Author: Zhao Ying

स्रोत: Wall Street CN

The Fed held rates steady, but Wall Street heard a louder hawkish cry. Three dissenting votes against maintaining an easing bias, the inflationary pressure from surging oil prices, and Chairman Powell’s term nearing its end have collectively shifted the market from pricing in rate cuts to a more complex assessment of rate hike risks.

According to trading desk reports, at the April 29 FOMC meeting, the Federal Reserve kept the federal funds rate target range unchanged at 3.50%-3.75%. Post-meeting analyses from Goldman Sachs, Bank of America, JPMorgan, and HSBC all converge on the same conclusion: what truly matters is not the rate decision itself, but the widening divergence in the statement’s language, indicating a loosening consensus on the policy direction within the committee.

Deteriorating conditions in Iran made oil prices the other key theme of the day. Bank of America noted that the 2-year Treasury yield rose by 10 basis points, with only about 3 basis points occurring after the Fed’s decision; the remaining 7 basis points were primarily driven by an 8% single-day surge in Brent crude oil to $120/barrel. JPMorgan also believes that the Iran situation and risks in the Strait of Hormuz pushed energy prices higher, directly compressing the Fed’s room for easing.

The leadership transition amplified policy uncertainty further. Powell confirmed this would be his last FOMC meeting as Chair, stating he would remain on the FOMC as a regular member after his term ends, with his departure date yet to be determined. Meanwhile, the Senate Banking Committee has advanced Kevin Warsh’s nomination for Fed Chair. An era of monetary policy has officially ended, and the new chair’s policy style and communication framework are becoming the new focal points for the market.

Three Dissenting Votes Undermine the Easing Bias

The most closely watched signal from this meeting was the division within the FOMC over the statement’s language.

Goldman Sachs economist David Mericle pointed out that three committee members – Hammack, Kashkari, and Logan – opposed the language implying an easing bias, a result that took Goldman Sachs by surprise. At the same time, Miran supported a rate cut, aligning with Goldman’s earlier assessment.

The controversy centered on the phrase “timing of additional adjustments.” In market context, this wording is seen as signaling the possibility of further rate cuts. The three members’ opposition to retaining this phrasing suggests some policymakers are no longer willing to continue signaling a one-way dovish stance to the market.

Powell acknowledged in his press conference that there was a “lively discussion” within the committee regarding policy guidance. He stated that the number of members favoring a shift to more neutral guidance had increased compared to March, and the FOMC’s central tendency is moving towards a “more neutral” interest rate outlook, though the majority believes the timing is not yet ripe. He even suggested that a wording adjustment “could come as early as the next meeting” – scheduled for June 16-17.

HSBC also emphasized that the essence of this divergence is that the policy direction is no longer singular. While the three members supported keeping rates unchanged, their explicit opposition to retaining the easing bias sends a clear message to the market: the next move could be either a cut or a hike.

“Rate Hikes” Return to Pricing, Bar for Cuts Raised

Wall Street’s consensus is that the Fed hasn’t officially pivoted to hiking, but the long-dormant word “hike” is back in the market’s vocabulary.

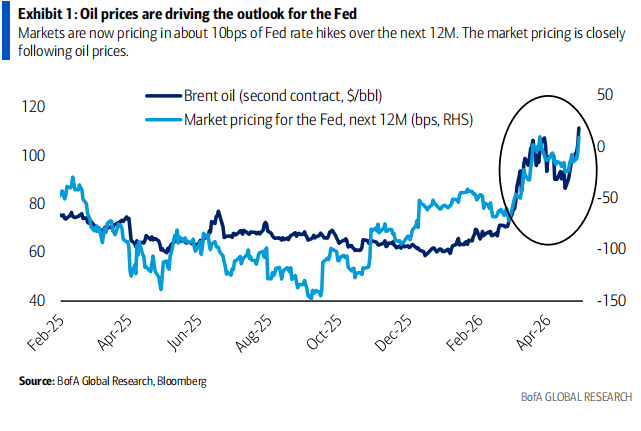

Bank of America stated that following a slightly hawkish FOMC meeting, compounded by record-high oil prices, the market is now pricing in approximately 10 basis points of rate hikes over the next 12 months. The bank also noted this differs from the 2022 hiking cycle, as the current energy shock also exerts downward pressure on growth, a point Powell highlighted in his press conference.

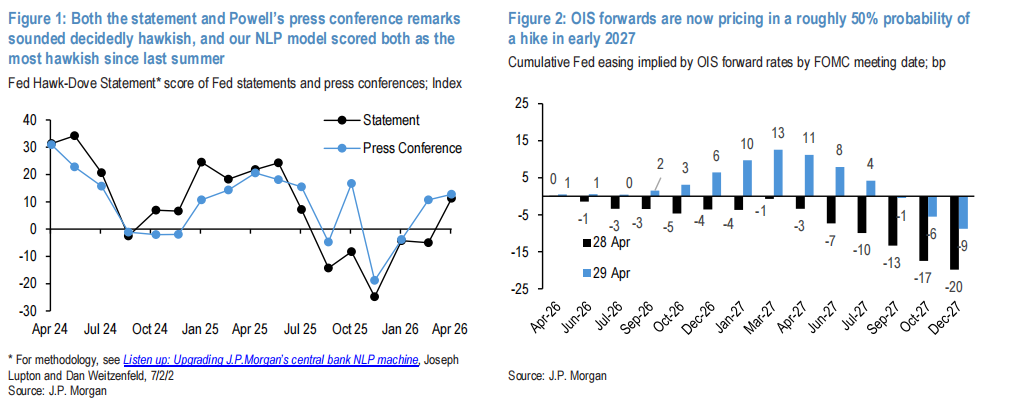

JPMorgan’s interpretation was more hawkish. Its natural language processing model showed that the hawkishness scores for both the statement and Powell’s press conference reached their highest levels since June 2025. The bank stated that money market pricing had swiftly shifted from “almost a full rate cut by end-2027” to “near a 50% probability of a hike by early 2027.”

Goldman Sachs maintained a more cautious view. The bank still forecasts rate cuts in September and December but believes the bar for cuts has been significantly raised in the absence of a clear weakening in the labor market. Goldman stated that the risk of an extended pause in rates is rising, but it remains highly skeptical of the possibility of a rate hike.

HSBC offered the strongest forecast. The bank expects the Fed to cut rates neither in 2026 nor in 2027. HSBC believes that unless core PCE inflation falls below 3% or even 2.5%, rate cuts are virtually impossible. Its own forecast shows core PCE inflation remaining above 3% until late 2026 and above 2.5% until late 2027.

Oil Takes Center Stage; Iran Situation Drives Pricing Logic

Unlike past meetings where the Fed’s statement dominated market reaction, energy prices were the core variable for interest rates on this day.

Bank of America noted that of the 10 basis point increase in the 2-year Treasury yield, only about 3 basis points were attributable to the Fed’s decision itself, with most of the remaining increase coming from Brent crude oil’s rise to $120/barrel. The bank argues that the primary driver of the Fed’s current outlook is the Iran situation and oil prices, rather than a simple policy reaction function.

JPMorgan also attributed the rise in front-end yields and the flattening of the yield curve to the worsening situation in the Middle East and risks in the Strait of Hormuz. Rising oil prices not only boost inflation expectations but also make it harder for the Fed to signal easing.

Powell explicitly stated in his press conference that amidst high uncertainty regarding geopolitical conflicts and energy prices, the majority of members saw no need to adjust policy guidance at this time. JPMorgan noted that Powell set preconditions for potential rate cuts, requiring stabilization in energy prices and progress on tariff issues.

Goldman Sachs believes that even if the geopolitical conflict eventually ends, some FOMC members might remain hesitant to cut rates if inflation is still closer to 3% than 2%. Even if the overshoot in inflation stems mainly from tariffs and energy price pass-through, policy easing may not arrive quickly.

Powell’s Farewell; Warsh Takes the Baton, Introducing New Variables

This meeting also marked the end of Chair Powell’s tenure.

Bank of America noted this was the last FOMC meeting chaired by Powell in his capacity as Chair. Goldman Sachs’s report also mentioned that Powell stated he would remain on the FOMC as a regular member after his term as Chair ends on May 15, with his departure date to be determined.

Regarding his decision to stay on, Goldman Sachs cited Powell saying he is waiting for relevant investigations to conclude with full transparency and finality, and will leave when he deems appropriate. JPMorgan and HSBC also mentioned that Powell intends to maintain a low profile and will not obstruct the FOMC’s functioning under Warsh’s leadership.

The progress of Warsh’s nomination has become a key focus for the market. JPMorgan noted that the Senate Banking Committee approved his nomination along party lines. HSBC pointed out that the full Senate vote has not yet occurred, but if things go smoothly, Warsh could be officially sworn in before the June meeting.

HSBC believes Warsh could bring about systematic changes to the policy communication framework. The bank’s rates strategists noted that Warsh has expressed skepticism about the Fed’s “dot plot” rate projection mechanism. If forward guidance is weakened in the future, bond market volatility could increase, and term premiums on long-end rates might face upward pressure.

Rate Volatility and Policy Uncertainty Coexist

For fixed-income investors, the message from this meeting was not monolithic. Short-end yields were pressured by oil prices and hawkish pricing, pushing expectations for rate cuts further out; however, a rate hike has not yet become a unified base case across investment banks.

Bank of America believes that for the investment-grade bond market, the current rise in yields partially offsets the impact of interest rate volatility. Since implied rate volatility remains below its peak in March this year, technicals for investment-grade bonds may be supported for the time being.

JPMorgan warned that the combination of pressure on short-end yields, relatively expensive mid-term Treasury valuations, and policy uncertainty stemming from the leadership change suggests the interest rate market is entering a more complex phase of competition.

HSBC maintains its “maximum bullish” stance on a multi-asset level, focusing primarily on US stocks. The bank stated that despite a hawkish reassessment of rate expectations, risk assets performed strongly in April, and optimistic sentiment surrounding the profitability of the AI supply chain remains an important narrative in the multi-asset market.

Overall, Wall Street’s conclusion on this FOMC meeting is: The Fed didn’t change rates, but it changed the market’s probability distribution for the next move. With Powell stepping aside, oil taking center stage, and Warsh set to take over, investors are no longer simply facing a timetable for rate cuts, but a new interest rate environment driven jointly by inflation, energy, employment, and policy communication.

यह लेख इंटरनेट से लिया गया है: Powell’s Final Act: Wall Street Hears a Louder Hawkish Tone

Original Compilation: Baihua Blockchain In this interview, Wilfred Frost conducted a second in-depth conversation with Dan Morehead, founder of Pantera Capital. They discussed Bitcoin’s positioning in the cycle after a 50% retracement from its highs; how fiat currency depreciation creates generational wealth conflict; and why the “smart money” is the last to enter this round. Key Insights Summary Most institutional investors still have a 0.0% allocation to blockchain, literally zero. It’s not that gold hit a new high; it’s that paper currency hit a historic low. This might be the first trade in history where the “smart money” is the last to enter. The average age of first-time homebuyers in the US has been pushed back from 28 to 40. We are facing a generational inflection point where money is…