Stop Focusing Solely on Oil Prices; the Bond Market is the Real Bellwether

Original Author: The Kobeissi Letter

Compiled by: Peggy, BlockBeats

Editor’s Note: Against the backdrop of escalating geopolitical conflicts, the market’s focus is quietly shifting. Initially, discussions centered on oil price shocks and the Middle East situation. However, as the war enters a stalemate phase, a more systemic variable is emerging: financial conditions themselves are tightening.

The core thesis presented in this article is that what truly dominates the current market is no longer the war itself, but the disorder in the bond market.

Over the past month, the rapid rise in the U.S. 10-year Treasury yield has directly reshaped interest rate expectations, shifting from a “rate cut path” to a “re-discussion of rate hikes,” and has exerted pressure on stocks, commodities, and even policy space. In this process, the persistent weakness in the labor market and the renewed rise in inflation expectations have amplified the Federal Reserve’s dilemma.

More notably, the author places this round of market volatility within the policy reaction function: when yields approach the 4.50%–4.70% “policy shift zone,” the probability of government intervention will rise significantly. Whether it’s the historical tariff suspension or recent changes in the pace of “peace talks,” both are interpreted as concrete manifestations of bond market pressure transmitting to the policy layer.

This leads to a deeper question: when the bond market begins to dominate asset pricing and policy pace, what signals should market participants follow? Geopolitical narratives, or the marginal changes in the yield curve?

In this round of structural shift, this article attempts to provide a clear answer—watch the bond market. Because it not only reflects risks but also determines the boundaries of risk.

The following is the original text:

As peace talks for the Iran war stall, an urgent question is emerging in U.S. markets: the bond market is “breaking down.” Amid severe bond market turbulence, we believe the probability of “intervention” is rapidly rising. What does this mean? Let’s explain below.

Before we begin, we suggest you bookmark this article; it will serve as a reference گائیڈ for market movements in the coming weeks.

When the Iran war broke out on February 28th (beginning with the U.S. and Israeli assassination of Iran’s Supreme Leader Khamenei), oil prices initially rose by less than 15%. The U.S. assessment at the time was that assassinating Khamenei would quickly trigger a regime change in Iran, leading to a relatively fast and less disruptive outcome. But as of now, the Iran war has entered its 27th day. The “15-point peace plan” proposed by the U.S. has been rejected by Iran, and peace talks have clearly stalled.

It is now uncertain whether any party still clearly desires to end this war. Consequently, oil prices remain elevated, with WTI crude again approaching $100 per barrel. But this is no longer the biggest problem facing the market. The real issue has shifted to the bond market and how it is rapidly evolving into the largest source of headwinds for the global economy.

The Core Issue

In the early stages of the war, oil prices were the market’s focus, and they still are to some extent. The reason is simple: the oil market most directly and rapidly reflects the war’s impact.

But now, the bigger problem is: the sudden surge in U.S. Treasury yields.

As shown below, over the 27 days since the Iran war began, the U.S. 10-year Treasury yield has risen from about 3.92% to 4.42%, a cumulative increase of 50 basis points. Remember, before the war broke out, the market’s focus was on: how many rate cuts would occur in 2026.

U.S. 10-Year Treasury Yield Since the Iran War Began

The current pace of increase in the U.S. 10-year yield, and the broader rise in Treasury yields, is roughly equivalent to the performance during the “Liberation Day” period in April 2025.

But the context this time is far more complex, and stabilizing the bond market is much less straightforward than it appears on the surface. This will soon become the market’s core narrative.

From Rate Cut Expectations to Rate Hike Pressure

To better understand the intensity of this shift, recall market expectations for interest rates at the end of 2025.

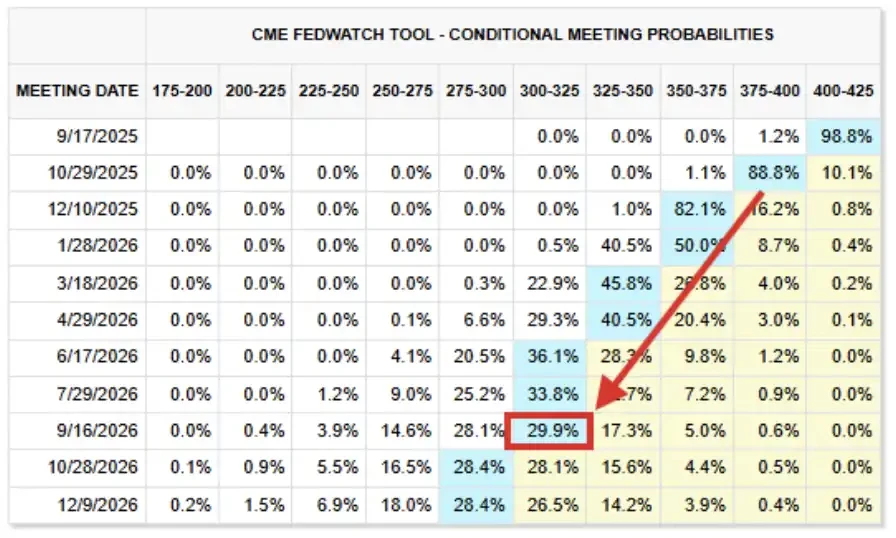

As shown below, the market’s “base case” at that time was: by 2026, the Fed’s federal funds rate would fall to the 2.75% to 3.00% range. There was even over a 25% probability that rates would fall even lower.

2026 Rate Expectations (Screenshot from September 2025)

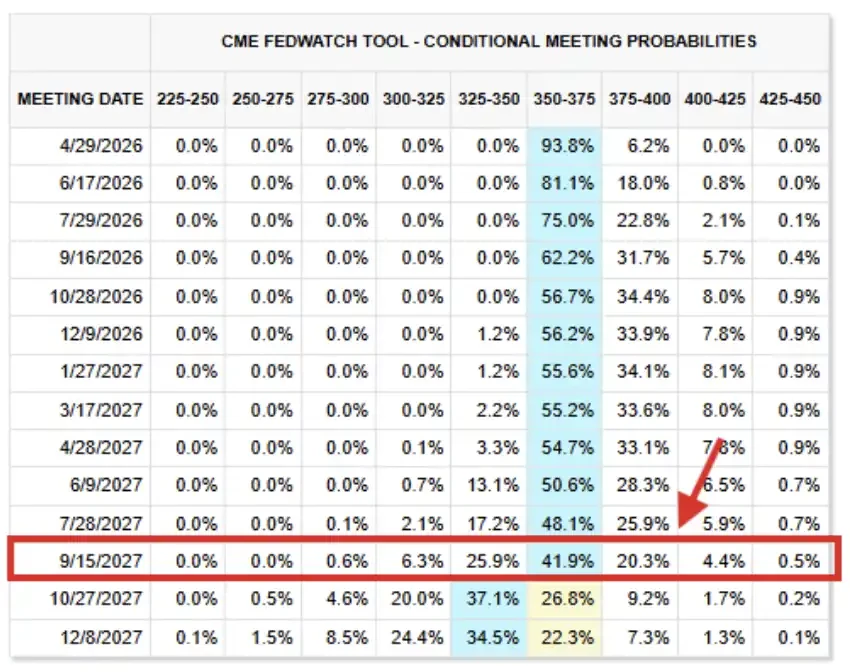

Now look at the current pricing from interest rate futures. Today’s “base case” shows: rates will essentially remain at current levels until September 2027, with the Fed’s federal funds rate expected to be in the 3.50% to 3.75% target range.

This is 75 to 100 basis points higher than expectations just a few months ago, and this outlook now extends to the end of 2027.

Interest Rate Futures as of March 26, 2026

In fact, the market has begun discussing the possibility of “rate hikes” again: there is currently about a 43% probability that the Fed will hike rates before the end of 2026. Objectively, the market can hardly withstand such a shock.

Next, we explain why.

The Labor بازار Will Only Get Worse

On September 17, 2025, the Fed cut rates as widely expected and signaled two more cuts before year-end. At that time, although inflation was still significantly above the Fed’s long-term 2.00% target, concerns about the U.S. labor market were intensifying.

In the post-meeting statement, the FOMC described economic activity as having “slowed” and added that “job gains have moderated,” while noting inflation “has risen and remains elevated.” Weak employment and rising inflation actually represented deviations from both of the Fed’s dual mandates of “price stability” and “maximum employment,” but the labor market issue was more prominent at the time.

Fast forward to today, the labor market situation has only worsened. Compared to September 2025, the market’s ability to withstand higher rates is actually weaker now.

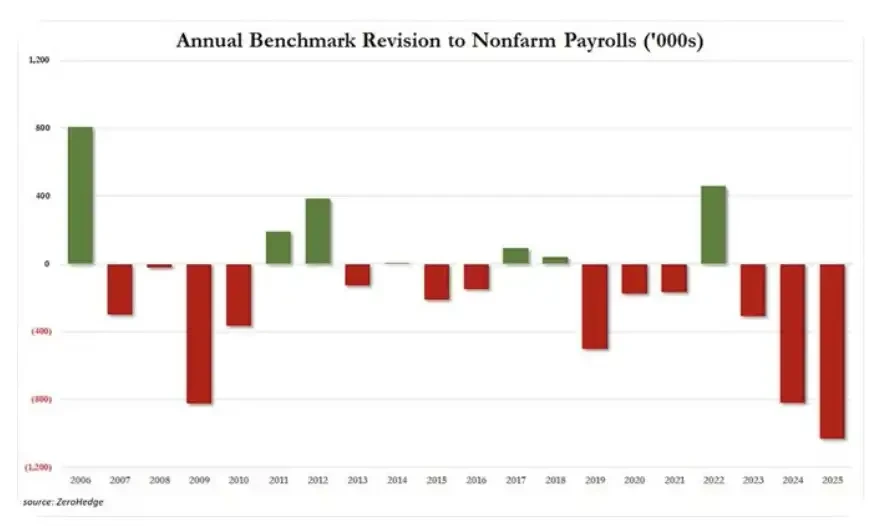

The reality is: First, U.S. 2025 employment data was revised down by a massive 1.029 million jobs, the largest annual downward revision in at least 20 years. Previously, 2024 and 2023 employment data were revised down by 818,000 and 306,000 jobs, respectively.

Cumulatively over the past three years, 2.153 million jobs have been “revised away” from the initially reported figures. Since 2019, a total of 2.5 million jobs have been revised away, and in 6 of the past 7 years, employment data has seen negative revisions.

Non-Farm Payroll Annual Revisions

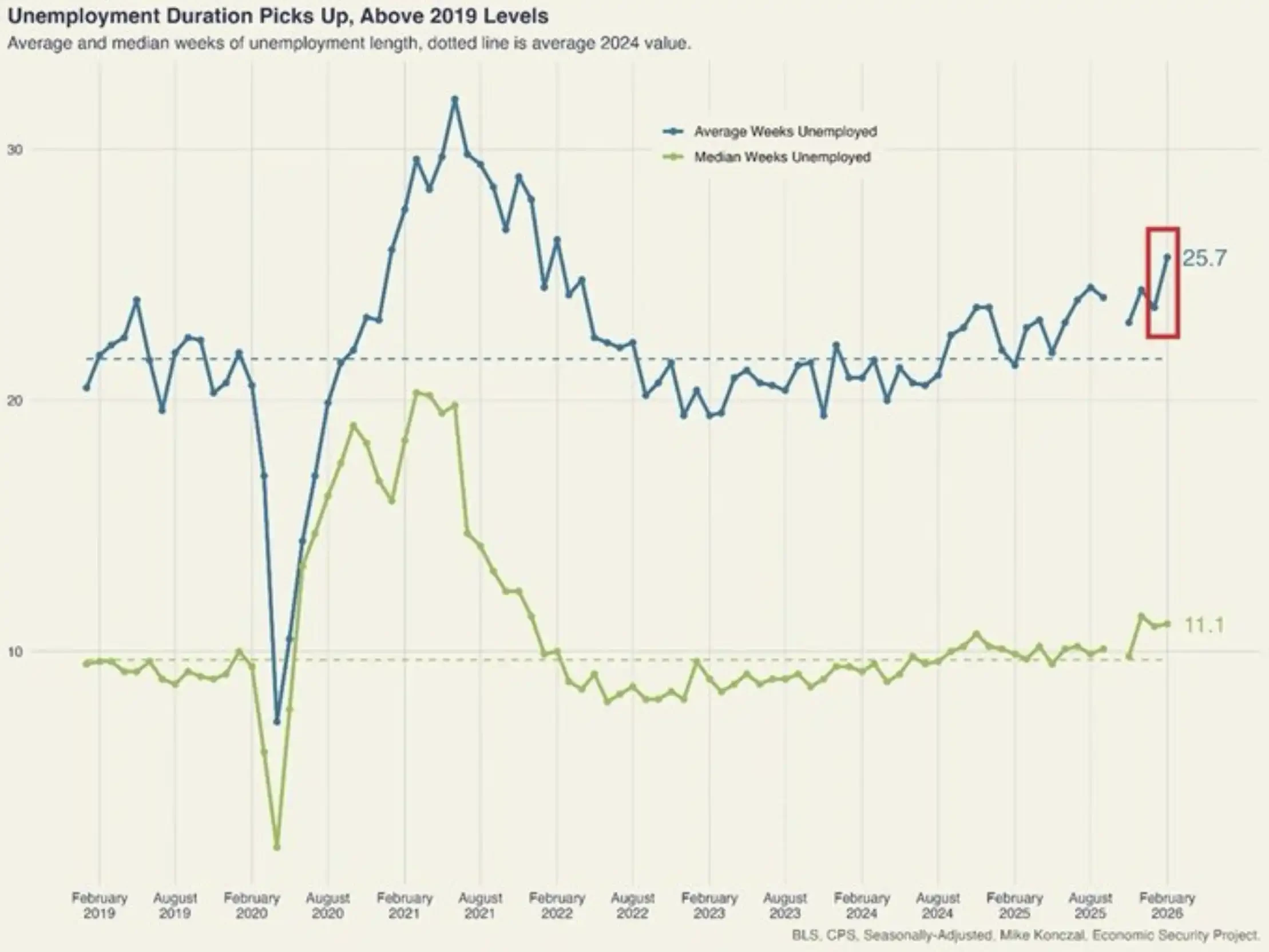

Here’s another example, and there are many similar cases. The average duration of unemployment in the U.S. rose by 2 weeks in February to 25.7 weeks, a 4-year high. Since October 2023, the unemployment duration has increased by 6.3 weeks cumulatively, the fastest pace since 2020-2021. This level is now significantly above pre-pandemic 2018-2019 levels.

U.S. Unemployment Duration Soars

Again, these signs are not isolated; we are seeing persistent and intensifying weakness in the labor market.

In our view, the U.S. economy cannot withstand the 10-year Treasury yield approaching 4.50%, let alone rising above 5.00%.

Why Is All This Happening?

From a macro perspective, the surge in U.S. Treasury yields and the reversal of rate cut expectations can be attributed to one core variable: inflation.

The Fed’s “dual mandate” was established by the U.S. Congress in 1977, requiring the central bank to achieve two primary goals through monetary policy: maximum employment and price stability. As mentioned earlier, when the Fed restarted rate cuts in 2025, the FOMC believed that, compared to still-elevated inflation, labor market weakness was the “more important” issue.

But with rising energy prices, the ongoing Iran war, and the post-war energy recovery cycle being repeatedly extended, inflation has once again become the primary contradiction—not because the labor market has improved, but because inflation itself has worsened.

U.S. 12-Month Inflation Expectations

As shown above, U.S. 12-month inflation expectations have surged to 5.2%, the highest level since March 2023. Notably, this expectation reversal began in early January and accelerated rapidly as President Trump threatened Iran, built up forces in the Middle East, and ultimately launched strikes against Iran on February 28th.

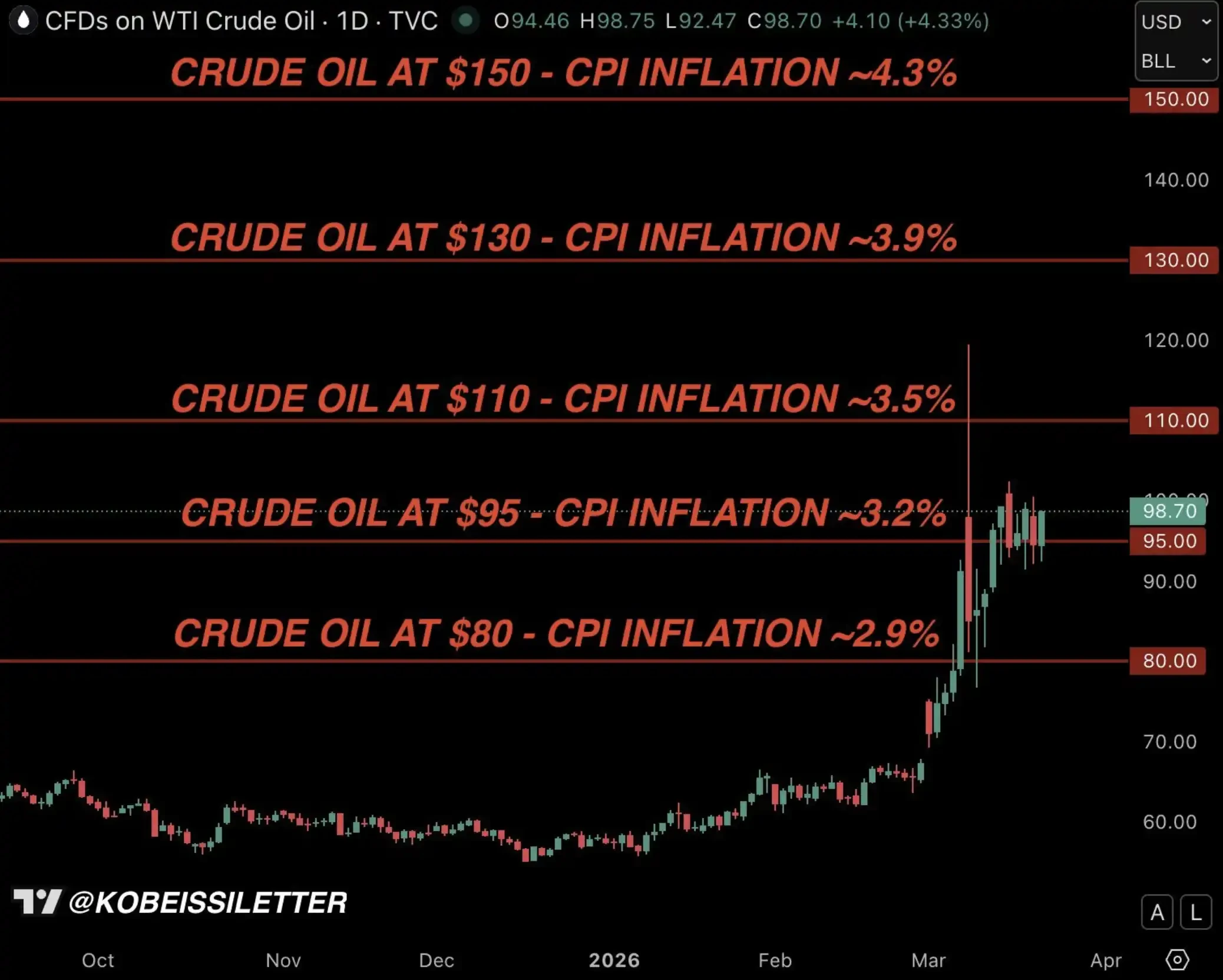

This brings us back to the model-based CPI inflation chart below. As we have repeatedly emphasized since the war began, if oil prices average $95 per barrel over three months, U.S. CPI inflation will rise to 3.2%.

Kobeissi Letter: U.S. Oil Price & Inflation Model

But the reality is, given the current series of knock-on effects, the rise in inflation is likely to be more than 3.2%.

We Believe “Intervention” Is Imminent

During the severe market volatility triggered by the trade war in early 2025, there was one key factor that ultimately prompted President Trump to announce a 90-day tariff suspension in April 2025—the bond market.

In the chart below, we outline the complete timeline of the rise in U.S. Treasury yields during the so-called “Liberation Day” period. It was this surge in yields that ultimately led to the policy shift on April 9th, alleviating market pressure.

And in a live interview on April 10th, Trump explicitly stated he was closely watching the bond market’s movements.

U.S. 10-Year Treasury Yield, April 2025

Thus, it appears the U.S. 10-year Treasury yield in the 4.50% to 4.70% range likely constitutes what we call Trump’s “Policy Shift Zone.” This level is slightly above the current position, and we largely agree: once yields reach this zone, policy intervention will become necessary to prevent a severe downturn in the U.S. economy.

U.S. 10-Year Treasury Yield, Trump’s “Policy Shift Zone”

In our view, this time will be no exception. In fact, we believe the timing of President Trump’s announcement of “peace talks” on March 23rd was no coincidence, as shown below.

March 23rd, The First Signal of Intervention

At 4:30 AM ET on March 23rd, we noted: compared to the energy market, the bond market’s problems had become more “disorderly.” Then, just 2 hours later, with the 10-year yield at 4.45%, President Trump likely engaged in decision-making discussions similar to those on April 9, 2025—when he announced the 90-day tariff suspension.

Another hour later, Trump announced a 5-day delay in strikes on Iranian power facilities and stated that “productive” talks were underway between the U.S. and Iran aimed at ending the war.

This may have been the first signal that intervention had begun.

What Should You Do Now?

The question we receive most often is: what does this mean?

From a macro perspective, we want to emphasize one point: the Trump administration is highly sensitive to volatility in stock, commodity, and bond markets. This is good news for investors—Trump does not want markets to fall, and his focus on this is noticeably higher than previous administrations.

This is also why oil prices, after their initial spike, have remained somewhat contained overall. Crude investors broadly believe that if oil again approaches $120 per barrel (as seen early in the war), Trump would quickly intervene.

More broadly, we believe that as the 10-year yield rises, downward pressure on stocks will intensify; but when yields approach what we call the 4.50% to 4.70% zone, the impending policy shift or “intervention” will limit the downside for stocks.

Furthermore, Trump, the Fed, and the entire administration understand that the U.S. labor market cannot withstand higher rates for long, which also means the current situation is unlikely to evolve into a “long war” and is more likely to see some form of de-escalation or resolution within weeks, not months.

Finally, behind all this volatility and noise, we want to emphasize: the AI revolution is only accelerating. Those AI companies that have led the market since 2022 and are now under pressure from the pullback are actually investing more and building faster.

Our view on stocks and the long-term AI trend remains unchanged.

Keep Watching the Bond بازار

What we are experiencing is not just volatility, but a shift in the “decisive variable.”

Over the past few weeks, market attention has focused on oil prices, war news, and geopolitical escalation. But beneath the surface, a more powerful force has been building and is beginning to dominate the situation.

The bond market is once again determining the direction of stocks, commodities, and even policy itself. And history has repeatedly shown that when financial conditions tighten too quickly, the question of intervention is never “if,” but “when.”

As we have emphasized all year, this market is increasingly like a game of “pattern recognition,” where the key is to act one step ahead of the “crowd.”

We believe the bond market will become the next most important narrative.

یہ مضمون انٹرنیٹ سے لیا گیا ہے: Stop Focusing Solely on Oil Prices; the Bond Market is the Real Bellwether

Related: How did the earliest regulators studying Bitcoin gradually step into the crypto world?

Author | Ding Dang (@XiaMiPP) In the eyes of most, there seems to be an unbridgeable chasm between the cryptocurrency industry and the US regulatory system. On one side are the boundary-pushing tech pioneers who believe code can rewrite financial rules, constantly testing the limits of the system. On the other side are the regulators, guardians of order and stability, wielding caution and rules as their shield to protect the bottom line of the financial system. Over the past decade, these two forces have clashed fiercely at times and reached brief compromises at others, always moving forward in a delicate state of tension. But some individuals stand precisely on this boundary line, such as Mark Wetjen. He spent nearly two decades working within the US financial regulatory system: from a…