Morgan Stanley Analysis: TSMC Q2 Earnings Ahead – How Long Can a 66% Gross Margin Hold?

長話短說

- TSMC will hold its Q2 earnings call on July 16, with 人工智慧/HPC demand, 2nm progress, and gross margin outlook as the core focal points.

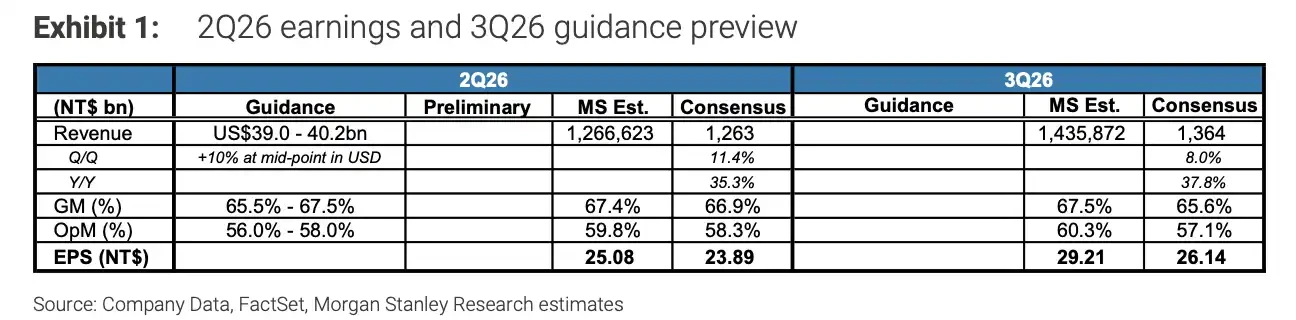

- The company reported Q1 USD revenue of $35.9 billion with a gross margin of 66.2%; Q2 guidance is for revenue between $39.0 billion and $40.2 billion, with a gross margin of 65.5% to 67.5%.

- HPC accounted for 61% of Q1 revenue, while 7nm and below advanced process nodes represented 74% of wafer revenue; high-performance computing and advanced nodes remain the growth drivers.

- TSMC expects USD revenue growth to exceed 30% in 2026, with capital expenditure trending toward the high end of the $52 billion to $56 billion range.

- AI orders remain strong, but the trajectory of 2nm ramp-up, increasing depreciation, overseas fab construction costs, and customer order pacing will all influence whether high margins can be sustained.

The focal points of this earnings call extend beyond just revenue growth. As the world’s largest dedicated semiconductor foundry, TSMC connects mobile chip clients like Apple and Qualcomm on one end, while serving AI accelerator, cloud custom chip, and high-performance computing demand on the other. The Q2 financial report will directly validate three questions: whether AI orders continue to be robust, whether the 2nm ramp-up is proceeding smoothly, and how long gross margins approaching 66% can be maintained.

Over the past year, AI demand has consistently driven up TSMC’s revenue, profit margins, and capital expenditure. The market is now more focused on whether the high growth driven by AI/HPC can continue to be translated into high gross margins.

Q2 Earnings: Can Gross Margins Hold at Elevated Levels?

TSMC has already delivered a strong set of results for Q1. The company reported first-quarter USD revenue of $35.9 billion, with a gross margin reaching 66.2% and an operating margin of 58.1%. In New Taiwan Dollar terms, first-quarter revenue was NT$1.134103 trillion, net profit was NT$572.480 billion, and EPS was NT$22.08. Revenue grew 35.1% year-over-year, while net profit increased 58.3% year-over-year.

The Q2 guidance remains at a high range. TSMC expects second-quarter USD revenue to be between $39.0 billion and $40.2 billion, with a gross margin of 65.5% to 67.5%.

This means that on July 16, what the market will scrutinize isn’t just whether revenue lands within the guidance range, but critically, whether the gross margin can hold above 65%. Current valuation and earnings expectations for TSMC are built upon the assumptions of strong AI/HPC demand, tight supply of advanced process nodes, and high capacity utilization rates.

Monthly revenue reports have already signaled sustained strong demand. TSMC’s May 2026 revenue was NT$416.975 billion, a 30.1% year-over-year increase. Cumulative revenue for the first five months of the year was NT$1.961804 trillion, up 30.0% year-over-year.

However, revenue growth does not automatically translate to synchronized profit growth. The initial phase of expanding advanced process capacity involves equipment investments, increased depreciation, and yield ramp-up costs. Ultimately, market reaction will be determined by the actual Q2 gross margin and management’s commentary on profit margins for the second half of the year.

Morgan Stanley expects TSMC’s Q2 gross margin to reach 67.4%, at the high end of the company’s guidance.

AI/HPC Remains TSMC’s Strongest Support

TSMC’s strongest growth driver currently remains AI and high-performance computing. Management stated on the Q1 earnings call that AI-related demand is “extremely robust” and raised the 2026 USD revenue growth forecast to over 30%.

The revenue structure also reinforces this assessment. In the first quarter of 2026, HPC accounted for 61% of TSMC’s revenue, while advanced process nodes (7nm and below) made up 74% of wafer revenue. While this cannot be directly equated to the AI revenue share, it clearly indicates that high-performance computing, advanced nodes, and high-end customer demand have become the backbone of TSMC’s revenue structure.

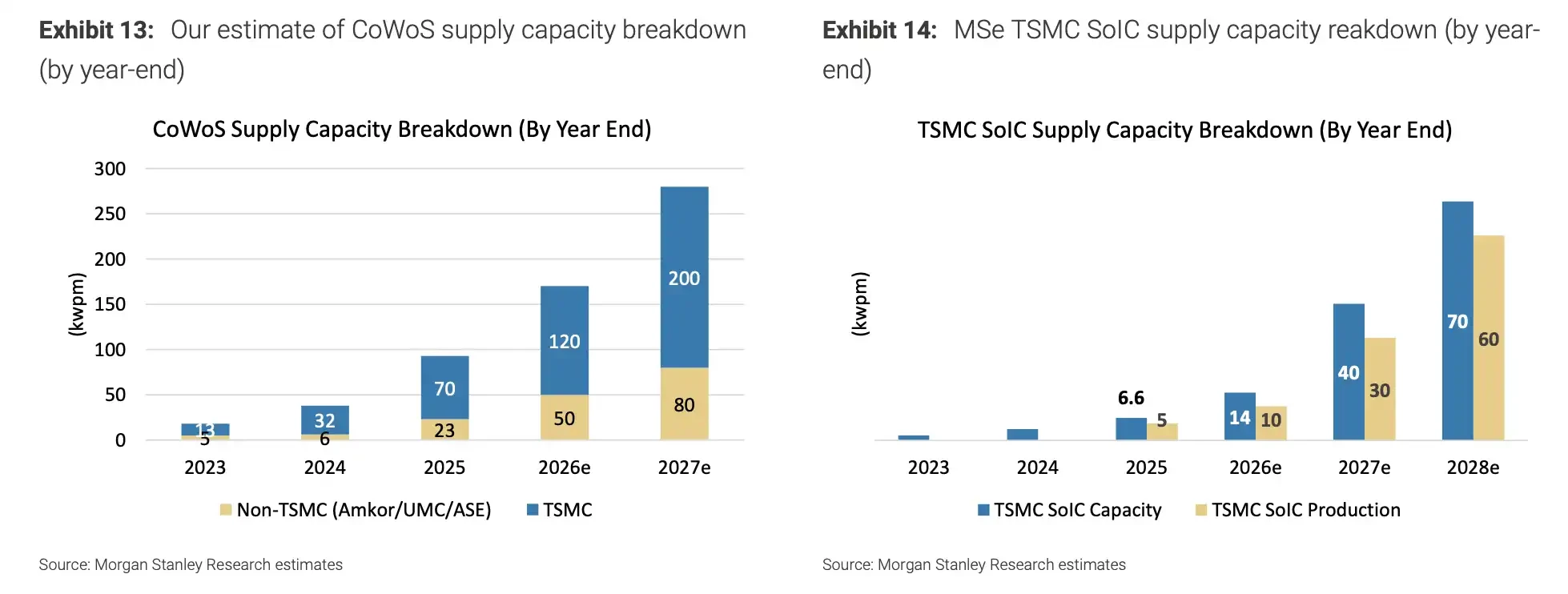

AI chip demand is driving up advanced packaging capacity; CoWoS and SoIC remain key expansion areas for TSMC.

The boost from AI chips for TSMC comes not only from order volume but also from the value per chip. AI accelerators and cloud custom chips are typically larger, more complex to manufacture, and rely more heavily on advanced process nodes and advanced packaging. This increases the value of each order and helps keep high-end capacity tight.

As long as AI capital expenditure continues to expand, TSMC can more easily maintain capacity utilization and pricing power. This is why the market views TSMC as a key earnings validation point within the AI hardware supply chain.

However, TSMC typically does not confirm specific customer orders from companies like Apple, Nvidia, or Qualcomm on its earnings calls. Investors mostly rely on the revenue structure, capital expenditure, monthly revenue reports, and management’s wording to gauge actual demand strength. Therefore, the commentary during the July earnings call regarding AI/HPC demand, customer inventory levels, and the order cadence for the second half of the year will be more important than the single-quarter data points.

Capital Expenditure Trending Higher, Increasing Margin Pressure

TSMC has 指導d its full-year 2026 capital expenditure toward the high end of the $52 billion to $56 billion range. This move indicates that management sees a long-term capacity gap driven by AI/HPC demand, rather than short-term order fluctuations.

Higher capital expenditure helps TSMC secure future orders but also brings higher costs. Investments in advanced process node production lines are enormous, and depreciation from equipment and fabs will gradually reflect on the income statement. Overseas fab construction in the US, Japan, and Germany can mitigate geopolitical risks but also introduces higher operational costs, management complexity, and supply chain costs.

Thus, capital expenditure trending toward the upper limit is a double-edged sword. When demand is strong, it signifies TSMC is further expanding its lead; when demand slows, it can quickly translate into gross margin pressure.

This is also why the market repeatedly questions gross margins. TSMC currently does not lack demand; the real point of contention is whether these orders can continue to be fulfilled at high profit margins.

The 2nm Ramp-Up Will Determine Future Profitability Flexibility

Beyond Q2 results, 2nm represents a more crucial variable for TSMC in the coming years. Management has previously stated that N2 entered high-volume manufacturing in the fourth quarter of 2025, with a multi-phase ramp-up in Hsinchu and Kaohsiung, driven by demand from smartphones and HPC/AI.

For customers, 2nm determines the performance boundaries of next-generation flagship smartphone chips, AI accelerators, and high-performance computing chips. For TSMC, 2nm determines its future pricing, capacity allocation, and gross margin levels for advanced nodes over the next several years.

The market’s focus is not solely on whether 2nm has entered mass production, but rather on how quickly supply can be expanded post-ramp, whether yields can improve as planned, and whether initial customer demand is sufficient to cover the substantial capital outlays.

If the 2nm ramp is smooth, TSMC can maintain its grip on advanced node supply during the AI demand peak and sustain its pricing power for high-end capacity. If yield rates, equipment delivery, or cost pressures exceed expectations, gross margins could face headwinds even as revenue continues to grow.

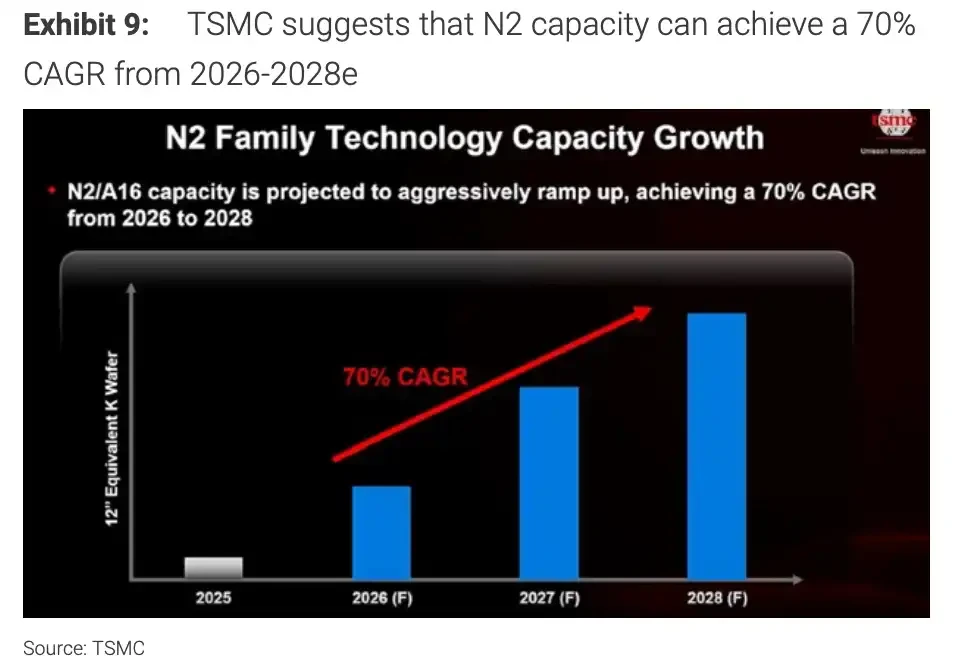

TSMC expects N2/A16 capacity to ramp up rapidly between 2026 and 2028, with a CAGR of approximately 70%.

What to Really Listen For on July 16

The key to the July 16 earnings call is not just whether TSMC meets its Q2 guidance.

More critically, it is about how management describes the AI/HPC demand outlook, advanced packaging capacity, 2nm ramp progress, capital expenditure plans, and gross margin expectations for the second half of the year.

If TSMC maintains its strong demand outlook while keeping gross margins within the 65.5% to 67.5% guidance range, confidence in the AI hardware supply chain will continue to be supported. If management signals more caution regarding customer orders, inventory, or cost pressures, investors will reassess how long the high growth in the AI supply chain can persist.

TSMC’s current strength comes from AI/HPC demand, advanced process node scarcity, and high-capital-expenditure capacity expansion. The risks are on the same chain: demand, pricing, yield, depreciation, and overseas execution. If any single link underperforms expectations, the gross margin approaching 66% will be the first to be tested.

本文源自網路: Morgan Stanley Analysis: TSMC Q2 Earnings Ahead – How Long Can a 66% Gross Margin Hold?

Related: Stock prices hit new highs, yet storage stocks still trade at a valuation trough

Today, Micron delivered a historic earnings report that has significantly boosted confidence across the semiconductor sector. FY2026 Q3 revenue reached $414.6 billion, exceeding market expectations by nearly $60 billion. A memory company, long tagged as a “low-margin commodity,” delivered gross margin guidance comparable to a software company. Its stock price surged 13% to 14% in after-hours trading, pushing its market capitalization to $1.16 trillion. Micron’s gains this year have already been substantial. Closing at $1,211.38 on June 22, it has more than tripled year-to-date and surged over 850% in the past 12 months, making it the third best-performing stock in the S&P 500 for 2026, after SanDisk and Western Digital – also memory companies. The entire sector is moving up by this magnitude. SK Hynix has risen over 800% in…