6 months to decide victory? SemiAnalysis: Meta may replace Google to be crowned the “third pole” of AI

简要说明

- SemiAnalysis bets Meta may surpass Google in the next 6 months, becoming the strongest contender behind Open人工智能 and Anthropic.

- This judgment is based on three factors: the $14.3 billion Scale AI deal, RL data production, and multi-GW computing power expansion.

- Muse Spark 1.1 has yet to catch up with frontier models; whether Meta can overtake Google depends on the performance of the next generation of models.

This isn’t to say Meta has already caught up. Meta released Muse Spark in April, and according to Axios on July 9, Muse Spark 1.1 has opened its API to developers, priced at $1.25 per million input tokens and $4.25 per million output tokens. Axios notes this is not the “great leap forward” model Meta had hoped for; its larger model, codenamed Watermelon, remains in training.

SemiAnalysis is betting on something else: after the setback with Llama 4, Zuckerberg is restructuring the AI organization more aggressively, pouring money, talent, internal engineering resources, and data center capacity into the super intelligence lab. The core point of contention in the report is whether Google can still hold its position as the third pillar of AI.

Current Models Are Not Strong; The Report Bets on a 6-Month Catch-Up Speed

After the debut of Meta’s super intelligence lab with Muse Spark, it has not replicated the open-source leadership felt during the Llama 3 and Llama 3.1 era. According to SemiAnalysis’s tests and assessments, Muse Spark and its subsequent versions still fall short of the frontier in most benchmarks and general agent scenarios.

This is also where the report requires the most qualification. Details like Muse Spark 1.1 being roughly equivalent to Opus 4.6 or GLM 5.2, and internal token usage not yet being migrated, are based on the authors’ tests and model judgments, not Meta’s official statements. At least from publicly available information, Meta has yet to produce a model capable of directly challenging OpenAI and Anthropic.

However, SemiAnalysis is focused on the slope. After the failure of Llama 4, Meta’s super intelligence team underwent a large-scale reorganization, and the short-term organizational chaos is being absorbed. The report judges that if the next round of model training and reinforcement learning data production begins to reflect in the products, Meta’s position might be higher than what current leaderboards show.

The $14.3 Billion Scale AI Deal Acquires the Scarce Talent Needed for Frontier Models

Meta’s most prominent move is its $14.3 billion investment in Scale AI. Multiple media outlets, including Fortune, Forbes, and Reuters, have reported that through this deal, Meta brought in Scale AI founder Alexandr Wang, who will join or lead teams related to super intelligence.

In the frontier model competition, this deal is more than just purchasing a data labeling company; it resembles an intense talent acquisition. Scale’s safety, evaluation, and alignment team, SEAL, is seen by SemiAnalysis as a crucial source for Meta to bolster its evaluation, alignment, and post-training capabilities.

Reuters also reported that Meta offered some AI engineers compensation packages worth hundreds of millions of dollars. This figure indicates that Meta has elevated super intelligence to a company-level priority, rather than standard AI product iteration. For a large tech company, the real challenge isn’t allocating a budget, but aligning research, products, infrastructure, and management around a single goal.

SemiAnalysis quotes Alexandr Wang from a recent podcast, stating that true frontier labs often first believe super intelligence is near, and then all business decisions follow that judgment. The report interprets Meta’s recent actions as converging towards the AGI priority model of OpenAI and Anthropic.

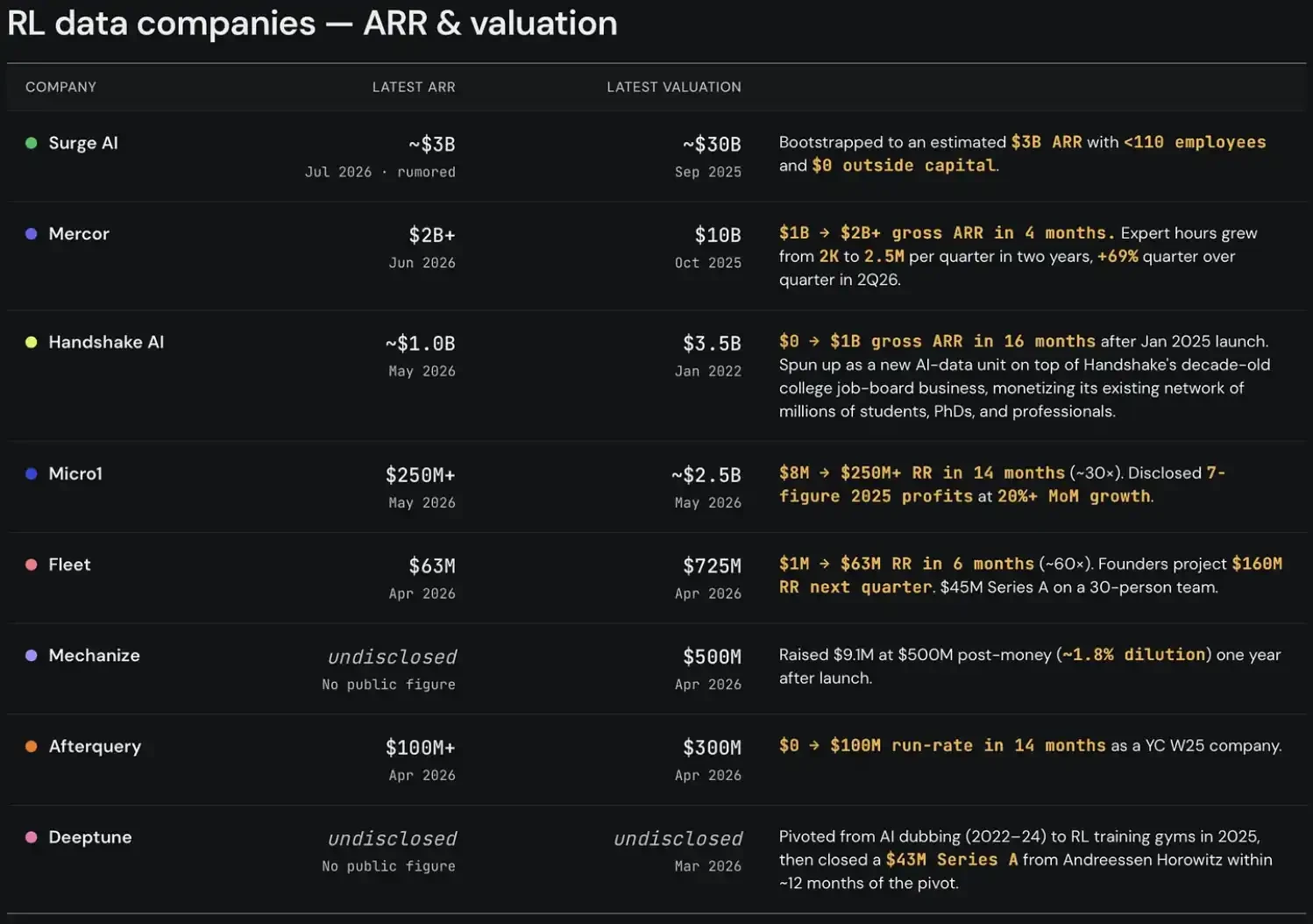

3,000 Engineers Shifted to RL, Meta Aims to Turn Internal Work into Training Data

Beyond talent, reinforcement learning tasks and real work data form the second line.

Today, model capability improvement no longer relies solely on pre-training data. More critically, it depends on whether models can complete tasks in environments close to real work: understanding context, calling tools, executing tests, fixing errors, and then iterating based on results. Tasks like codebase repair, product analysis, and internal tool calls are much closer to the true difficulty of white-collar work than standard exam questions.

SemiAnalysis states that Meta has reassigned approximately 3,000 engineers to become full-time RL task creators. This figure needs to be interpreted within the report’s context, but if executed well, Meta’s advantage becomes clear: it isn’t simply outsourcing the purchase of human data; it is turning its own engineering organization into a training task production line.

This type of data is particularly important for agents. Many RL tasks appear difficult, but the actual prompts often detail steps too meticulously, inconsistent with real work habits. Screen recordings, daily workflows, tool-call logs, and internal evaluation systems may be better suited for training models capable of automating white-collar work.

This is also one reason the report favors Meta catching up to Google. Google has DeepMind, Gemini, TPUs, and its cloud business, but Meta is concentrating its internal organization, data, and engineering capabilities towards a single model objective.

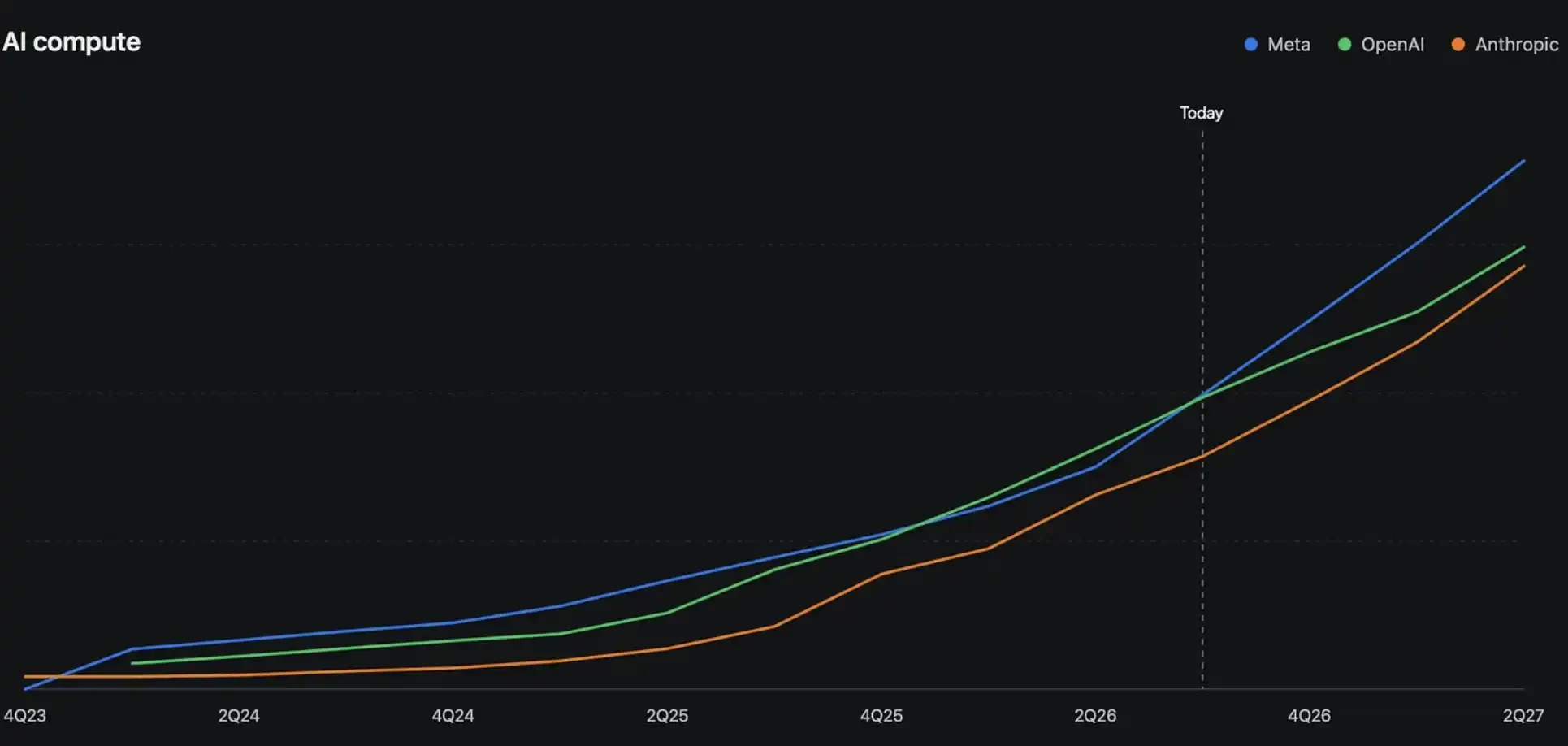

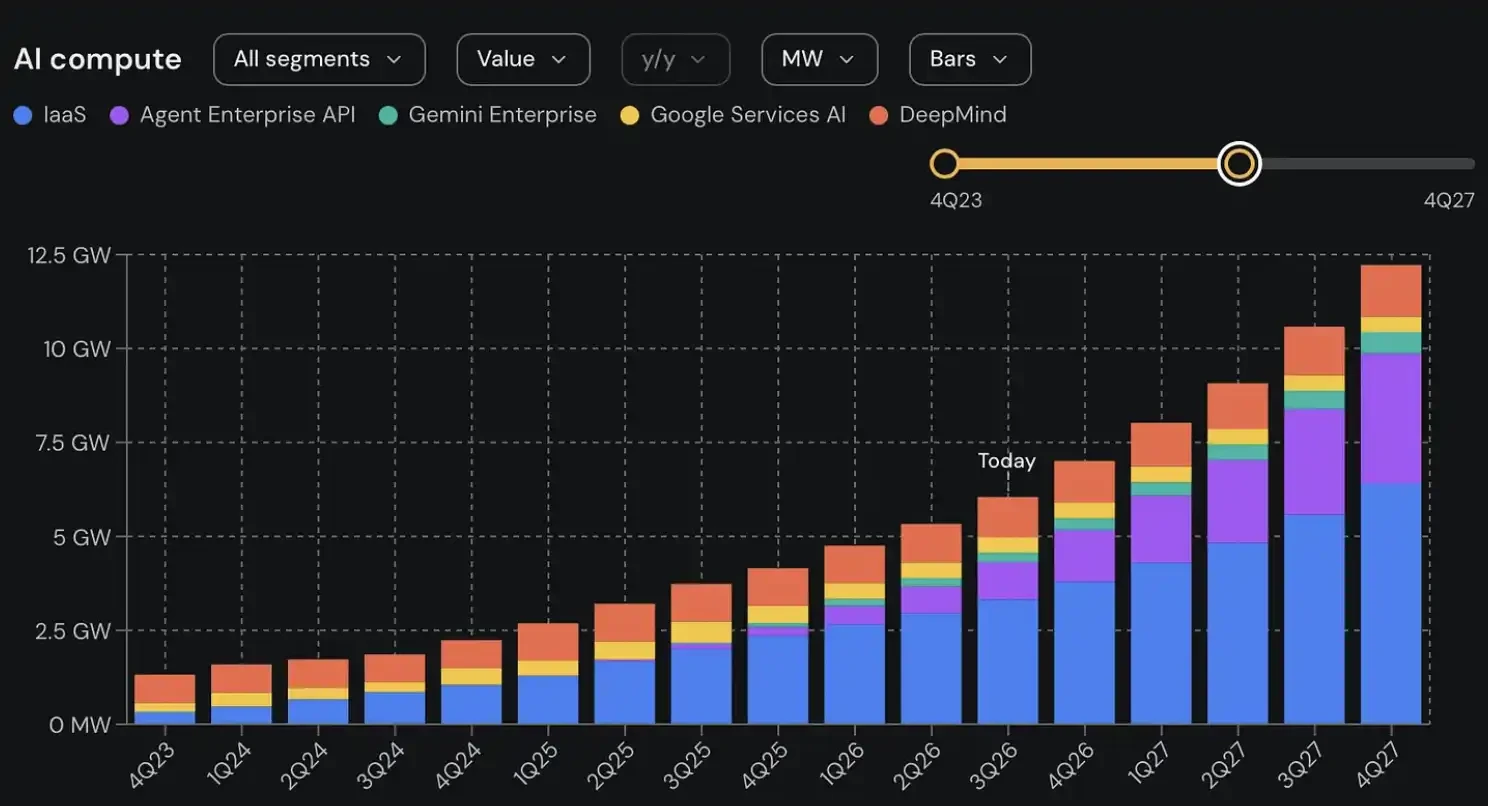

Multi-GW Computing Power Expansion Puts Meta at the Frontier Table

Computing power is the third line. In a July 2 article, SemiAnalysis stated that Meta has signed contracts for over 5GW of capacity in the first half of this year, accumulating nearly 10GW in transactions since 2024, and judges that the bulk of incremental capacity will still flow to Meta’s super intelligence lab.

For ordinary investors, the key point isn’t the specific data center design, but the direction of capital expenditure. Meta is expanding computing power not for conventional cloud services, but to prepare larger clusters for internal model training, post-training, and agent loops. The heavier the training and reinforcement learning, the more computing power deployment speed affects model iteration speed.

The report also mentions infrastructure concepts like cross-regional connectivity and rapid data center deployment. These details are still part of SemiAnalysis’s model projection, but the direction is clear: Meta is using infrastructure to buy time.

The controversy surrounding Google is not about whether it has computing power, but how it is allocated. SemiAnalysis expects that a significant portion of Google’s new data center capacity will serve its IaaS and third-party API business, and the resource concentration available to DeepMind for frontier training may be lower than outsiders imagine. Even if Google expands more AI infrastructure through external financing or capital markets, some of the new capacity could be consumed by cloud customers.

Therefore, the report presents a more controversial judgment: the competition for third place in AI is no longer a secure position for Google, but may become a reordering among Meta, Google, and other high-compute players.

The Biggest Problem Remains: Meta Has Yet to Deliver a Frontier Model

The most impactful, and also riskiest, part of this report is that it bets on the next six months, not on results already achieved.

Meta already has the $14.3 billion Scale AI deal, the addition of Alexandr Wang, compensation packages worth hundreds of millions of dollars, multi-GW computing power expansion, and internal engineering resources shifted towards RL tasks. However, these are still conditions for catching up, not a model victory in itself.

Muse Spark 1.1 currently cannot prove Meta has entered the same tier as OpenAI and Anthropic. Larger models like Watermelon are still in training; their actual capabilities, costs, availability, and developer feedback have yet to undergo market testing.

Google hasn’t left the table either. DeepMind, TPUs, Gemini, and its cloud business remain hard advantages. The real divergence is that Google’s resources must serve search, cloud, API customers, and its own models simultaneously, while Meta is concentrating more resources into its super intelligence lab.

If Meta’s next-generation model shows no significant progress, the $14.3 billion talent acquisition and massive computing power investment will become heavier capital expenditure pressure. Only if the new models and agent products deliver results will the battle for the third position in AI truly begin to shift.

Related: Leverage Wiped Out, Buying Absent: Bitcoin Still Stuck Waiting for the “Final Drop”

Original Translation: Chopper, Foresight News TL;DR: The AVIV Z-Score fell to -1.09 before retreating to -1.06, indicating that the current price has entered a deeply oversold territory relative to the cycle’s mean. The low price failed to trigger an effective rebound, and market panic continues to spread. Over 95% of short-term holders are in a loss position. The proportion of profitable supply held by short-term holders has only slightly recovered to 3.3%, far below the four-year average of 55%. The market fundamentals are fragile and highly susceptible to external shocks. The Short-Term Holder Spent Output Profit Ratio (STH-SOPR) Z-Score dipped to a low of -1.86, just 0.14 standard deviations away from the critical -2 threshold indicating deep panic selling. This suggests escalating stop-loss behavior in the market, but it has…