Trade.xyz Pricing the World? On-Chain Markets Are Becoming the Market Itself

Original Author: @kelxyz_

Compiled by: Peggy, BlockBeats

Editor’s Note: Since early 2026, Trade.xyz has rapidly gained momentum. In mid-March, its partnership with S&P Dow Jones Indices to launch officially licensed S&P 500 perpetual futures was seen as the first instance of traditional financial assets entering the on-chain trading system in a 7×24 format. Coupled with sustained growth in trading volume and open interest, Trade has become one of the most watched projects within the Hyperliquid ecosystem and is considered a key case study for “TradFi asset on-chain perpetuals.”

The author argues that as on-chain perpetual futures begin to cover traditional financial assets, Trade.xyz is transitioning from an “execution tool” to a “pricing center.” Since its launch in 2025, Trade has established a first-mover advantage through liquidity, product expansion, and brand partnerships. From mật mã-native assets to traditional assets like the S&P 500 and commodities, its markets are not only meeting trading demand but are also starting to participate in price discovery. A more significant change lies in the pace—the market is shifting from “reacting to news” to “predicting news,” and in some scenarios, even driving price changes ahead of time.

In the author’s view, Trade’s core competitiveness stems from a “flywheel” composed of liquidity, user experience, capital efficiency, and brand, and it has already shown early signs of a dominant player in the “Gorilla Game,” poised to take a leading position in the tradfi perpetual futures arena.

However, this lead is not yet secure. Homogeneous competition, incentive mechanisms, regional and brand differentiation, technological paths, and the involvement of traditional institutions and regulation could all reshape the landscape. The key question is not the growth rate, but whether its structural advantages can be continuously strengthened.

Building on this, the author further points out that as the on-chain market represented by Trade takes shape, a series of opportunities are emerging—from arbitrage, rates and funding rate trading, to microstructure research, high-yield products, conditional markets, and agent systems. This article accordingly identifies several directions worthy of close attention from developers, investors, traders, and researchers. These paths collectively point towards a faster, more continuous, and more reflexive market environment.

So, is it possible for Trade.xyz to evolve from a high-growth trading platform into a key piece of infrastructure in a new generation of financial markets?

The following is the original text:

Those who can identify and grasp “reflexive technological revolutions” often reap the greatest rewards in globally-scaled “winner-take-all” markets.

This article will focus on the market technology revolution led by Trade. In this revolution, as perpetual futures continue to expand across various asset classes, permissionless leverage will intersect with technologically autonomous systems at internet speed.

Some judgments for the coming years: On-chain perpetual futures will gradually shift from “reacting to news” to “predicting news,” then to “front-running news,” and ultimately even “making news.” Perpetual futures covering traditional financial assets will generate over $10 billion in annual revenue for trading platforms.

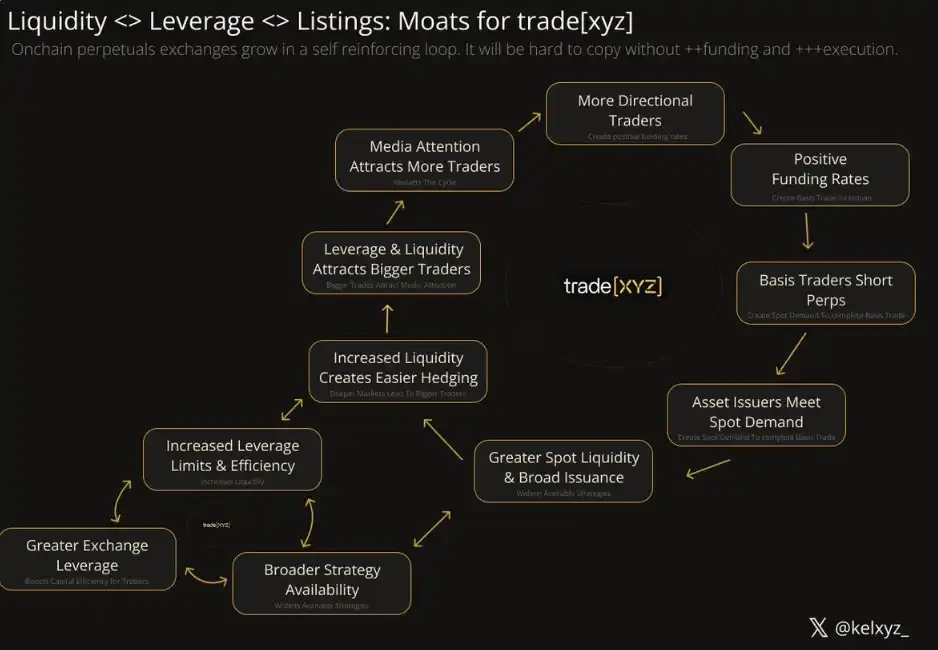

The flywheel of liquidity, market access, brand partnerships, user experience, and capital efficiency built by trade.xyz will allow it to capture the largest share of value in this market.

We will see multiple multi-billion dollar macro hedge funds liquidated in real-time on-chain. Garrett Bullish’s high-profile liquidation of hundreds of millions of dollars is just the beginning.

The next “Roaring Kitty” will profit from a cross-jurisdictional short squeeze, and the counterparties will be unable to manually press a “pause button.”

As autonomous agents expand in duration and capability, compute-sensitive agents will utilize the permissionless leverage provided by Trade, combined with automated “persuasion capabilities,” to create and monetize market volatility.

1. The “Second Act” of Perpetual Futures

Between 1997 and 2008, Blackberry created approximately $80 billion in value for shareholders, with company revenue peaking at $20 billion in 2008. Over these 11 years, its smartphones achieved unprecedented cultural influence. In a sense, smartphones had already changed the world.

But that was just the first act.

By 2025, Apple’s revenue reached $416 billion, with the iPhone product line alone contributing $209 billion.

If the first act was the expansion of market size, the second act was the reshaping of the “relationship between people and information”—a change that was nearly impossible to foresee at the time. Beyoncé sleeping with a Blackberry was, at most, a distant cultural archetype; later, Netflix, leveraging smartphones, directly competed with “sleep itself” and grew into a company worth hundreds of billions of dollars.

Perpetual futures are at a similar inflection point.

Their first act was futures trading around crypto-native assets, creating trillions of dollars in trading volume and giving rise to a batch of companies worth billions or even tens of billions of dollars, including Hyperliquid.

On the surface, perpetual futures are not complex: they are contracts without an expiry date, pegged to the price of an underlying asset. Of course, they involve complex pricing mechanisms, but at a macro level, that’s their structure. And when such contracts begin to be applied to traditional financial assets, they have already started to make news, even “pricing news” in advance. In just a few months, we have seen the embryonic form of their second-order effects.

2. Capital Flowing at the Speed of Information

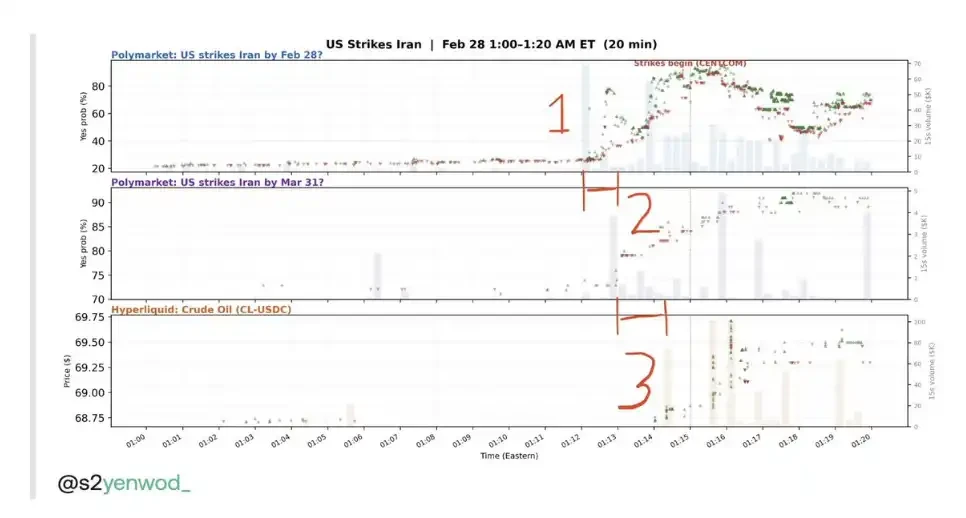

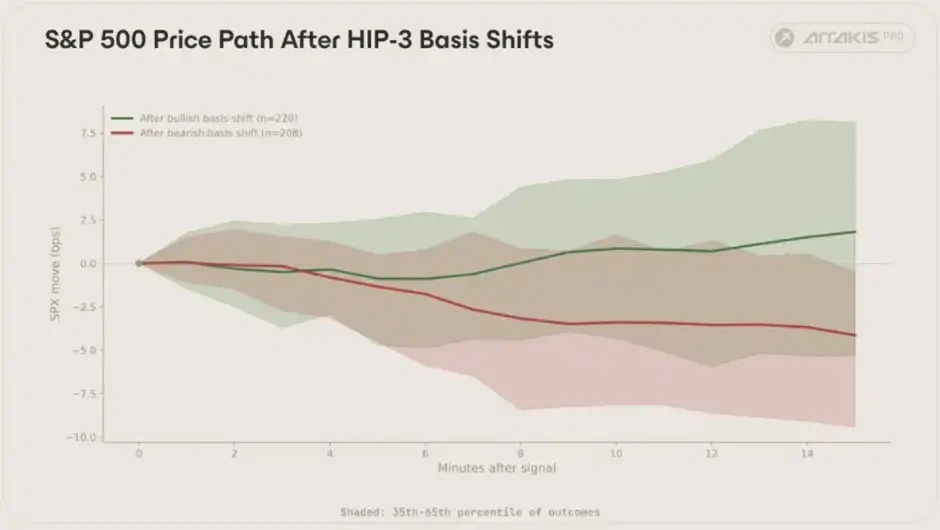

Trade’s market reaction speed to news is accelerating, a point particularly evident during the Iran attack incident a month ago.

Source: yenwod

In this emerging 7×24-hour “speed game,” Trade primarily competes with prediction markets for the title of “world’s fastest” pricing power. The current landscape is:

· Anonymous news accounts first release information on social media

· Professional traders (sharps) on Polymarket react first

· Trade’s market reaction is relatively slower, but liquidity is significantly stronger

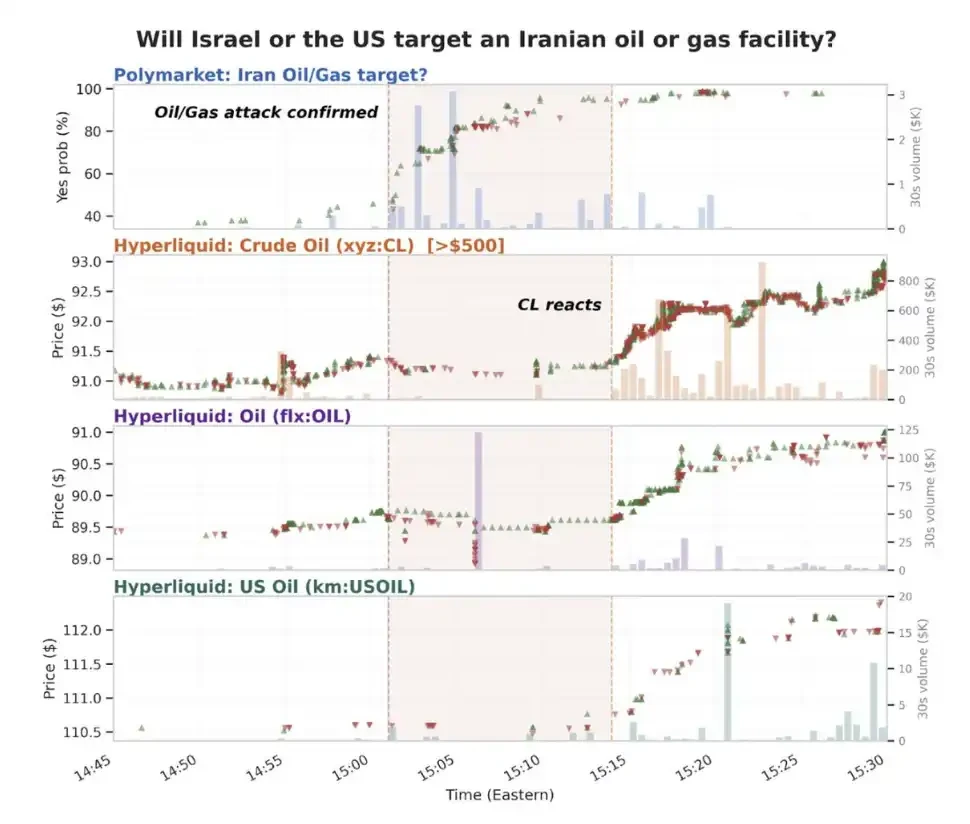

Source: yenwod

The endgame will be completely different. The phase where “news precedes market volatility” will not last long; the market will begin to move abnormally before the news even happens.

We expect Trade to replace Polymarket and occupy the position of “speed advantage,” mainly for three reasons:

First, compared to Polymarket, Trade’s potential profit space increases by orders of magnitude due to its higher liquidity.

Second, Polymarket’s current speed advantage largely stems from the political attention accumulated after the 2024 election; Trade has only entered the mainstream spotlight for a few weeks.

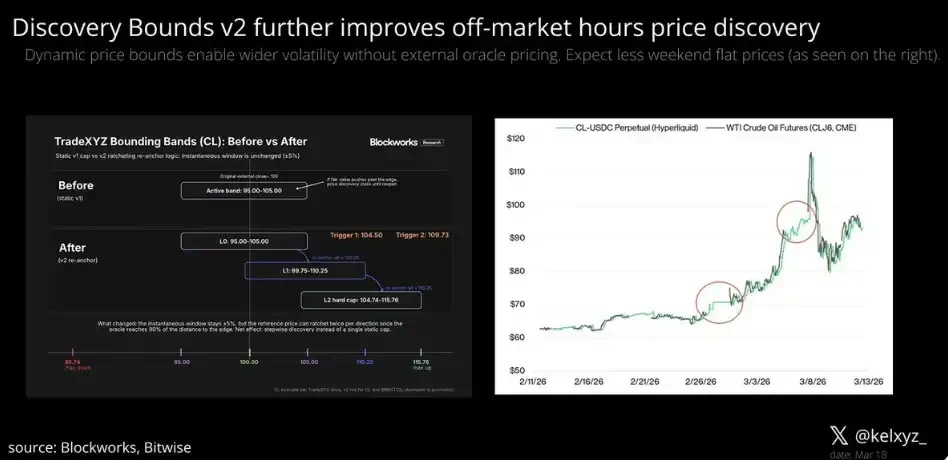

Third, Trade’s market was initially constrained by the Discovery Bounds v1 design—a risk management mechanism used to keep “abnormal market prices” within a reasonable range. With the launch of Discovery Bounds v2, the system will have greater price flexibility during non-trading hours while still maintaining robust risk control.

Source: Steven x Bitwise

Trade has already shown signs of market pricing shifting from “passive reaction” to “active guidance.” In the future, these markets will run ahead in the direction “where the news is about to happen” before the news even occurs.

Microstructure

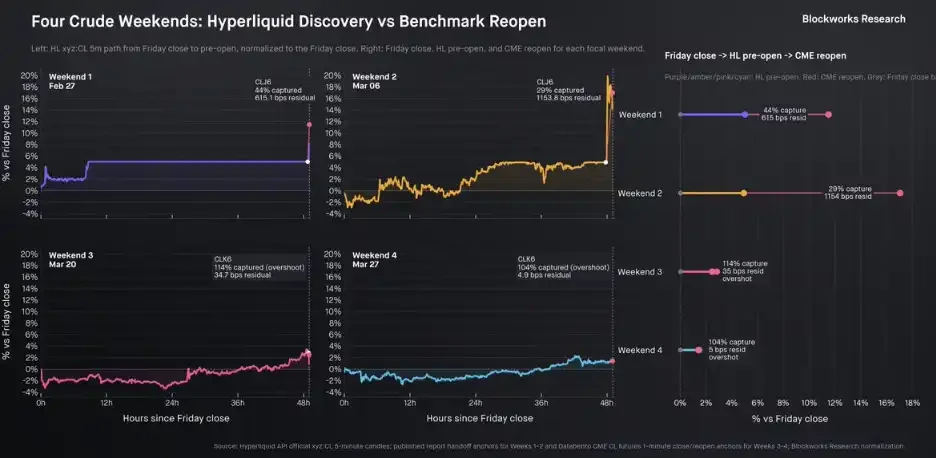

Analysis from Shaun DeDevens (Blockworks) has consistently been one of the most valuable references in the field of market microstructure. His latest research focuses on “weekend price discovery.”

During the recent Easter long weekend, social media-driven sentiment and trading behavior combined to cause sharp market volatility again, particularly evident in oil-related assets.

The key points are as follows:

The resulting volatility is highly attractive to traders. During the weekend, the median trading volume in commodity markets, primarily on trade.xyz, has surged from approximately $150 million to over $1 billion, a 7-fold increase.

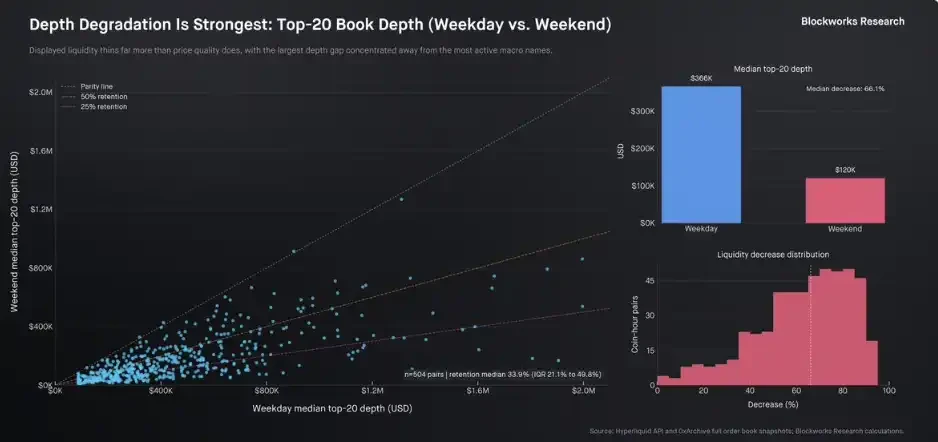

Initially, weekend liquidity seemed to drop significantly—median liquidity across all markets fell by about 66.1%. However, at the same time, the liquidity in the top markets contributing the majority of volume remained largely at levels similar to weekdays.

His silver market microstructure analysis is also worth reading (and was the original focus of this section). These studies collectively point to a core conclusion: “Hyperliquid and Trade.xyz have proven that 7×24-hour on-chain markets are playing an increasingly important role in the price discovery process of traditional assets.”

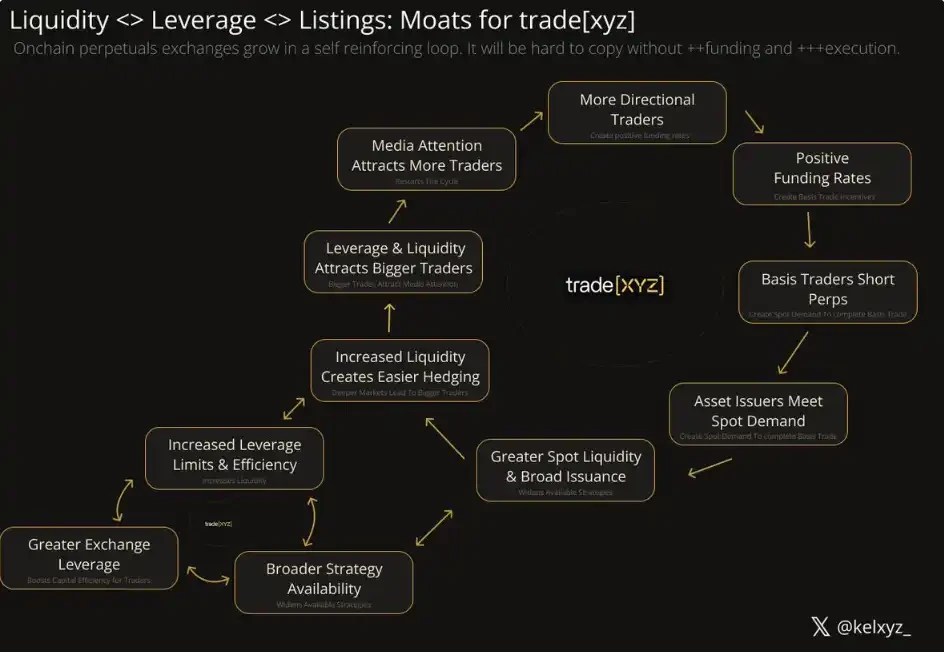

3. Gorilla Game: Moats and Competition

Geoffrey Moore’s “Gorilla Game” provides a classic framework for analyzing high-growth technology industries. Its core logic is simple: companies that dominate in the early stages often grow into “Gorillas” and dominate the market for a long time until new technological innovations restart the next round of competition.

This framework posits that the key to investment and identifying “winners” concentrates on two stages:

· Application Layer: Penetration capability in early niche markets

· Infrastructure Layer: Expansion capability after entering the high-growth phase

But currently, an increasing number of companies and protocols (including Trade) exhibit a degree of vertical integration, blurring the boundary between “application” and “infrastructure”—and making the distinction between “infrastructure-level penetration” and “application-level growth” less clear.

How to accurately bất chấpne these positions will become key to understanding the competitive landscape, making investment decisions, and identifying the ultimate winners.

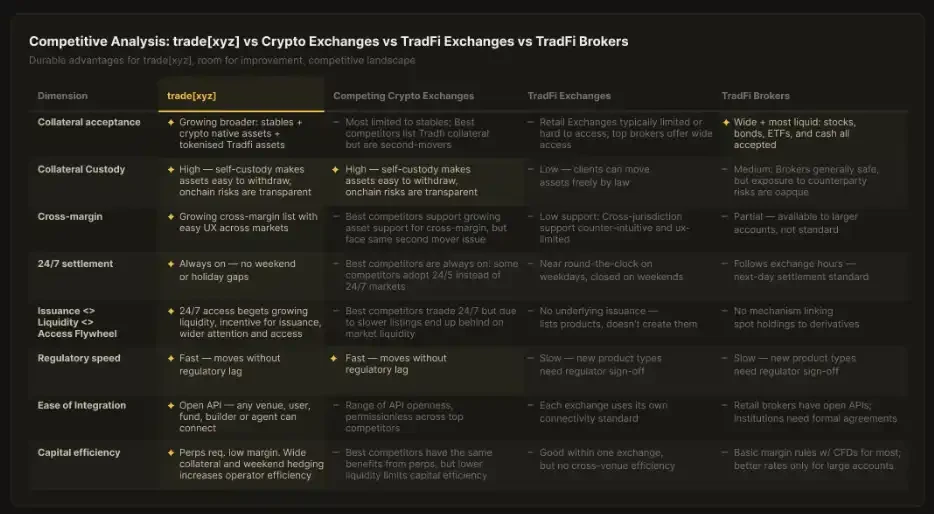

Since its launch in October 2025, Trade has achieved record growth (annualized fees are approaching $100 million), established an official partnership with the S&P 500, and taken a leading position in multiple market metrics. In terms of product form, Trade is gradually evolving into a “Gorilla” in the traditional finance perpetual futures space.

According to Geoffrey Moore’s framework, becoming a “Gorilla” typically relies on four types of core competitive advantages:

1. Customer Scale Advantage (Driven by Media Exposure and Partnerships)

Acquiring more users through large-scale media coverage and key partnerships. Trade has been featured multiple times on Bloomberg, The Wall Street Journal, and partnered with S&P Dow Jones Indices (SPDJI), clearly leading its peers in this dimension.

2. Higher Barriers to Entry (Increasing Switching Costs Through Technical Details)

Increasing user migration costs through a series of “implicit” technical optimizations. This part remains a relatively weak link, but mechanisms like portfolio margining, native spot markets, and fee reduction through growth models are beginning to show initial effects.

3. Economies of Scale (Reducing Costs Through Liquidity and Reputation)

Liquidity itself attracts more liquidity, and brand effects further amplify the advantage. Trade’s HIP-3 native competitors—theoretically also benefiting from Hyperliquid’s brand endorsement—consistently lag in liquidity competition for similar markets. Taking the S&P 500 market as an example, Trade’s trading volume surpassed that of other, longer-running similar markets in less than a day after launch.

4. Premium Pricing Power (Pricing Power from Industry Standard Status)

This is still difficult to conclude definitively, but a potential signal is: even with zero-fee competitors (like Lighter), Trade’s market prices have repeatedly traded at a premium.

These advantages are significantly powerful individually, and once combined, they may determine the final landscape of the entire market.

Although the logic of “self-reinforcement, leading all the way” is quite clear, competitors still have multiple paths to vie for the position of “King of Stock Perpetual Futures.” There will be at least a second winner, and it’s not impossible for a competitor that truly challenges Trade’s early advantage to emerge. The main paths include:

1. Product Commodification

Well-funded, resource-rich competitors may level the playing field through a “commodification” strategy. If Trade’s advantages in liquidity acquisition and brand are weakened, competition will reset to the same starting line—especially before “premium pricing power” and “user switching costs” are truly established. This pattern is common in many VC-backed industries: latecomers, while not completely replacing the first mover, can still capture a significant market share.

Projects represented by Lighter are adopting this exact strategy—attracting retail traffic with top-tier capital backing and “zero fees.” Although the market response has been tepid so far (its token has performed poorly since launch), forward-looking capital is still betting on a potential reversal.

2. Incentivization

Traditional “airdrop farming” has been largely exhausted in the crypto industry; token incentives alone are insufficient to build long-term competitive advantages. Historically, few successful cases, such as Uniswap vs. SushiSwap, Compound vs. Aave, all combined incentives with product advantages or other competitive elements. Aave, in particular, ultimately won the Gorilla Game in the lending track through “incentives + product leadership.”

For tradfi perpetual products, incentives alone cannot break through; they must be combined with other differentiated approaches.

3. Brand and Regional Differentiation

A frequently overlooked case is PancakeSwap—compared to SushiSwap, it achieved more lasting success through a combination of incentives, resource support, and “brand + regional positioning.”

A more typical example comes from centralized exchanges: such as Bybit, Upbit, etc., which achieved significant growth by focusing on different user groups and communities.

Potential paths include:

· Regional differences (e.g., edgeX targeting Asian users)

· User type segmentation (e.g., Architect targeting institutions, edgeX focusing on mobile)

· Channel partnerships (e.g., Lighter’s partnership with Telegram Wallet)

The key competitive question is: against the backdrop of the leader continuously expanding horizontally (covering regions, brands, distribution channels), can these differentiated “wedges” be solid enough and further extend into deeper competitive moats?

4. Technical Differentiation

Currently, the Hyperliquid infrastructure that Trade relies on is at the industry forefront in terms of performance. But the performance race has no finish line.

New scaling paths (like LayerZero, Fogo) or liquidity mechanisms (like Ostium, Variational, Extended) may construct new competitive dimensions. In a market extremely sensitive to “latency,” technological breakthroughs theoretically possess disruptive potential.

But the question remains: whether these performance improvements, still in the theoretical stage, can translate into liquidity and market share growth in reality remains to be seen.

5. Incumbent Counterattack and Regulation

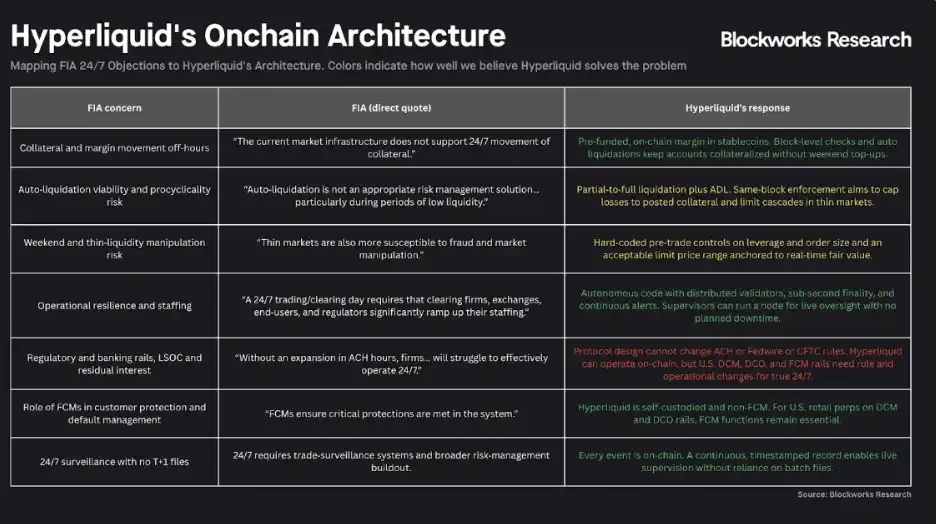

According to Geoffrey Moore’s framework, in the early stages of a market, incumbents often compete while simultaneously pushing to raise industry entry barriers.

This trend has already emerged. Regulatory-related bodies from the Futures Industry Association have expressed clear concerns about the 7×24-hour markets based on the Hyperliquid and Trade architecture, issuing strongly worded public letters.

Overall, competition does exist, but the barriers are rising rapidly. The real question is no longer who can “enter this market,” but who can, after entering, continuously build sufficiently thick structural advantages.

Source: Blockworks

Well-funded traditional institutions with regulatory resources may try their best to slow the development of on-chain markets while accelerating the launch of their own “compliant alternatives.”

This is one of the most frequently mentioned competitive risks—participants with high market capitalization, strong distribution capabilities, ample liquidity, and deep political influence, such as the traditional brokerage system, Robinhood, etc., may all enter Trade’s market.

But the “regulatory advantage”

Bài viết này được lấy từ internet: Trade.xyz Pricing the World? On-Chain Markets Are Becoming the Market Itself

Related: Odaily Editorial Team Tea Talk (March 11)

The content of this column is based on the real investment and observation experiences of Odaily editorial team members. It does not accept any form of commercial advertising, nor does it constitute investment advice (after all, we are equally experienced in losing money). Its purpose is solely to broaden perspectives and supplement information sources, not to manufacture consensus. Welcome to join the Odaily community (Telegram Discussion Group, X Official Account) to exchange ideas, question, and banter together. Wenser (X: @wenser2010) Introduction: Crypto abstractionist, crypto enthusiast for fun, sharp-tongued critic Sharing: 1. After late January, OpenClaw experienced its own “public discussion frenzy.” I’ve been researching it these past couple of days as well. My preliminary conclusion after looking into it is: ordinary people might as well make good use of Claude Code or…