side convinced the other. However, based on the direct debate between two frontline investors, we have gained a deeper glimpse into the reality of the crypto primary market — “whether there is capital” doesn’t seem to be the core issue; “where the capital is and whether you can access it” is the real crux.

On the surface, industry capital remains abundant, even highly concentrated in later-stage rounds. But from a practical standpoint, both VCs and entrepreneurs are facing a market that is becoming “structurally tighter” — early-stage capital appears dispersed but is fiercely competitive, while mid-to-late-stage capital seems plentiful but has extremely high barriers to entry. This also means the rules of the primary market game are changing. The era of completing a financing cycle based on narratives, traffic, and short-term execution is rapidly fading away. It is being replaced by a fundraising environment that relies more heavily on genuine business progress, long-term capabilities, and deterministic growth paths.

For VCs, this is a cycle of “fewer moves, heavier judgment.” For entrepreneurs, it is a survival test that requires crossing longer cycles and higher barriers.

この記事はインターネットから得たものです。 How much capital do VCs sticking to the primary market still have on hand?

Introduction Pump.fun launched in early 2024 as a permissionless Meme Launchpad on Solana, allowing anyone to create and trade tokens within seconds via a Bonding Curve mechanism. Starting as a niche experiment, it quickly became one of the highest-revenue applications on any public blockchain. From 2024 to 2025, Pump.fun’s daily protocol revenue consistently matched or even surpassed that of Hyperliquid, a fact made more notable by the inherently cyclical nature of the Meme market it operates in. Its native token, $PUMP, was issued at $0.004 through a $600 million ICO, with an FDV of $4 billion. Over the past few months, revenue has hit record highs and the token’s value has doubled, yet the current price of $PUMP is around $0.0019, down approximately 80% from its all-time high of $0.086…