First-day trading volume crushes Polymarket as Hyperliquid enters the prediction market with BTC binary options

Author: Asher (@Asher_0210)

On May 2nd, Hyperliquid launched HIP-4 Outcome Pasars on mainnet, officially introducing outcome markets to its on-chain trading system. The first batch listed are BTC intraday binary outcome contracts, allowing users to trade on whether the BTC price will be above or below a specified price at a certain point in time. Contract prices float between 0.001 and 0.999, reflecting the market’s pricing of the event’s probability; they settle at 1 if the event occurs and 0 if it doesn’t. Contracts are fully collateralized in USDH, with no fees for opening positions.

This is not a simple product expansion. In the past, Polymarket functioned more like an information market centered around events, where users entered a specific market due to elections, sports, geopolitical conflicts, or kripto trends, expressing their judgment on outcomes through prices. Kalshi, on the other hand, attempts to place event contracts within a clearer regulatory framework.

Hyperliquid’s entry point is different. It doesn’t first build a standalone prediction market to attract users to migrate funds, but instead starts directly from its most familiar trading environment—integrating outcome contracts alongside perpetuals and spot trading. For Hyperliquid, prediction markets are not just about betting on outcomes, but a new tool for traders to express direction, manage risk, and build strategies.

BTC Intraday Market Off to a Strong Start, First-Day Data Exceeds Expectations

The first market under HIP-4 is a daily settlement BTC price performance market. This choice is very “Hyperliquid”—starting not from politics, sports, or entertainment, but from the BTC price volatility that crypto traders are most familiar with.

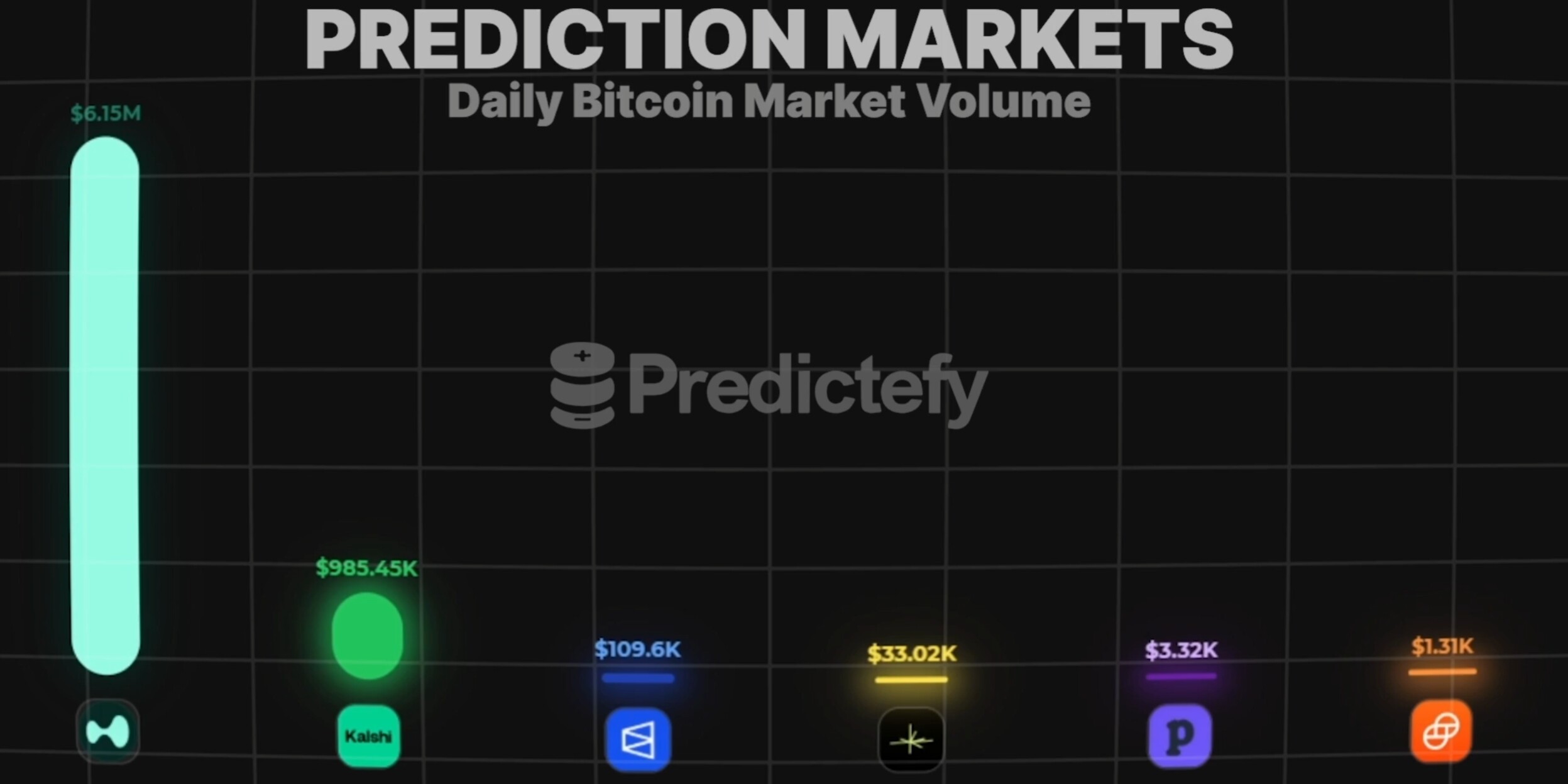

On its first day, HIP-4 delivered impressive data. According to Predictefy, on the launch day of Hyperliquid’s event contracts, the trading volume for its BTC price-related event contracts reached $6.15 million, far exceeding similar markets on Kalshi, Polymarket, and other prediction platforms. That is, in the niche market of BTC price-related event contracts alone, Hyperliquid ranked at the very top on day one.

Data Source: Predictefy

Furthermore, on its first day, HIP-4 generated over $12,000 in total trading fees, with over 54,000 trades executed by more than 3,000 unique traders. For a newly launched HIP-4 focused on prediction market-related events, these figures are already quite impressive. It didn’t achieve this by flooding the market with numerous event categories, but by achieving a cold start within the single BTC intraday market. This makes HIP-4’s initial step even more significant.

Why HIP-4 Isn’t Simply a Modification of HIP-3

Hyperliquid previously supported Builder deployment of perpetual contract markets through HIP-3. The question arises: since perpetual markets are deployable, why design HIP-4 separately? The answer lies in the fundamentally different settlement logic of outcome contracts.

Perpetual contracts require continuous pricing, allowing the oracle price to adjust gradually. However, binary outcome contracts can only settle at 0 or 1. If an oracle mechanism unsuitable for binary contracts is used, it could leave a prolonged window for mispricing even after the event outcome is certain, creating nearly risk-free arbitrage opportunities.

Therefore, HIP-4 is designed as a standalone outcome market primitive. It’s not a reskinned perpetual, but a contract type specifically designed for maturity, settlement, dispute resolution, and Oracle result confirmation. For the average user, prediction markets seem like simply buying Yes or No. But for a real trading system, the true difficulty lies in how events are defined, who confirms them, when they settle, how disputes are handled, and how erroneous results are corrected and penalized. The core of a prediction market isn’t just the front-end page and trading entry point; it’s the settlement mechanism itself.

Hyperliquid, Polymarket, and Kalshi: Different Battlefields

Comparing Hyperliquid’s HIP-4, Polymarket, and Kalshi reveals three distinct directions for prediction markets:

- Polymarket’s core advantage is event richness and user mindshare: Its greatest strength lies in transforming complex events into tradable questions, combining public attention, media dissemination, and market probabilities. Political elections, geopolitical conflicts, celebrity events, sports tournaments, and crypto project milestones can all be quickly turned into markets.

- Kalshi’s advantage lies in its compliance pathway: It operates closer to an event contract platform within the traditional finance context, with target users and regulatory frameworks not entirely identical to Polymarket or Hyperliquid. The recent intensifying debate over prediction market regulatory authority in the US, and the conflict between the CFTC and state-level regulators, indicates event contracts are no longer a fringe product but have entered the core discussion zone of financial regulation.

- Hyperliquid’s edge is its trading experience and capital efficiency: Hyperliquid boasts its own L1, HyperCore matching engine, on-chain order book, and spot and perpetual infrastructure. Official documentation shows HyperCore includes fully on-chain perpetual and spot order books, where orders, cancellations, trades, and liquidations are executed transparently, capable of handling 200k orders/second.

Thus, Hyperliquid may not necessarily take all of Polymarket’s users in the short term. A lightweight user interested in the US election, sports events, or entertainment gossip might not enter Hyperliquid’s trading interface just to buy an event contract. However, a trader already using Hyperliquid for BTC, ETH, Gold, Oil, or equity perpetuals might naturally incorporate BTC intraday outcome contracts as part of their portfolio.

HYPE: The Potential Value Capture Hub in This Competition

The significance of HIP-4 for Hyperliquid goes beyond adding a new trading scenario; it further integrates prediction markets with HYPE’s staking, fee, and buyback mechanisms. According to HIP-4’s design, Phase 1 involves validators deploying standardized markets, while Phase 2 will open up permissionless deployment. Future market creators wishing to launch their own prediction markets will need to stake 1 million HYPE. Each staking slot can support rolling and periodic markets, reusable after settlement. In cases of oracle manipulation, abnormal market states, or prolonged downtime, the staked assets can be slashed.

This threshold is significantly higher than HIP-3’s 500,000 HYPE. The reason is understandable: outcome markets depend more heavily on event definitions and Oracle settlement than perpetual markets. Perpetual prices adjust continuously, but outcome markets ultimately result in 0 or 1. A settlement error doesn’t just harm the trading experience of one market; it erodes the credibility of the entire prediction market system.

For HYPE, HIP-4 introduces two layers of incremental demand. First, staking demand. More Builders wanting to deploy outcome markets will need to lock up more HYPE. Especially as categories like sports, macroeconomics, politics, crypto events, and entertainment gradually open up, the right to create quality markets may become a high-barrier operational license. Second, fees and buyback logic. Hyperliquid already has strong transaction volume and fee capture capabilities, with a significant portion of protocol fees used to buy back HYPE. If HIP-4 generates new trading volume, outcome markets will not just be an added feature but become part of the growth flywheel for fees and HYPE buybacks.

This is also a key differentiator between Hyperliquid and Polymarket or Kalshi. The growth of Polymarket and Kalshi is primarily reflected in platform trading volume, market share, and brand influence. In contrast, Hyperliquid’s growth translates more directly into demand for and value capture by HYPE.

Market is Optimistic, but HIP-4 Still Needs to Prove Itself

Market feedback on HIP-4 leans optimistic, and the reason is straightforward. Hyperliquid already possesses mature trading infrastructure, active trading users, and a clear HYPE value capture mechanism. Entering the prediction market doesn’t require rebuilding a matching system or finding its first batch of traders from scratch.

However, HIP-4 is still in a very early stage. Currently, the market is concentrated on BTC price outcomes. Whether it can expand to sports, politics, macroeconomics, crypto events, and entertainment will depend on the successful rollout of permissionless deployment in Phase 2. Furthermore, outcome markets have higher requirements for oracles and settlement mechanisms. Event definitions, data source selection, dispute resolution, and erroneous settlements will all directly impact market trust.

So, the significance of HIP-4 isn’t that Hyperliquid has already won the prediction market race, but that it offers a new competitive direction for this track. Polymarket proved events can form information markets; Kalshi represents the path of compliant event contracts; Hyperliquid aims to prove that event contracts can also be part of an on-chain trading system.

If past prediction market competition was about who could capture more hot topics and attract more bettors, then after HIP-4, a new line of competition emerges: who can truly integrate event outcomes into traders’ capital, positions, and strategies.

This also means Polymarket’s rival is no longer just Kalshi. With Hyperliquid’s entry, the next phase of prediction markets may not just be a competition between event markets, but a competition between trading systems, liquidity, and asset pricing capabilities.

Artikel ini bersumber dari internet: First-day trading volume crushes Polymarket as Hyperliquid enters the prediction market with BTC binary options

According to the indictment unsealed by the DOJ on the same day, Van Dyke was involved in an operation on January 3 of this year to capture Venezuelan President Nicolás Maduro from the presidential palace in Caracas. Reports indicate that Van Dyke wagered on prediction markets just before the operation that Maduro would be captured, earning over $400,000. Although the reports did not disclose specific account details, based on the betting direction and profit amount mentioned, we were able to identify the account 0x31a5. This is precisely one of the five insider accounts highlighted by PolyBeats in two consecutive reports on January 4 and January 7. Reviewing Van Dyke’s Account Activity Let’s rewind the timeline to January 4 of this year. Following Maduro’s capture, PolyBeats meticulously parsed the on-chain data,…