MetaMask co-founder leaves, leaving behind a little fox packed into an IPO prospectus

The person who built this little fox doesn’t want to build anymore.

On April 23rd, MetaMask co-founder Dan Finlay officially announced his departure from Consensys, ending a decade-long development career. The reason cited was burnout and a desire to spend more time with family.

MetaMask is arguably the most recognized product application in the 加密 world. Almost anyone who has installed a 加密 wallet recognizes the logo of that little orange fox. In 2016, Finlay and another co-founder, Aaron Davis, built this browser extension within Consensys, allowing ordinary people to interact with Ethereum without running a full node.

Over the decade, according to multiple third-party platforms, global installations have exceeded 100 million, with approximately 30 million monthly active users. The swap feature has generated over $325 million in cumulative fee revenue.

Looking through public information, I found that Finlay rarely gave interviews over the past decade. He previously coded at Apple and seems fundamentally an engineer, not someone building a public persona.

When someone like this says they’re tired, they usually mean it. But the timing of his departure makes it hard not to speculate.

Just a few months ago, Consensys hired JPMorgan Chase and Goldman Sachs as IPO advisors, aiming for a possible listing as early as this year, according to Axios.

The company’s last funding round was in 2022, with a valuation of $7 billion at the time. Since then, it has gone through at least two rounds of layoffs. Meanwhile, the $MASK token, which was hinted at since 2021, has seen no movement in five years.

Issuing a wallet token might not be that necessary; what’s more alarming is that the little fox might not be that necessary for everyone anymore.

The Default Fox, But Not a Must-Have

In the past, many dApp development docs stated step one as “Please install MetaMask first.” It was the default wallet for the industry, much like the blue Internet Explorer icon on your Windows desktop ten years ago.

The problem is, being the default is no longer the same as being the preference.

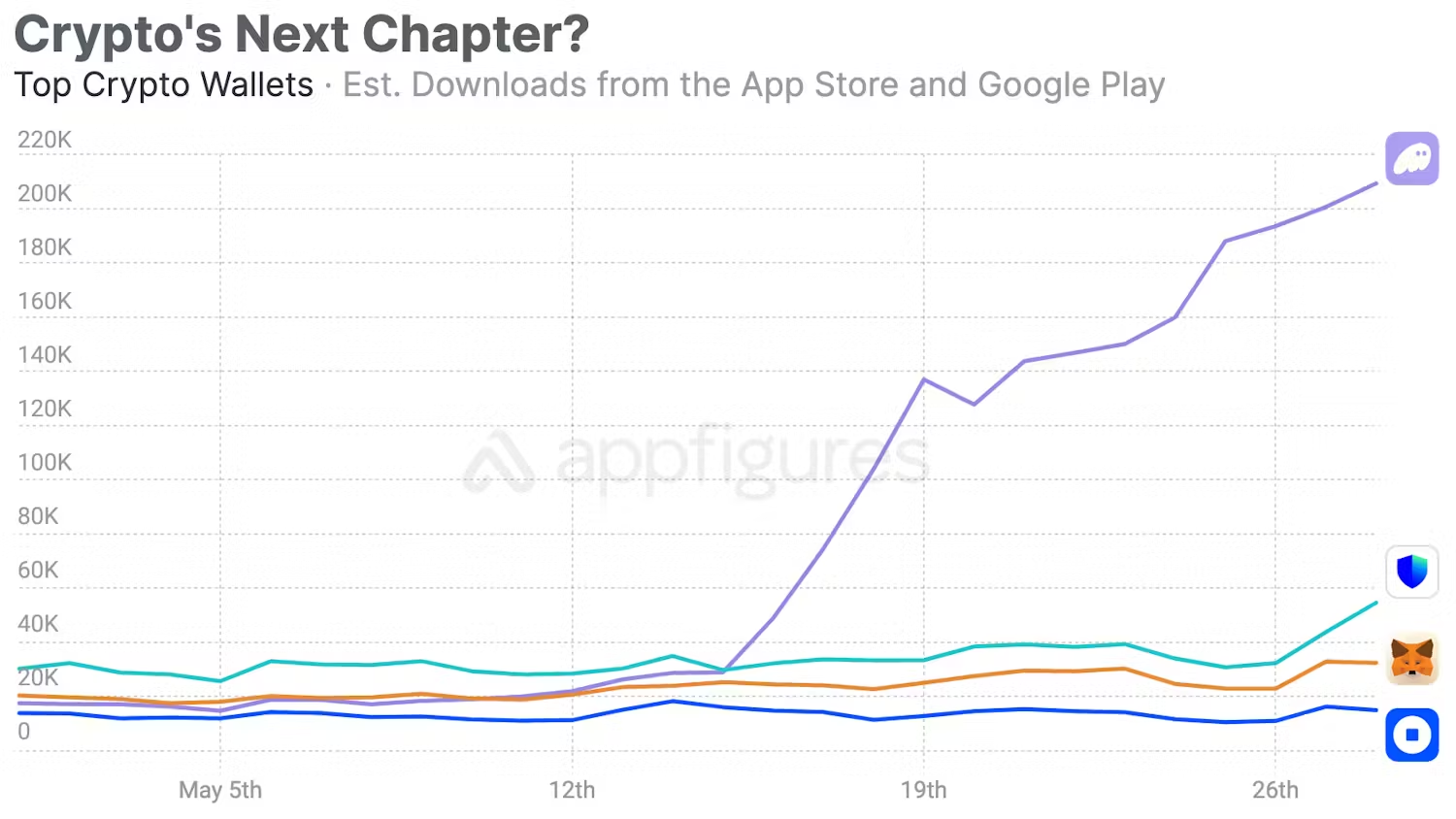

Phantom started as a Solana-only wallet and later expanded to Ethereum and Bitcoin. In January 2025, it raised $150 million in a Series C round, valuing it at $3 billion.

According to on-chain data analysis by Whales.market, Phantom’s annualized revenue is approximately $108 million, compared to MetaMask’s roughly $46 million. That’s more than double, and Phantom launched five years after MetaMask.

Phantom originated on Solana in 2021 and rode the wave of the Solana ecosystem’s revival and explosion. According to Helius, Solana’s DEX trading volume surpassed Ethereum’s in 2024. In 2025, its on-chain application revenue reached $2.39 billion, a 46% year-over-year increase. 725 million new wallets completed their first Solana transaction in 2025. When these users came in, Phantom was waiting at the door.

What about MetaMask? Native Solana support only arrived in May 2025. Before that, users wanting to access Solana through MetaMask had to install a third-party plugin called Snaps, an experience akin to installing a Chrome engine on Internet Explorer…

In those five years, Solana went from being a chain nearly killed by the FTX collapse to becoming one of the highest-volume chains. Phantom grew its valuation along with it, securing $150 million in Series C funding in early 2025, valuing it at $3 billion.

I believe MetaMask’s slowness wasn’t just a technical issue; it was also an identity problem. MetaMask is the prodigal son of Ethereum; its parent company Consensys was founded by Ethereum co-founder Joe Lubin.

Supporting Solana was expansion for Phantom but viewed as a betrayal for MetaMask. By the time the Ethereum ecosystem’s growth had demonstrably slowed down, forcing a cross-chain move, the window of opportunity had already passed.

Of course, MetaMask still has the strongest compatibility within the Ethereum ecosystem. Almost all dApps on EVM chains treat it as the default option for testing; its 30 million MAUs are not fake.

But this stickiness isn’t due to product strength; it’s due to switching costs. Switching costs can only prevent old users from leaving, not prevent new users from coming.

A person who started playing on-chain in 2025 was likely not recommended MetaMask by friends when installing their first wallet.

The Fox Waiting for the Right Price

The product is falling behind, people are leaving, but Consensys is pursuing an IPO.

According to Axios, in October 2025, Consensys hired JPMorgan Chase and Goldman Sachs as IPO advisors, aiming for a possible listing as early as this year. If successful, it would be the first company deeply tied to Ethereum’s core infrastructure to list on the US stock market.

But in the same year it hired investment banks, Consensys underwent at least two rounds of layoffs.

In October 2024, it cut 20% of its staff, around 160 people. CEO Joe Lubin cited macroeconomic pressures and regulatory uncertainty. Another round of layoffs happened in mid-2025, this time framed as “driving profitability.”

On Glassdoor, a well-known job review community, employee evaluations look worse than the layoffs themselves.

One wrote that the company lays off at least two rounds a year, targeting front-line contributors, while management is never touched. Another said that after sharing promotion aspirations with their superior, their name appeared on the next layoff list.

It’s hard to tell how much of these reviews is emotion and how much is fact. But a company significantly laying off staff just before an IPO, while employee morale hits rock bottom, is a signal in itself.

Then there’s the story of the MASK token.

In 2021, Lubin tweeted “Wen $MASK?”, causing a brief stir in the community. In 2022, he elaborated on plans for a token + DAO to drive “progressive decentralization.” In May 2025, Finlay, in an interview with The Block, responded to a question about the token’s launch with just a maybe.

For users, the MASK token was a carrot dangled in front of them to keep them using, interacting, and contributing on-chain data to MetaMask. For Consensys, the token is a card yet to be played before the IPO.

Issue it too early, and you dilute the IPO narrative; issue it too late, and the community loses patience. Now the co-founder is gone, the token is still unissued, but the IPO is on the horizon.

MetaMask’s product competitiveness is declining, a trend that will be hard to reverse in the short term. However, MetaMask’s brand recognition remains; that little orange fox is still the most recognized crypto logo globally.

The value of a brand decays at a different rate than the value of a product; brand value decays slower.

For crypto companies, an IPO often sells not just the product, but the brand plus the narrative. “Ethereum Infrastructure,” “Web3 Gateway,” “World’s Largest Self-Custodial Wallet”… these labels still work well on pitch decks for traditional investors. Lubin himself is an Ethereum co-founder, an identity that carries weight with traditional investors.

So Consensys’s choice is to package MetaMask into a public company shell and let the secondary market price it, while the brand is still valuable, the regulatory window is open, and Wall Street still has enthusiasm for crypto infrastructure.

Silence Isn’t Golden

The reaction to co-founder Finlay’s departure was remarkably muted within the crypto community. No flood of farewell posts, no sentiment about “the end of an era.” Most people don’t even seem to care about this news.

The topic of MetaMask’s co-founder leaving or staying generated less buzz than a tweet from some KOL complaining about the quality of conference swag.

That in itself says something.

MetaMask is a rare case in the crypto industry. It possesses the industry’s biggest brand, but its founders have virtually no personal brand.

In an industry where the founder is often the biggest marketing resource, MetaMask’s two founders chose to remain invisible. The product spoke for them, until the product stopped speaking effectively.

I believe MetaMask’s story is fundamentally a story about being the “default.”

In the tech industry, becoming the default is the most powerful competitive advantage, but also the most dangerous anesthetic. When you are the default, user growth happens automatically without you needing to do anything.

But this growth masks the fact that the product itself is aging. By the time you notice users are leaving, the exodus has likely been happening for a while.

Internet Explorer was the default browser, and it lost to Chrome. Nokia was the default phone, and it lost to the iPhone.

Windows Media Player was the default player, and it lost to everyone. When these products lost, their market share was still high, their brand recognition was still strong, but new users had already stopped choosing them.

MetaMask is now standing at this exact point. Existing users are still there, the brand is still loud, but new users have gone elsewhere. Consensys’s IPO plan, at its core, is about monetizing this existing user base.

At a stage where brand value exceeds product value, selling is indeed the rational choice.

The day Finlay left, MetaMask had just launched an advanced permission feature called ERC-7715. He said he looked forward to experiencing it as a regular user in the future.

A product’s creator becoming its ordinary user is perhaps the most understated and quietest farewell in the crypto industry.

But for MetaMask, how many ordinary users will still click on that little fox every day next year? Are you still using it?

本文来源于互联网: MetaMask co-founder leaves, leaving behind a little fox packed into an IPO prospectus

Related: CoinEx Research: Geopolitical Tensions Drive Up Oil and Gold Prices, Crypto 市场 Absorbs Liquidity Shock

As tensions in the Middle East escalate once again, global markets are repricing geopolitical risks. The divergent performances of crude oil, gold, stocks, and crypto assets reflect the different roles these asset classes play within the macro-financial system. Oil Prices: The Core Channel for Risk Transmission The latest escalation of conflict has sparked market concerns over potential supply disruptions in the Strait of Hormuz, driving oil prices higher. This strait handles approximately one-fifth of global oil shipments, serving as a critical hub for the transmission of geopolitical risks to the global economy. Rising oil prices not only impact energy costs but may also elevate inflation expectations and, through the bond market, affect global liquidity conditions. Currently, the upward movement in oil prices reflects more of a precautionary risk premium rather…