Morgan Stanley’s First Bitcoin ETF One-Week Review: Defying the Trend to Attract Capital, a Signal of Institutional Accumulation

Author|jk

What is this ETF?

On April 8, Morgan Stanley officially launched the Morgan Stanley Bitcoin Trust (ticker: MSBT) on NYSE Arca, a platform under the New York Stock 交換, making it the first spot Bitcoin ETF in U.S. history to be issued under the name of a major commercial bank.

The fund has Coinbase serving as the 加密貨幣currency custodian and The Bank of New York Mellon handling cash and administrative duties. Its core competitive advantage lies in its annual fee rate of 0.14%. This is currently the lowest among all spot Bitcoin ETFs in the U.S. market, lower than BlackRock’s IBIT at 0.25%, Grayscale’s mini BTC at 0.15%, and Bitwise’s at 0.20%.

To briefly summarize Morgan Stanley: It is one of the top-tier investment banks and financial services companies in the United States, founded in New York in 1935; with a market capitalization of approximately $180 billion, it is one of the Global Systemically Important Banks (G-SIBs), standing alongside Goldman Sachs, JPMorgan Chase, and Bank of America as a top Wall Street institution; it consistently ranks among the top three globally in areas such as IPO underwriting, M&A advisory, and stock brokerage.

Inflow and Outflow Data for the First Week of Listing

On its first trading day (April 8), MSBT recorded a net inflow of $30.6 million, with trading volume around $34 million and over 1.6 million shares changing hands. Notably, the entire Bitcoin ETF market saw a net outflow of $93.9 million that day, with Fidelity’s FBTC and ARK 21Shares experiencing significant outflows. Only BlackRock’s IBIT and MSBT recorded positive inflows against the trend. In other words, this ETF managed to attract capital against the trend amid a market-wide outflow. On April 9, as news of U.S.-Iran ceasefire talks boosted market sentiment, the entire Bitcoin ETF market shifted to a net inflow of $304 million. MSBT continued to record a net inflow of $14.9 million, ranking third among all ETFs for the day, behind only BlackRock’s IBIT ($269.3 million) and Fidelity’s FBTC ($53.3 million).

Entering the following week (Monday, April 13), the market weakened again, with the entire Bitcoin ETF market returning to a net outflow state. On Tuesday, April 14, the situation was similar. Fidelity’s FBTC saw a single-day outflow as high as $229.2 million, and the entire market had a net outflow of $291 million. However, MSBT recorded a positive inflow of $6.28 million, making it, along with BlackRock’s IBIT and Bitwise’s BITB, one of only three mainstream Bitcoin ETFs to maintain net inflows that day.

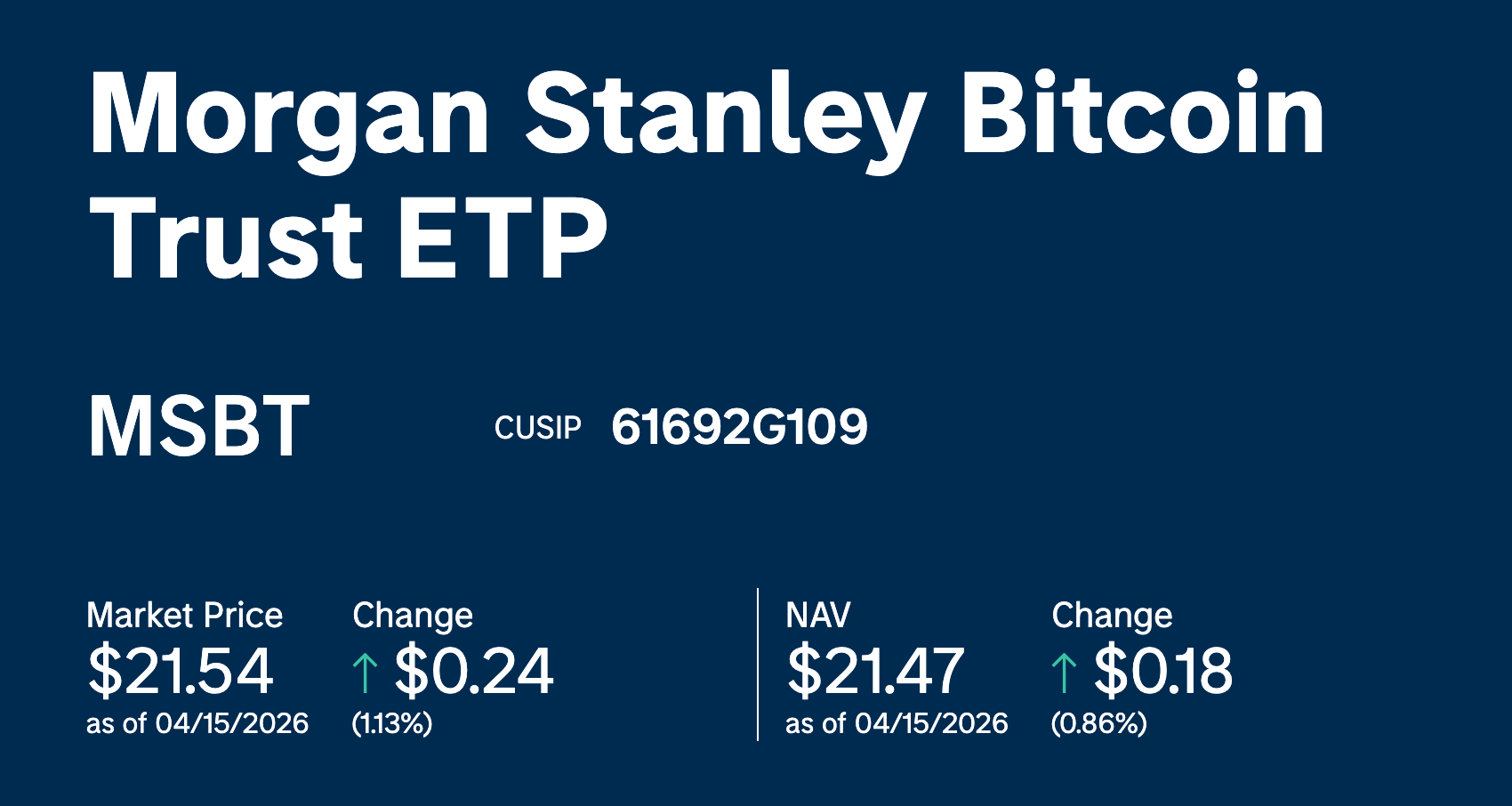

Cumulative data: Since inception, it has accumulated a net inflow of $37.5 million, with fund AUM approximately $63.84 million (according to Morgan Stanley). SoSoValue data shows $70.12 million, holding about 960 BTC. The market price shows a 0.57% premium relative to NAV. Since inception, the market price return is +6.86%, and the NAV return is +6.24%.

Behind the Data: Institutions Accumulating at Bear 市場 Lows

MSBT’s inflow data, placed in the current market context, sends a very clear signal.

After Bitcoin hit its all-time high of $126,198 in October 2025, it experienced a significant correction and is currently oscillating in the $70,000-$75,000 range, representing a drawdown of approximately 44% from the peak. Throughout the first few months of 2026, U.S. spot Bitcoin ETFs experienced four consecutive months of net outflows, with market sentiment low and retail investors exiting.

But what are institutions doing? MSBT’s data provides a good example.

First, regarding the timing of the launch, Morgan Stanley prepared this product for about 18 months, ultimately choosing to launch it at a time when Bitcoin had halved from its all-time high and market sentiment was generally pessimistic, rather than chasing the rally at the peak of a bull market. Second, this ETF has seen consecutive inflows against the trend during a period of widespread pessimism. On April 13 and 14, the entire Bitcoin ETF market saw significant net outflows (a single-day outflow of $291 million on the 14th), yet MSBT still maintained positive inflows.

This indicates that the funds flowing into MSBT are not hot money transferred from other ETFs due to fee differences.

Third, Morgan Stanley’s internal recommended allocation ratio is as high as 4%. Previously, the bank had advised clients to set their Bitcoin allocation between 0% and 4%. With the launch of MSBT, advisors now have a direct internal tool with the lowest fees. If Morgan Stanley’s approximately 16,000 wealth advisors are actively promoting allocations to high-net-worth clients, even a tiny percentage of reallocation from the $7 trillion in client assets under management could bring billions in sustained inflows. Bloomberg ETF analyst Eric Balchunas even predicts MSBT’s AUM could reach $5 billion within a year.

Goldman Sachs is Also Preparing to Enter

Finally, just six days after MSBT’s listing, on April 14, Goldman Sachs announced its application to launch its first-ever proprietary Bitcoin ETF, becoming another major U.S. bank to personally enter the fray following Morgan Stanley.

However, Goldman’s product is fundamentally different from MSBT. This fund, named the “Goldman Sachs Bitcoin Premium Income ETF,” employs a Covered Call strategy, aiming to generate consistent premium income by selling options while maintaining Bitcoin exposure. Following the application process, it is expected to officially list as early as late June to early July 2026.

The fund will allocate at least 80% of its net assets to Bitcoin-linked instruments, including spot Bitcoin ETPs, related options, and Bitcoin ETP index options, while employing a covered call strategy to generate monthly income. The specific operation is: the fund dynamically adjusts the proportion of options sold between 40% and 100% of its Bitcoin exposure. This range design allows the fund to continuously collect option premiums in sideways or mildly rising markets. However, during significant Bitcoin rallies, as upside gains are capped, the fund’s performance will lag behind pure spot ETFs.

Simply put, this is a structure that “trades some upside potential for stable cash flow”—regularly distributing option premiums to holders. It is suitable for investors who want exposure to the Bitcoin narrative but prioritize stable cash flow over full price appreciation. Bloomberg ETF analyst Eric Balchunas therefore jokingly called it “Boomer Candy,” tailor-made for traditional institutional investors who want a piece of the Bitcoin pie but can’t stomach the volatility.

Goldman’s entry subsequently drove a single-day market-wide inflow of $411.5 million. This means, there’s no need to panic in a bear market; top Wall Street institutions have already begun collectively positioning.

結論

MSBT’s first-week numbers don’t appear particularly eye-catching at first glance. The cumulative inflow of $37.5 million is negligible compared to BlackRock’s IBIT with its $55 billion size. However, the signal itself is very significant: a century-old institution managing $7 trillion in wealth, entering the market with the lowest-ever fee rate amid a 44% Bitcoin correction and extremely pessimistic sentiment, and relying on 16,000 advisors to continuously push allocations to high-net-worth clients. For readers focused on institutional movements, MSBT’s weekly inflow data will become an important window to observe Wall Street’s true stance moving forward.

Related: The Endgame of Crypto Neo-Banks: Licenses, Stablecoins, and Super Apps—Who Will Prevail?

Original Compilation: Chopper, Foresight News If you ask ten 加密貨幣 users what a neobank is, you might get the same answer: a card that allows spending with stablecoins. But if you ask ten developers, the answers could be all over the place. Some are developing non-custodial wallets linked to Visa cards; others are forking Aave and calling it a savings account; and still others are applying for full banking licenses. Monthly transaction volume for crypto debit cards grew from around $100 million at the beginning of 2023 to over $1.5 billion by the end of 2025 (a 106% CAGR), with the market’s annualized scale exceeding $18 billion. Card spending linked to stablecoins reached $4.5 billion in 2025, a 673% year-over-year increase. However, the entities actually processing this volume are highly…