In-Depth Analysis of STRC: MicroStrategy’s New Magic Trick for Raising Funds to Buy Bitcoin

Compiled by | Odaily (@OdailyChina); Translator | Azuma (@azuma_eth)

Over the past two weeks, we’ve seen a significant increase in STRC trading volume, alongside growing buzz about the product on social media platforms like X. Therefore, I believe now is a good time to write an article about Strategy and its new structure. This is my fourth article on Strategy and the Bitcoin treasury model:

- The first article introduced the Strategy playbook, where I clarified some common misconceptions about the model.

- The second article explained the “full-stack treasury company” model and the mechanisms supporting its NAV premium.

- The third article introduced the preferred share playbook, a new model launched by Strategy in 2025, which is now the company’s primary strategy.

In this article, we will focus on STRC. It has now become MSTR’s most significant preferred share product and the central focus for Michael Saylor (founder of Strategy) and his management team.

TL؛ DR

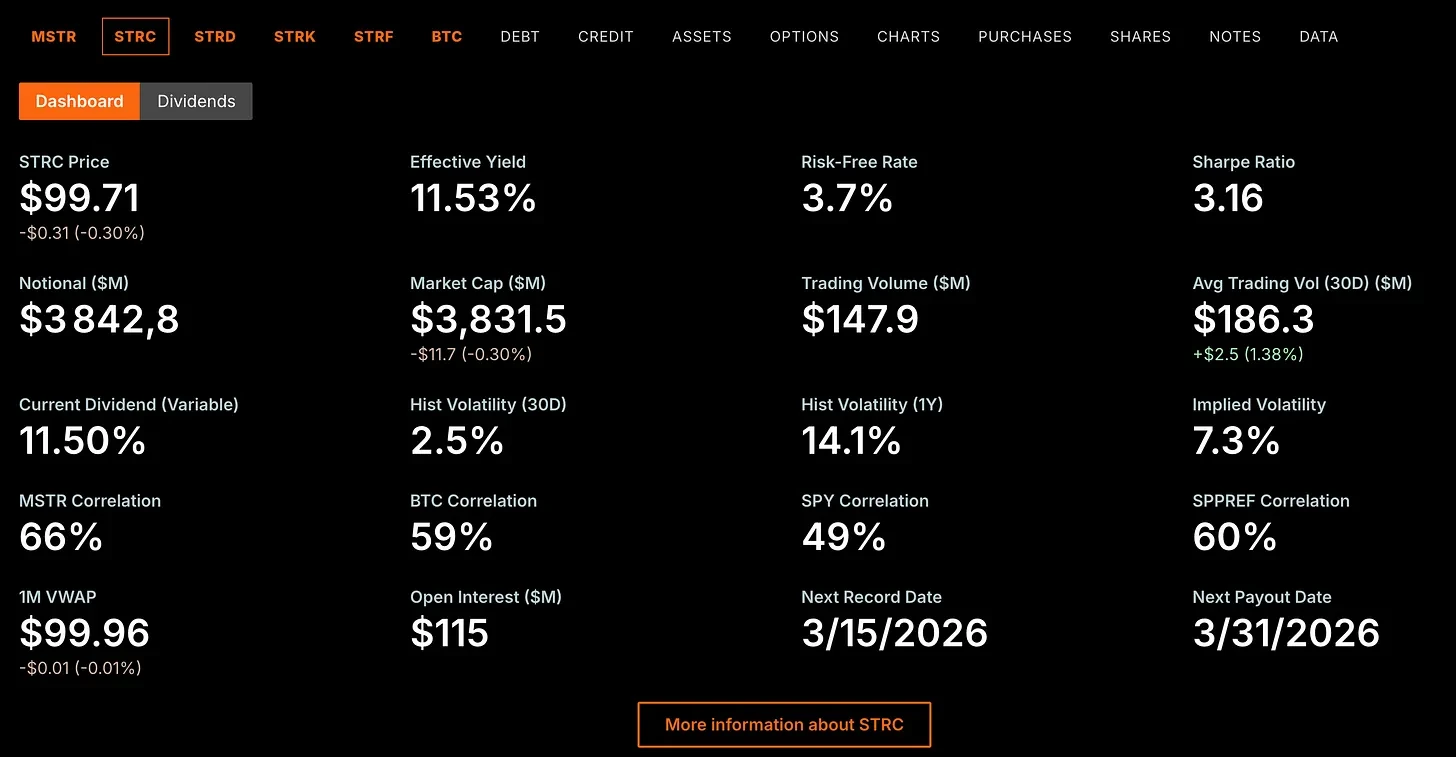

- STRC is an income-generating instrument backed by Strategy’s Bitcoin treasury. Its dividend rate adjusts dynamically to maintain a price close to par value ($100). Currently, you can earn an 11.5% annualized yield (paid monthly) on a relatively stable and transparent-risk instrument.

- STRC is essentially a way for Strategy to convert yield demand into structural buying pressure for BTC. As long as Strategy runs both the STRC and MSTR ATM issuance mechanisms (and mNAV > 1), this structure can scale massively without increasing MSTR’s leverage. This means Strategy can absorb tens or even hundreds of billions of dollars in new demand for STRC while keeping the leverage ratio around 33% and credit risk unchanged.

- By using the common stock ATM to maintain leverage, roughly $3 of BTC is added to the treasury for every $1 of STRC issued. Based on rough estimates, when STRC trades near par ($100) with a daily volume of $100 million, it could translate to $100-$150 million in BTC purchases.

- Strategy effectively splits BTC exposure into two different risk tranches: STRC holders get relatively stable, low-volatility income, while MSTR shareholders take on the remaining upside and volatility of BTC. As Lavoisier said: “Nothing is created, nothing is lost, everything is transformed.”

- The design goal of the entire structure is to increase the بٹ کوائن-per-share ratio over time. This ultimately benefits MSTR common shareholders, as it means MSTR should mechanically outperform BTC.

- Short-term pullbacks of 5%–10% in STRC are possible, but as long as market confidence in the structure remains, arbitrage trading will typically pull the price back towards par.

- The real risk is not a sudden collapse, but a prolonged BTC bear market, which could gradually stress the entire structure over time. Even in the (extremely unlikely) worst-case scenario, the process would be very slow due to dollar reserves and Strategy’s flexibility in adjusting dividend rates.

- If Strategy ultimately fails, it likely won’t be a dramatic, sudden event like Luna/UST, but rather a slow, long-term deterioration.

- It’s logically difficult to be bullish on BTC while bearish on MSTR and STRC. At Strategy’s current risk level (which may change), it’s nearly impossible for Strategy to fail before BTC does.

What is STRC and How Does It Work?

First, let me briefly review the concept of preferred shares: simply put, they are debt-like financial instruments but legally still equity in the company. This means these preferred shares never need to be “repaid,” and Strategy cannot default on them.

In the capital structure, preferred shares rank above common stock (MSTR) for claims, meaning in a bankruptcy scenario, preferred shareholders get paid before common shareholders.

So far, Strategy has issued five preferred shares (STRF, STRC, STRK, STRE, STRD), which I detailed in my previous article. Here are the key features of STRC (also known as Stretch):

- It falls into the “short-duration high-yield credit” category.

- Strategy aims to keep STRC’s price as close to $100 (par value) as possible, ideally within a 1% range of $99–$100.

- STRC pays floating dividends monthly; the current dividend rate is 11.5%.

- If STRC trades significantly below par, Strategy can increase the monthly dividend rate, making the product more attractive and boosting demand until the price returns near par.

- If STRC’s price rises above $100, Saylor can issue and sell new STRC shares at $100 via the ATM (at-the-market) program. This effectively creates a price ceiling around $100.

- If Saylor doesn’t want to issue shares via ATM, the company has another option—redeem STRC at $101, meaning market participants have little incentive to buy STRC above that price.

- Like Strategy’s other preferred shares, STRC is a perpetual preferred stock, meaning it has no maturity date and no repayment deadline.

Odaily Note: All STRC data can be found on Strategy.com. The screenshot below is from March 13, 2026, which was an ex-dividend date, hence STRC’s price is below par.

How Does Strategy Use ATM to Control Leverage?

Although Strategy’s preferred shares are not legally debt, they can be seen as a way to introduce leverage to the balance sheet. Strategy distinguishes between the leverage ratio (convertible notes / BTC reserves) and the amplification ratio (convertible notes + preferred shares / BTC reserves).

درحقیقت، the amplification ratio is the true measure of Strategy’s leverage level. This means that whenever Saylor issues and sells new STRC, Strategy’s leverage increases. If Saylor wants to reduce the company’s leverage, the tool he can use is the common stock ATM issuance—issuing new MSTR shares and using the proceeds to buy BTC, expanding the company’s size while lowering the leverage ratio.

The logic is straightforward: Suppose a company holds $10 billion in BTC, has $3 billion in debt, and a market cap of $12 billion. Its leverage ratio is: $3B debt / $10B BTC = 30%.

Assume the company issues an additional $2 billion in new shares and uses the funds to buy $2 billion in BTC. With BTC price unchanged, the market cap becomes $14 billion, the BTC treasury becomes $12 billion, but the nominal debt amount hasn’t changed. The new leverage ratio is: $3B debt / $12B BTC = 25%.

From this example, it’s clear that through common stock ATM issuance, the company can both scale up (market cap from $12B → $14B) and reduce leverage (30% → 25%).

Is Strategy Aggressively Buying BTC with STRC?

How STRC Demand Translates into BTC Buying Pressure

As I mentioned earlier, Saylor only sells STRC at $100, not below.

This means that when the price is below $100, all trading volume is just existing STRC shares changing hands between past, present, and new holders. When the price reaches $100, some volume still corresponds to regular STRC share trading (as some are willing to sell at $100), but the remaining volume corresponds to Saylor issuing new shares and selling them at $100 to meet “excess demand.”

Last week, the ratio of STRC’s weekly trading volume to the weekly ATM issuance size was about 40%. I’ll use this number in the example below, but it’s obviously not a fixed rule; it could be 25% or 60% in some cases.

When STRC trades near par with a daily volume of $100 million, the situation is roughly this: Saylor can issue 40% of that amount via the STRC ATM program, i.e., issue and sell $40 million in brand-new STRC shares. He then immediately uses that $40 million to buy BTC.

Odaily Note: The ATM activates and runs when STRC’s price reaches $100.

However, selling STRC increases the company’s leverage (as it’s a debt-like instrument), and Saylor certainly wants to keep leverage stable. Strategy’s current leverage is around 33%, and I believe he wants to keep it around that level. This means for every $1 of new “debt,” $3 of BTC reserves must be added. In the previous example, if Saylor adds $40 million in “debt” via STRC and buys $40 million in BTC, he still needs to add another $80 million in BTC to the company’s reserves. How does he do that?

The answer was explained in the previous section—using the common stock MSTR ATM mechanism. Therefore, Saylor would issue and sell $80 million in new MSTR shares and immediately use the proceeds to buy $80 million in BTC.

So the conclusion is, based on this rough calculation, $100 million in daily STRC volume corresponds to about $40 million in new STRC issuance and approximately $120 million in BTC purchases. Through STRC, Strategy has found a way to convert demand for stable yield into BTC buying power.

What if STRC Demand Explodes? Would Saylor Be Forced to Max Out Leverage?

I also want you to notice another point: according to the model I just described, Strategy could theoretically triple the market cap of STRC (i.e., add about $8 billion more in STRC “debt” on top of the current $4 billion market cap) without increasing the company’s leverage ratio (i.e., credit risk).

Saylor already has all the necessary tools to scale STRC to meet any level of market demand while still keeping leverage stable at 33%.

Obviously, this increases the nominal size of the company’s “debt” and the dividend payments required, but these metrics grow in sync with the BTC treasury size, meaning Strategy doesn’t take on any additional BTC price-related risk.

What Are the Real Limits of This Strategy?

The model I described above, running both STRC and MSTR ATM mechanisms simultaneously, requires two conditions.

The first condition is obvious: STRC must be trading at $100. When this happens, it essentially means demand for STRC exceeds its current market cap, so Saylor issues new shares to meet the excess demand.

The second condition, which I haven’t mentioned before, is that mNAV must be above 1x to use the common stock ATM mechanism. As I explained in detail in another article, Strategy’s core goal is always to increase the bitcoin-per-share (bps) ratio over the long term. When they sell MSTR shares and buy BTC while mNAV is above 1x, it is accretive from a bps perspective; the higher the mNAV, the more accretive the operation; when mNAV is exactly 1x, it’s neutral; but when mNAV is below 1x, using proceeds from MSTR sales to buy BTC is dilutive from a bps perspective, so they avoid it.

You may have noticed that in the previous section, I mentioned: using the MSTR ATM can both scale the company and reduce leverage. But if mNAV is above 1x, then using the common stock ATM has an additional benefit—improving the bps ratio.

By the way, the mNAV metric is actually displayed directly on the homepage of Strategy.com. They use the most diluted mNAV as a reference, which is the correct approach. Currently, it’s around 1.2x, and I believe the lowest it has been in 2026 is around 1x.

So, what if a situation arises where, due to excessive STRC demand, Saylor has to issue new STRC shares, but mNAV is below 1x? Would that mean he can’t use the MSTR ATM to maintain stable leverage, forcing him to increase leverage?

First, I think this scenario is unlikely because STRC trading stably at $100 itself implies investor confidence in the overall structure, so MSTR’s mNAV should theoretically be at least above 1x. Second, this assumption ignores another tool they have to control STRC demand—lowering the dividend.

The Dividend Rate Question: Can 11.5% Be Sustained?

First, let me remind you that STRC launched with a 9% dividend rate. The dividend rate is a tool that can be adjusted to match STRC demand and ensure its price stays near par.

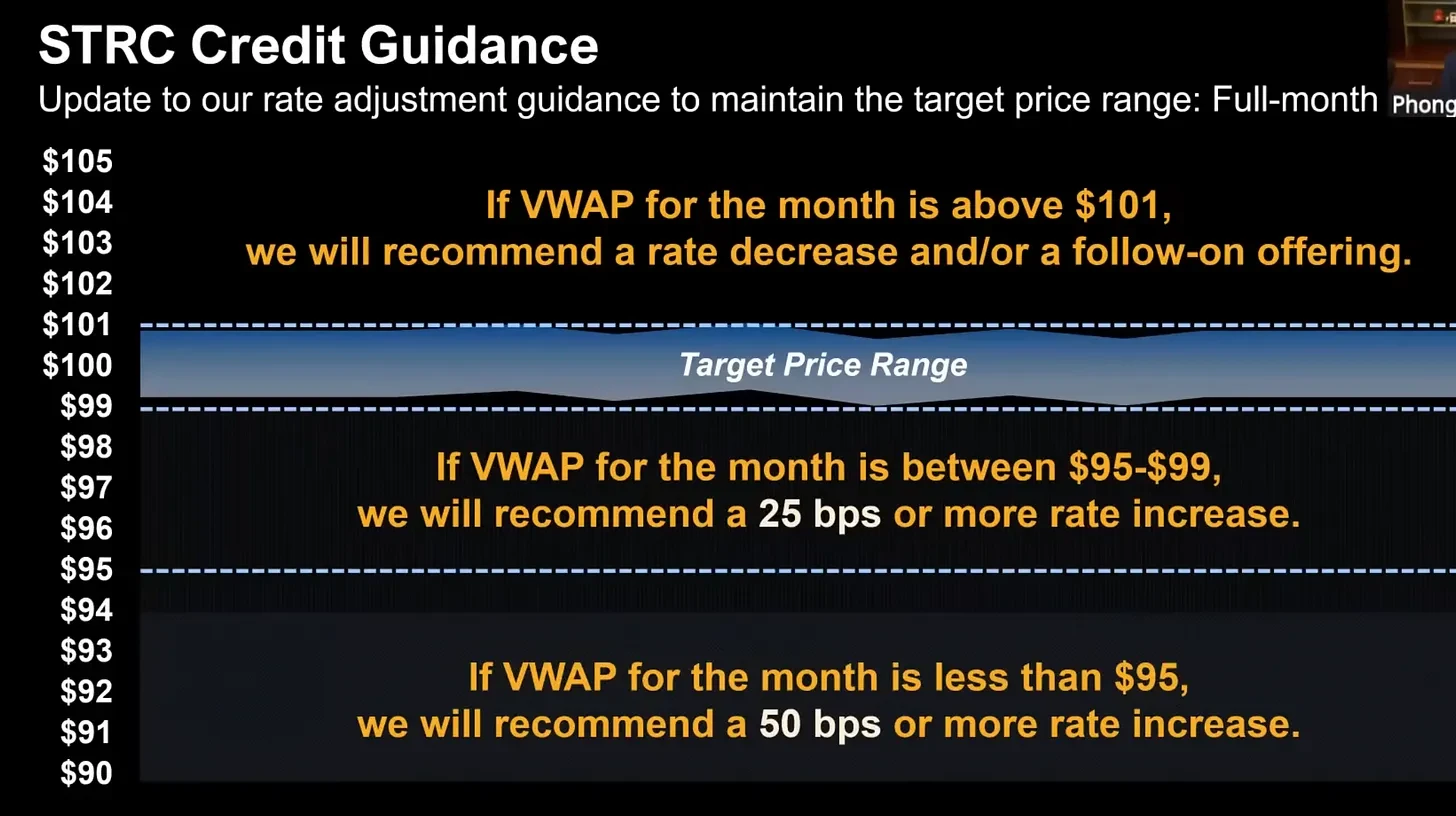

Strategy’s current guidance is: if STRC’s monthly VWAP (Volume Weighted Average Price) is between $95–$99, they will increase the dividend rate by 25 basis points (bps); if the monthly VWAP is below $95, they will increase it by 50 bps; if the monthly VWAP is above $101, they will decrease the dividend rate.

So, what they’ve done so far is essentially gradually raise STRC’s dividend rate from 9% to 11.5% to reach an equilibrium where STRC trades around $100 in daily trading. This week has been STRC’s most successful week so far, as it not only traded consistently near par but also with massive volume (around $300–400 million daily, compared to an average previously just over $100 million).

Odaily Note: Chart of STRC’s performance since launch.

STRC demand fundamentally depends on several variables:

- Credit risk: What is Strategy’s current leverage ratio? In other words, how much BTC is currently “backing” STRC? This directly depends on BTC’s price—if BTC falls, all else equal, leverage increases, credit risk rises, and STRC demand falls (i.e., STRC price drops).

- Yield: What dividend rate is STRC currently paying? The higher the dividend rate, the greater the demand for STRC.

- Awareness: How many people know about STRC? In the initial months or years after a product launch, this is a very important factor, as it’s essentially a variable that only goes up, significantly affecting STRC demand, all else equal.

- Confidence: How many people, after seeing STRC trade for months and consistently pay dividends, are willing to put money into it? This is a special factor because confidence can swing widely—if STRC trades in a narrow range near $100 for a long time, more people will consider it safe; but if we suddenly see a 10% drop in a day, that trust can evaporate quickly.

From STRC’s launch until now, we’ve seen: credit risk increased (as BTC fell 45% from its ATH), yield increased, awareness increased, and confidence increased. One factor negatively impacted demand, while three positively impacted it. We are now finally in an “ideal” state: STRC is stable around $100.

When BTC price was around $68k, an 11.5% yield was the dividend level needed to pull STRC’s price back to par. For a product that has traded for less than eight months, this seems quite positive to me. Saylor expects BTC’s compound annual growth rate (CAGR) over the next 20 years to be 20–30%. As I explained in detail in another article, under this assumption, it’s perfectly reasonable to issue “debt” at 11.5% to buy an asset expected to grow 25% annually. The

یہ مضمون انٹرنیٹ سے لیا گیا ہے: In-Depth Analysis of STRC: MicroStrategy’s New Magic Trick for Raising Funds to Buy Bitcoin

Related: ERC-5564: Ethereum’s Stealth Era Has Arrived, Receiving Addresses No Longer ‘Exposed’

Original compilation: Luffy, Foresight News Have you ever opened Etherscan to search for your own wallet address, not to check a transaction, but just to see what it looks like to an outsider? Your current balance, every token you’ve ever held, NFTs you’ve bought, protocols you’ve interacted with, those late-night DeFi attempts, every airdrop you’ve claimed or ignored… everything is there, completely public. Imagine sending this address to a freelancer who’s supposed to pay you, a DAO giving you a grant, or even just someone you met at a conference. You’re not just handing over a receiving address, but an entire, complete on-chain financial life. The reason is simple: Ethereum, like most public chains, treats every address as essentially a public ledger. Most people have felt this awkwardness. You hesitate…