Zhipu is already worth a trillion yuan. How should Anthropic’s valuation be calculated?

長話短說

- Binance’s Anthropic Pre-IPO perpetual contract, assuming a share count of 1 billion shares, currently implies a total market cap of approximately $1.7 trillion, but this still cannot be equated to the actual clearing price of common stock.

- Related assets: Anthropic, Zhipu, Amazon, Google, AI private asset trading platforms, RWA / tokenized stocks sectors.

- Domestic large language model Zhipu has been the absolute focus of the capital market in recent days. After continuous gains without a pullback, it just reached a milestone of 1 trillion Hong Kong dollars on the Hong Kong Stock 交換.

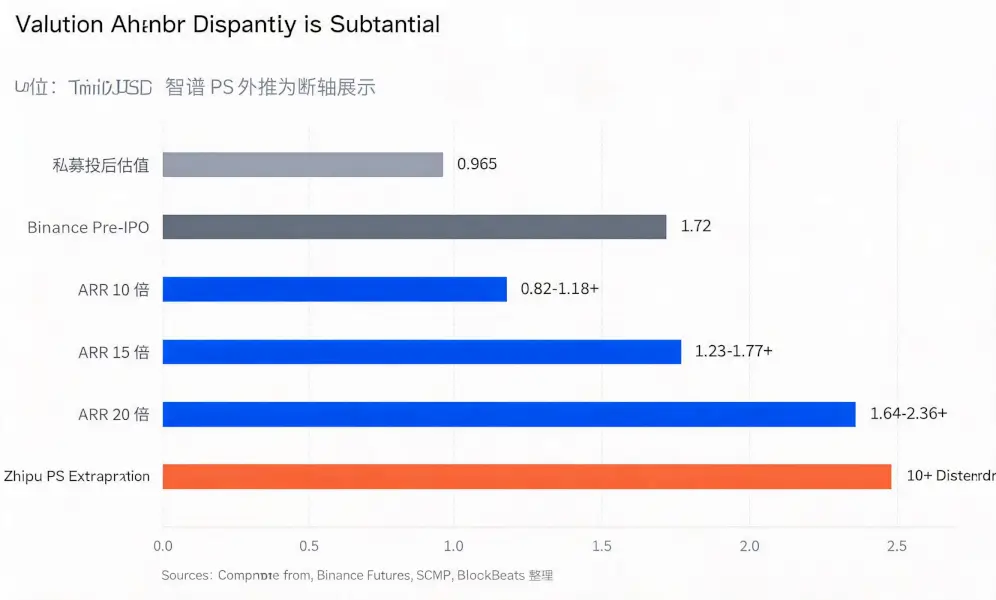

Zhipu’s commercialization path is completely benchmarked against Anthropic, as stated by CEO Zhang Peng. A few months ago, Anthropic just completed a $65 billion funding round, with a post-money valuation of approximately $965 billion.

So, a few months later, can we calculate how much Anthropic is worth based on Zhipu’s surge?

First, Let’s Calculate Using PS

According to a SCMP report, Zhipu’s 2025 revenue was 724.33 million RMB, a year-over-year increase of 131.9%, with a total loss of 4.72 billion yuan and an adjusted net loss of 3.18 billion yuan. It is still in a stage of low revenue base and significant losses. The major revaluation of its stock price and market cap in 2026 is not just trading on the current income statement, but also includes progress in domestic LLM capabilities, the substitution narrative driven by access restrictions to overseas models like Claude Fable and Mythos, the scarcity of AI targets on the Hong Kong stock market, and the amplification effect of public market liquidity on hot assets.

Based on Zhipu’s approximate 2025 revenue of around $100 million, its market cap once corresponded to a PS ratio of several hundred times. This multiple is far higher than traditional high-growth software companies and exceeds the valuation framework that most mature tech stocks can sustain.

Apply this multiple to Anthropic.

If we calculate based on Anthropic’s annualized revenue run rate of over $30 billion to $47 billion, the theoretical valuation corresponding to hundreds of times revenue would enter the tens of trillions of dollars, far exceeding the price given by current private market funding.

But $10 trillion is clearly distorted.

On-Chain Pre-IPO Has Prices, But Also Equity Gaps

On-chain Pre-IPO assets are tradable entry points provided by platforms in token form. Currently, the most well-known venue for trading Anthropic’s Pre-IPO assets is Binance.

When Binance Futures launched the ANTHROPICUSDT contract on June 2, it disclosed that the contract uses 1 billion shares, and explicitly stated that this share count is for reference only, does not represent the actual share count post-IPO, and does not constitute Binance’s endorsement of the implied valuation.

Based on the latest market data on June 22, ANTHROPIC’s latest price is approximately 1,718 USDT. Using the platform’s estimated share count of 1 billion shares, a rough calculation shows that the implied total market cap of Anthropic corresponding to the on-chain contract price is approximately $1.72 trillion. The problem is that liquidity is very poor, with only $1 million in trading volume over 24 hours.

Anthropic’s Anchor is in Revenue Velocity and Cost Curve

Besides the $10 trillion calculated by PS and the $1.72 trillion calculated from low liquidity, is there another method?

For example, identifying the two most critical variables for an AI company: Can revenue continue to grow at a high rate, and can costs continue to decline?

Traditional software companies are often priced using revenue multiples because their marginal costs are very low. Selling the 1 millionth customer a piece of software doesn’t linearly increase extra costs. But large model companies are different. Every time a user calls a model, it consumes computing power, electricity, chip depreciation, and cloud resources in the background. This is the inference cost.

If inference costs don’t drop fast enough, higher revenue could also mean higher cash burn. This is why Anthropic’s ARR and gross margin are more important than revenue alone. ARR isn’t last year’s audited revenue; it’s the annualization of the most recent month’s or quarter’s revenue, used to observe the company’s current commercialization velocity.

Valuation can start with a simple formula: Anthropic’s ARR multiplied by a revenue multiple, then discounted or given a premium based on gross margin and cloud costs.

Looking only at the IPO window, the core variable is how much ARR Anthropic can achieve before going public. Mainstream expectations from overseas buyers for the combined ARR of Anthropic + OpenAI by the end of 2026 are concentrated in the range of $140 billion to over $200 billion. If Anthropic maintains its current revenue share of approximately 59%, its corresponding ARR would be roughly $82 billion to over $118 billion. At a 10x ARR multiple, that corresponds to over $820 billion to $1.18 trillion; at 15x, over $1.23 trillion to $1.77 trillion; at 20x, over $1.64 trillion to $2.36 trillion.

This is a relatively reliable valuation algorithm for Anthropic currently.

The market essentially bets on three things being true simultaneously when willing to assign a near-trillion-dollar private valuation to Anthropic: sustained demand for Claude from enterprises and developers, the ability for scenarios like Agents and code assistants to generate high-quality revenue, and a sufficiently fast decline in inference costs to move gross margins from early low levels closer to those of software companies.

None of the Three Anchors is the Answer

So, back to the original question. Zhipu, Pre-IPO prices, and ARR multiples – three methods can each produce a number, but none can serve as the sole answer.

Zhipu provides the emotional ceiling. It shows the market is willing to pay a very high premium for scarce AI assets, but directly applying it to Anthropic yields a clearly distorted result like $10 trillion.

Binance provides the trading price. $1.72 trillion seems closer to reality, but it corresponds to a low-liquidity Pre-IPO contract, not the actual clearing price of common stock.

The ARR multiple is relatively more reliable, but it’s just a framework. Whether Anthropic’s post-IPO valuation can hold ultimately depends on whether several conditions can be met simultaneously: continued high revenue growth, enterprise and developer demand translating into stable recurring purchases, Agents and code assistants generating high-quality revenue, and inference and cloud costs declining fast enough.

If all these conditions are met simultaneously, a valuation near or even exceeding $1 trillion has support. If any one of them falters, the market will reprice Anthropic rather than continue to believe in a single attractive valuation anchor.

本文源自網路: Zhipu is already worth a trillion yuan. How should Anthropic’s valuation be calculated?

Related: SK Hynix: Can It Double Again?

TL;DR Aletheia Capital raised its SK Hynix target price to approximately $3,500, significantly higher than the target range of about $2,000 to $2,520 set by most mainstream institutions. At the core of this pricing divergence is whether the market is willing to believe that the HBM shortage, DRAM price increases, and free cash flow improvements can extend into 2027. Related tickers: SK Hynix, Samsung Electronics, Micron Technology, NVIDIA supply chain. Aletheia Capital is an independent research and investment advisory firm headquartered in Hong Kong, serving institutional investors and covering sectors such as Asian tech hardware. In contrast, publicly reported target prices are about $2,000 from SK Securities and around $2,520 from Mirae Asset and KB Securities. What makes the $3,500 target price truly aggressive is not just that it’s more…