Wall Street’s “Trojan Horse”: Analyzing the Power Restructuring and Infrastructure Convergence Behind ICE’s Stake in OKX

In the spring of 2026, Intercontinental Menukarkan Group (ICE) completed a strategic investment in the kriptocurrency trading platform OKX at a valuation of $25 billion. As the parent company of the New York Stock Menukarkan (NYSE), this deal by ICE moves beyond the previous tentative model where Wall Street merely established “capital channels” through spot ETFs. Analyzing the disclosed cooperation framework between the two parties—from spot price data licensing and establishing joint venture entities to the joint distribution of tokenized stocks—the focus of the collaboration directly targets the underlying operational hubs of financial markets.

The licensing of spot data aims to establish a regulated pricing anchor for traditional institutional capital entry; while the advancement of joint ventures and tokenized stocks essentially attempts to bridge the physical boundary between the traditional fiat currency system and native kripto liquidity pools. This systematic strategic bundling indicates that traditional mainstream capital’s strategy towards the crypto ecosystem has officially transitioned from peripheral “asset allocation” to an “assimilation” phase relying on capital intervention in underlying infrastructure.

This is not merely a simple financial settlement; it is a top-down power reshaping of the emerging crypto market by the old financial system, leveraging capital leverage and compliance frameworks.

Power Restructuring: The Transfer of Pricing Power and the Mutual Assimilation of Infrastructure

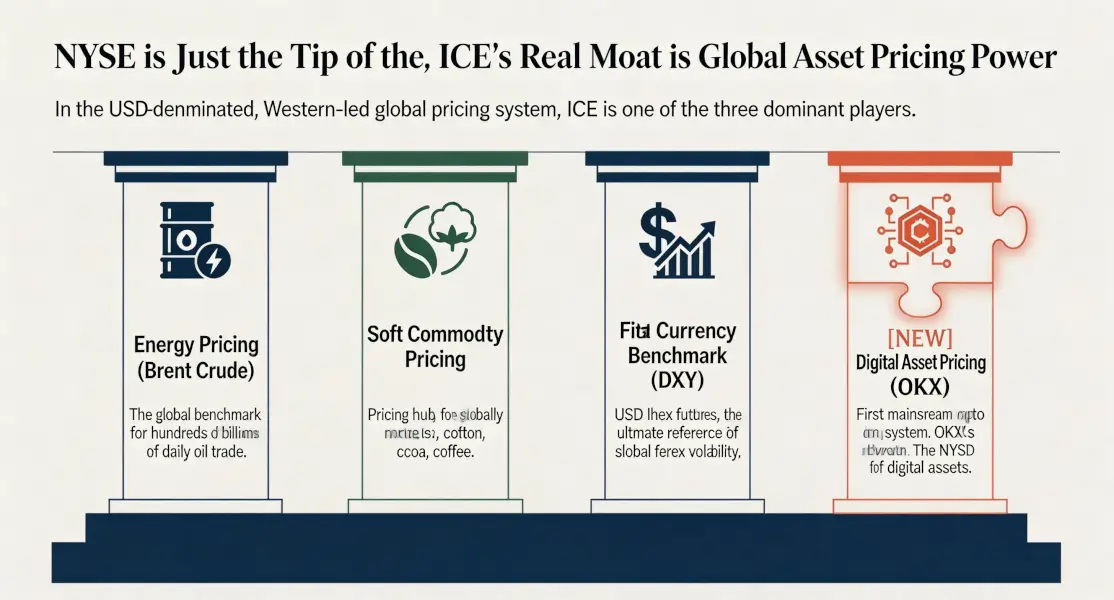

The core anchor of this deal lies in the foundational pillars of the financial system: pricing power and clearing infrastructure.

As an oligopoly in traditional markets, ICE monopolizes pricing benchmarks for core macro assets ranging from stock data of the New York Stock Exchange (NYSE) to Brent crude oil and the US Dollar Index. This pricing power, based on legal trading hours and centralized clearing, forms the core of its business model. However, facing a crypto asset network with a total market capitalization in the trillions of dollars, operating 24/7 with highly fragmented liquidity, ICE’s original traditional price discovery mechanism exhibits a clear structural disconnect.

Obtaining OKX’s spot data license is a substantive move by ICE to fill this disconnect. Currently, the Chicago Mercantile Exchange (CME) has already gained some pricing advantage in the institutional market through regulated Bitcoin futures. By deeply binding capital with a leading spot platform, ICE can directly penetrate offshore markets to obtain first-hand underlying trading and depth data. This allows it to bypass a lengthy cold start and directly build its own crypto derivatives product line compliant with US regulatory standards, attempting to reclaim the ultimate interpretative authority over crypto liquidity back into Wall Street’s traditional infrastructure system.

For OKX, transferring core spot pricing data is the price paid to break through its current business bottlenecks. Currently, the stock competition among pure crypto asset trading platforms is intensifying, with single-user acquisition costs peaking. The fee model relying solely on spot and perpetual contracts has hit a growth ceiling. By accessing ICE’s underlying compliance architecture, OKX has essentially completed a business model transformation: from a single crypto asset matching engine to a two-way distribution network connecting 120 million native crypto liquidity users with Wall Street’s compliant financial products.

Path Evolution

Looking back at ICE’s expansion history in the crypto space, its business path has undergone a strategic correction based on real market feedback.

In 2018, ICE launched Bakkt, a Bitcoin futures platform focused on physical delivery. Its early strategic logic was typical “compliance infrastructure first”: attempting to siphon and regulate crypto market trading volume by establishing clearing and delivery channels meeting the highest regulatory standards for traditional institutions. However, Bakkt’s subsequent prolonged business stagnation validated a structural rule: in the crypto market, compliance frameworks cannot create liquidity out of thin air. Traditional trading systems detached from native retail networks and crypto market maker ecosystems easily become “compliance islands” lacking real trading depth.

Bakkt’s setback during the cold start prompted ICE’s management to reassess its business logic. They realized that in a two-sided trading market with strong network effects, the cost of rebuilding the trading habits of tens of millions of crypto users and reshaping underlying liquidity far exceeds building a set of institution-grade clearing code. Rather than spending cycles on internal incubation, it’s better to directly turn to external capital capture.

Since then, ICE’s resource allocation has shown clear node-embedding characteristics. In 2025, ICE invested in the decentralized prediction market Polymarket. The commercial essence was to preemptively secure an entry point for on-chain event-driven data sources and pricing for non-standard assets. This heavy investment in OKX now directly cuts the radius of asset capture into the core of the crypto world—the two-way liquidity network for spot and derivatives.

From promoting Bakkt’s “self-built closed loop” to now achieving “capital embedding” through stakes in Polymarket and OKX, ICE’s evolution represents a common consensus among current Wall Street giants: abandon the heavy-asset model of reshaping crypto rules from scratch, and instead use capital leverage as a “Trojan horse” to directly connect crypto-native infrastructure with proven scale effects into their own vast global clearing and distribution networks.

The “Second Half” of Tokenized Assets

The large-scale on-chain migration of RWA (Real World Assets) constitutes the direct commercial motivation for this infrastructure convergence.

Entering the second half of 2025, with the US regulatory side initially clarifying the classification and ownership framework for Tokenized Securities, the scale of on-chain mapping of underlying stock assets saw a structural leap. Facing this incremental space sufficient to reshape the underlying settlement protocols of traditional securities markets, core Wall Street institutions are accelerating their competition for the issuance and circulation hubs of tokenized assets.

In the infrastructure evolution of asset tokenization, the market has diverged into two distinct evolutionary paths. Nasdaq tends towards reformism, relying on traditional clearing centers like DTCC (Depository Trust & Clearing Corporation) to complete the registration and circulation of tokenized assets within the existing compliance system. In contrast, ICE’s strategic layout shows clear vertical integration characteristics, attempting to reconstruct a full-chain closed loop from asset encapsulation to end-user distribution:

On the supply side, the NYSE is advancing a tokenized securities engine supporting Delivery vs. Payment (DVP) and 24/7 circulation; on the clearing side, ICE attempts to eliminate cross-chain settlement friction between fiat and digital assets by establishing a Tokenized Deposits mechanism; and on the distribution side, OKX’s accumulated user base of hundreds of millions of native crypto accounts completes its liquidity outlet to the global retail end.

This hybrid infrastructure architecture of “underlying licensed assets + on-chain native distribution” poses a substantive substitution threat to the traditional T+1 settlement cycle in terms of transaction efficiency. Looking at the medium to long-term industry evolution, the core barrier in the RWA track is shifting from a singular “asset on-chain capability” to the “integration capability of compliant channels and global liquidity.” After this systematic integration, both small and medium-sized crypto platforms lacking high-quality fiat asset channels and unilateral financial institutions constrained by traditional distribution channels will face the risk of liquidity being siphoned away. Composite infrastructure possessing cross-domain asset clearing and global network reach capabilities will hold substantive dominance in asset pricing in the next cycle.

Deep-Seated Friction

Returning from strategic speculation to the execution level, this infrastructure integration faces significant structural friction. Capital-level binding does not directly eliminate the underlying misalignment between the traditional fiat system and the crypto-native ecosystem in terms of regulatory paths, clearing mechanisms, and governance structures.

First is the end of regulatory arbitrage and the compliance costs of multi-jurisdictional oversight. After experiencing early-stage rough expansion in offshore markets, OKX attempts to complete its compliance reshaping for the US market by introducing ICE’s traditional licensing system. However, US regulation of crypto and tokenized assets has long been fragmented between the SEC (focusing on securities attributes) and the CFTC (focusing on commodity attributes). The cross-border classification of tokenized stocks, the penetrating scrutiny of offshore liquidity, and the lengthy compliance processes that joint venture entities must undertake under a multilateral regulatory system will substantially increase operational expenses. Whether ICE’s lobbying leverage on Capitol Hill can translate into substantive licensing benefits for OKX in the yet-to-be-defined crypto legislative game remains highly uncertain.

Second is the liquidity mismatch risk induced by asynchronous clearing mechanisms. Although the cooperation framework involves joint R&D of tokenized deposits, at this stage, the fiat settlement cycles of traditional banks, limited to weekdays and legal trading hours, inevitably create a physical time lag with the 24/7 high-frequency matching of crypto networks. During extreme volatility events such as macro data releases or on-chain black swans, the closure or delay of fiat channels can easily trigger liquidity dislocations on the crypto side. How to build market-making and buffering mechanisms between non-synchronous clearing networks that can withstand margin breaches during extreme market conditions constitutes the core technical resistance to underlying system integration.

Finally, there is the substantive mutual exclusivity of governance structures and risk appetites. The governance bottom line of traditional regulated financial institutions is extreme risk aversion and absolute process compliance; whereas the business driving force of crypto-native platforms is essentially built on agile iteration and embracing high-volatility exposure. When traditional capital’s compliance committees substantively intervene in the product launch flow and asset listing rights of crypto platforms, it will inevitably lengthen the decision-making chain. This game between risk tolerance and business expansion efficiency will cause long-term governance friction at the board level of the joint venture company, potentially weakening the platform’s competitive edge in purely crypto-native arenas.

Full-Asset Circulation in a “Frenemy” Landscape

Looking horizontally at the current macro-financial cycle, the cooperation between ICE and OKX constitutes a landmark node in the “convergence of TradFi and Crypto infrastructure.”

This systematic convergence is accelerating replication across the industry: from BlackRock establishing Coinbase as the core custody and prime brokerage node for its spot ETFs, to traditional market-making giant Citadel Securities penetrating the order flow of platforms like Kraken, to JPMorgan Chase advancing institutional intraday repo clearing based on its Onyx blockchain—the physical separation between fiat capital networks and decentralized protocols is being systematically broken.

In this process, the market is evolving an “asymmetric symbiosis” pattern based on factor exchange. Traditional Wall Street oligopolies no longer seek to build crypto trading engines from scratch; instead, they precisely capture the high-frequency, globalized, and traditionally compliance-frictionless retail trading flow of the crypto market through capital injection and channel authorization. Meanwhile, native crypto infrastructure exchanges partial equity and underlying data sovereignty for the balance sheet support of traditional finance, fiat clearing whitelists, and institutional moats to withstand extreme compliance risks. This asset restructuring based on comparative advantage is substantively stripping away the early “anti-establishment” label of the crypto ecosystem, weaving it thoroughly into the operational orbit of global financial capital.

Projecting along this path of infrastructure fusion, the asset forms and circulation boundaries of global capital markets are tending to dissolve. The endgame for next-generation financial infrastructure points towards a global asset clearing network with “unified ledger” attributes. Under this architecture, the issuance vehicles for heterogeneous assets—whether native proof-of-work Bitcoin, tokenized US stocks encapsulated by smart contracts, or RWA assets mapping real-world income rights—will detach from traditional settlement silos. They will achieve 24/7 instant settlement and cross-asset cross-margin circulation based on atomic settlement within a shared global liquidity pool. This is not only a structural release of clearing efficiency but also a complete reshaping of the global liquidity pricing paradigm.

Kesimpulan

Marked by ICE’s stake in OKX, the capacity consolidation in the crypto asset trading arena is nearing its end. Within the foreseeable macro cycle, with traditional regulatory frameworks like Basel substantially covering crypto asset exposures and persistently high compliance costs squeezing platform profit margins, global crypto liquidity will irreversibly concentrate towards a few oligopolistic nodes possessing “traditional licenses + native infrastructure.”

In this landscape evolution, tail-end trading platforms lacking quality fiat clearing channels, core regulatory licenses, and access to mainstream institutional order flow will face severe liquidity depletion. In the stock competition of two-sided markets, they may be passively cleared out due to inability to bear exponentially growing compliance expenses, or become discounted M&A assets for traditional capital to complete their full-chain infrastructure puzzle.

For leading native platforms that have completed capital binding, their business model has undergone a fundamental transfer: in exchange for accessing the trillions-of-dollars balance sheets and compliant distribution channels of traditional finance, platforms must fully internalize Wall Street’s stringent KYC/AML standards, anti-manipulation monitoring systems, and capital adequacy requirements. Pure “technological neutrality” no longer applies, replaced by a highly privileged and access-controlled financial intermediary model.

Penetrating the underlying logic of this infrastructure reconstruction, this is not a simple zero-sum game, but a cross-cycle balance sheet swap. Traditional financial oligopolies have used capital leverage to achieve low-cost capture of the next generation of distributed ledgers and 24/7 clearing networks; while the crypto-native industry, by substantively ceding its early “decentralization and censorship-resistance” fundamentalism, has exchanged for a perpetual license to access the main artery of global fiat currency liquidity.

About BlockBooster

BlockBooster is a next-generation alternative asset management firm for the digital age. We utilize blockchain technology to invest in, incubate, and manage the core assets of the digital era—from blockchain-native projects to Real World Assets (RWA). As value co-creators, we are committed to discovering and unleashing the long-term potential of assets, capturing exceptional value for our partners and investors in the wave of the digital economy.

Penafian

This article/blog is for informational purposes only and represents the author’s personal views, not the position of BlockBooster. This article is not intended to provide: (i) investment advice or recommendations; (ii) an offer or solicitation to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets, including stablecoins and NFT, involves extremely high risks, with significant price volatility, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions regarding specific situations, please consult your legal, tax, or investment advisor. The information provided in this article (including market data and statistics, if any) is for general reference only. Reasonable care has been taken in compiling this data and charts, but no responsibility is accepted for any factual errors or omissions expressed therein.

Artikel ini bersumber dari internet: Wall Street’s “Trojan Horse”: Analyzing the Power Restructuring and Infrastructure Convergence Behind ICE’s Stake in OKX

Related: Taking Web3 to “Daily Life”: Zakk Explains OKX Web3’s “Next Phase”

At the event, Zakk, Head of OKX Wallet, systematically shared the core methodology of OKX’s Web3 products and key directions for the coming years: rooted in security and self-custody, bridged by product experience, and driven by ecosystem and infrastructure, ultimately pushing crypto assets from being “professional tools” into “daily life.” Pursuing the “Ultimate” Web3 Experience In Zakk’s explanation, the “ultimate Web3 experience” is not a slogan but a set of verifiable, sustainably iterable product standards—firstly, security and self-custody; secondly, “leaving complexity to the system and simplicity to the user.” He emphasized the underlying principle of self-custody: Not your key, Not your asset, which serves as the long-term guiding principle for OKX Wallet’s design and trade-offs. More “down-to-earth” was his use of personal experience to explain why security capabilities must be…