The market isn’t buying Meta’s AI narrative: Behind the low valuation lie three unresolved challenges

長話短說

- Bank of America raised its capital expenditure forecasts for Alphabet, Meta, and AWS, projecting a combined capacity of up to 57GW by 2027.

- A model breakdown shows Meta’s implied value per GW of 人工智慧 capacity is approximately $4 billion, significantly lower than the two major cloud providers.

- Meta appears cheapest, but enterprise AI sales, power access, and customer payment remain unproven.

The key takeaway from this report is not who is spending the most, but that with the same AI data center expansion, the market assigns vastly different prices to the capacity of different companies. AWS and Google Cloud already have mature cloud businesses that can sell computing power to enterprise clients. Meta relies more on its advertising business, AI recommendation efficiency, and its still-early enterprise AI products, resulting in a lower value for its data centers reflected in the stock price.

For investors, AI capital expenditure must ultimately answer a practical question: can electricity, GPUs, and data center capacity be converted into cloud revenue, enterprise AI service revenue, or higher advertising efficiency? Meta’s discount precisely indicates that this question has not yet been fully bought into by the market.

Big Three Capacity to Reach 57GW by 2027, Capex Still Rising

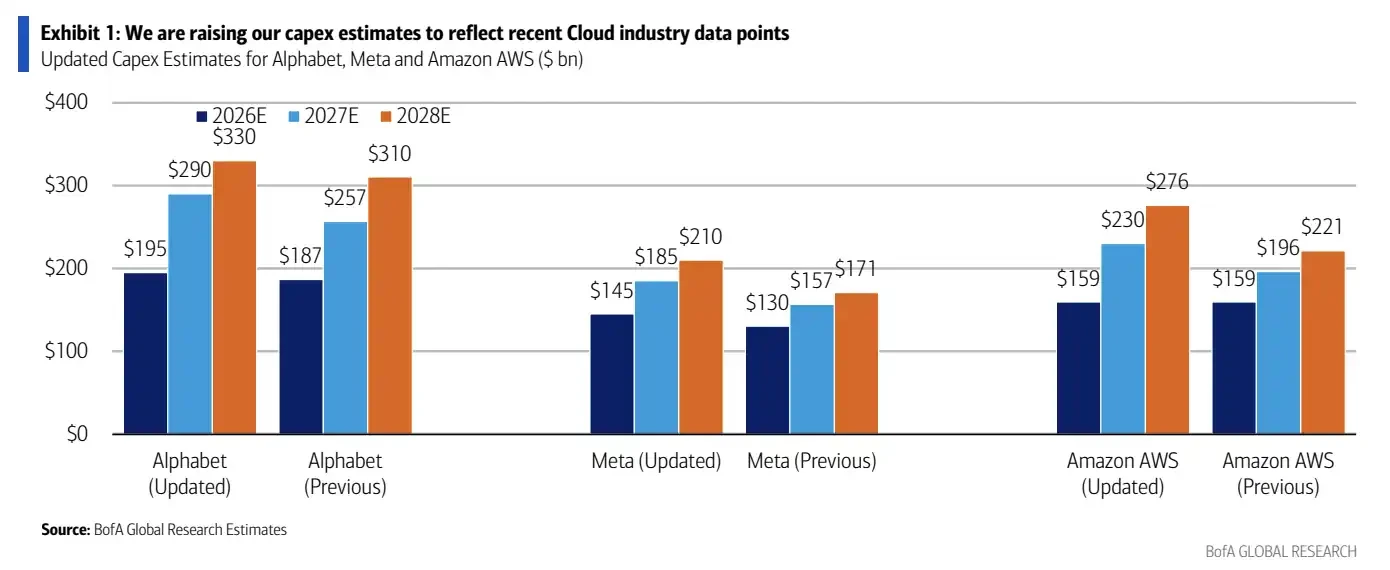

According to Bank of America’s forecasts, the overall capital expenditure expectations for Alphabet, Meta, and AWS for 2026 to 2027 have been revised upwards. Specifically, Alphabet’s 2026 capex forecast was raised from $187 billion to $195 billion, and its 2027 forecast from $257 billion to $290 billion. Meta’s 2026 forecast was raised from $130 billion to $145 billion, and its 2027 forecast from $157 billion to $185 billion. AWS’s 2026 forecast remained at $159 billion, while its 2027 forecast was raised from $196 billion to $230 billion.

These figures are closer to Bank of America’s model projections and do not all equate to the companies’ official guidance. Publicly, Meta had previously raised its 2026 capex guidance to between $125 billion and $145 billion, while Alphabet’s public guidance is approximately $180 billion to $190 billion.

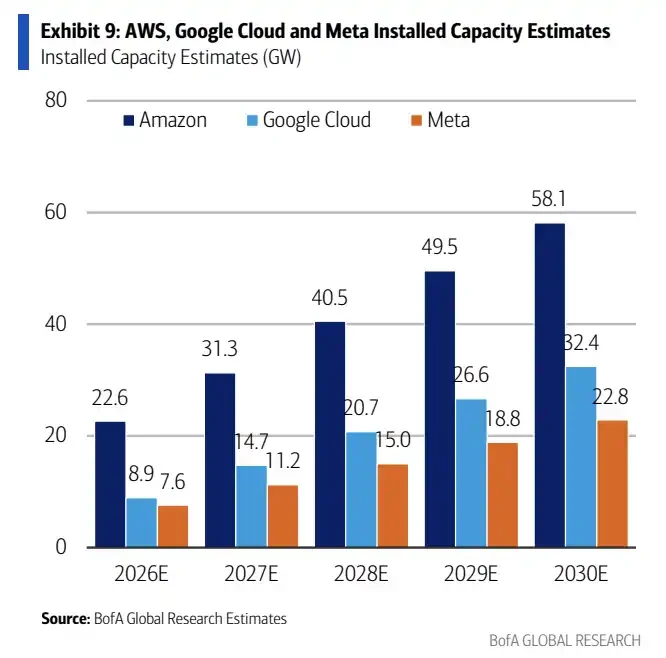

Corresponding to data center capacity, Bank of America estimates the combined capacity of the three companies will be approximately 27GW by the end of 2025, rising to 39GW in 2026, and further to 57GW in 2027. In other words, an additional ~30GW of capacity is expected over two years.

The largest increase comes from Amazon. From 2026 to 2027, AWS is expected to add approximately 15GW, Google about 9GW, and Meta about 6GW. AWS has a larger existing cloud infrastructure base, with enterprise demand, internal e-commerce, and AI services absorbing the capacity, hence its largest expansion scale.

Comparison of old and new 2026-2028 capital expenditure forecasts for Alphabet, Meta, and AWS, showing the most significant upward revision for 2027.

The cost of building the same 1GW capacity also varies. According to Bank of America’s estimates, for each additional GW of capacity added in 2026, the cost is about $25 billion for Amazon, $37 billion for Google, and $45 billion for Meta. Amazon’s cost is lowest, mainly due to economies of scale and proprietary chips. Meta’s cost is highest, more affected by upfront civil engineering investments and reliance on external GPUs.

This places Meta in a more awkward position: its added capacity is not the largest, but its per-GW construction cost is higher. If it cannot successfully generate enterprise revenue in the future, or clearly reflect it in advertising efficiency, the market will find it harder to assign a higher valuation to this part of its assets prematurely.

Valuation Gap Widens: Meta Worth Only $4 Billion per GW

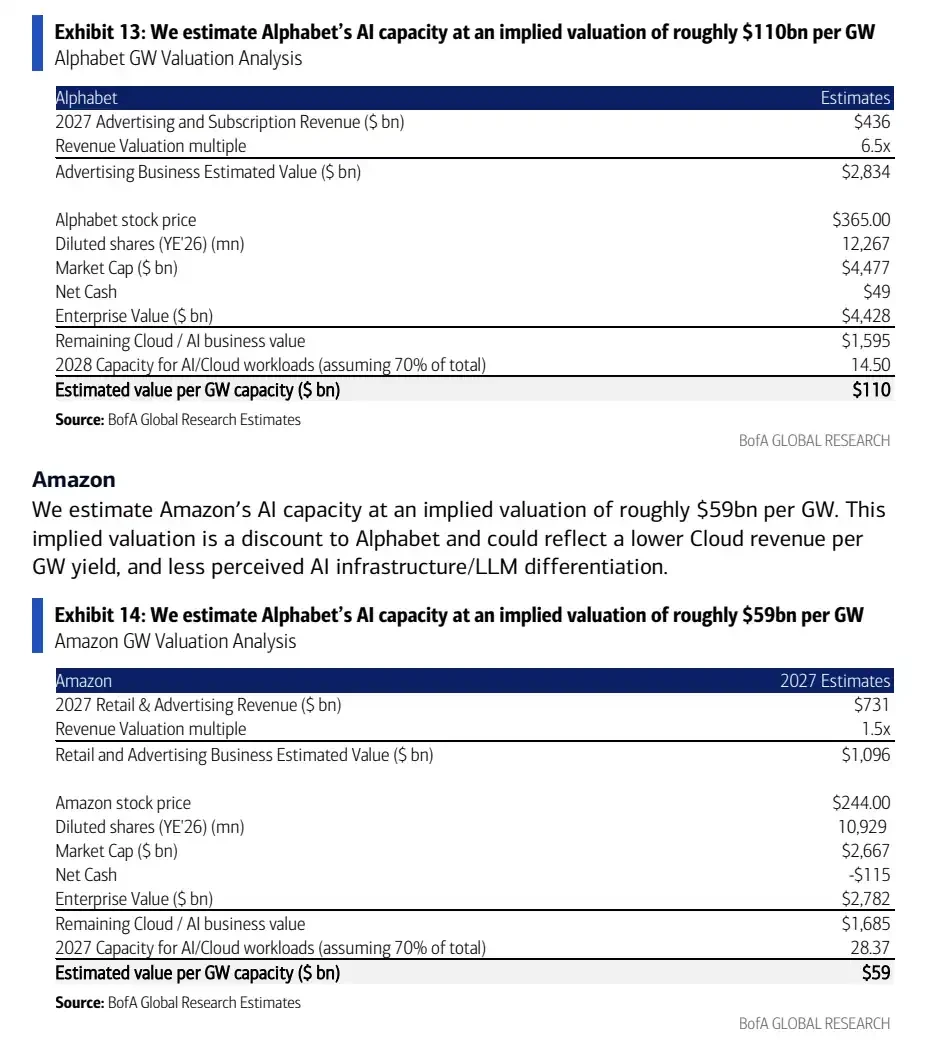

Bank of America’s valuation methodology involves first stripping out the value of the three companies’ traditional businesses, and then deriving the market’s implied value for their AI capacity.

After back-calculating based on 2027 multiples for core advertising, retail, etc., Meta’s implied valuation per GW of AI capacity is only about $4 billion. Alphabet is approximately $110 billion/GW, and Amazon is about $59 billion/GW.

This gap directly points to the differences in the commercialization paths of the three companies. The market is more willing to view Alphabet and Amazon’s data center capacity as monetizable assets, but remains notably cautious about Meta’s AI capacity.

Comparison of implied valuation per GW of capacity: Alphabet ~$110 billion, Amazon ~$59 billion, Meta ~$4 billion.

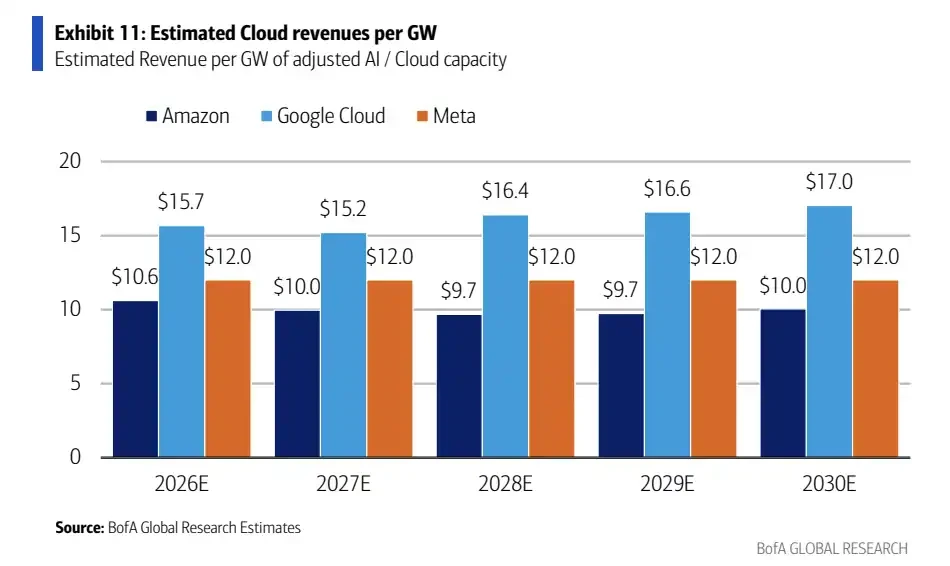

The capacity of AWS and Google Cloud is more easily mapped to cloud revenue. According to Bank of America’s model, AWS’s cloud revenue per GW in 2026 is about $10.6 billion, and Google Cloud’s is about $15.7 billion. The revenue path is relatively clear, with enterprise clients purchasing cloud computing, AI training, and inference services.

Meta is different. It has a massive advertising business and AI recommendation systems, but its enterprise-level AI revenue is still in an early stage. Even if Meta accelerates the construction of AI data centers, the market will still ask: will this capacity primarily enhance its own advertising efficiency, or can it be sold externally like cloud providers?

If primarily used for internal products, the valuation method would be closer to advertising efficiency improvement rather than an independent cloud infrastructure asset. For Meta to achieve a higher valuation per GW, it needs to present a clearer path for enterprise AI products, subscription revenue, or Business Agent sales.

Meta’s Upside Hinges on Selling Its Capacity

In Bank of America’s optimistic scenario, Meta’s data center capacity could reach approximately 22.8 to 23GW by 2030. If 40% of this is used for enterprise AI sales, calculated at a revenue of $12 billion/GW, it implies a potential enterprise revenue opportunity of about $110 billion.

This remains a model assumption, not a management target or a confirmed revenue opportunity. It explains where the ‘Meta is undervalued’ narrative comes from: if Meta can productize part of its AI capacity in the future, selling AI services, subscription products, or Business Agent capabilities to enterprises, then the current implied value of about $4 billion/GW would appear very low.

Installed capacity growth forecast for Amazon, Google Cloud, and Meta from 2026 to 2030; Meta’s capacity is projected to be ~22.8GW by 2030.

The problem is that this assumption has not yet materialized. AWS and Google Cloud already have clients, contracts, and cloud revenue metrics. Meta needs to prove it is not just ‘building compute for itself’ but can also generate sustainable enterprise AI revenue.

Potential catalysts listed in the report include improvement in cloud gross margins, increased visibility for Meta’s enterprise AI and subscription products, and more detailed disclosure of AI revenue breakdowns. Some more forward-looking products and partnerships remain largely at the hypothetical level and cannot be directly counted as realized business contributions.

Estimated Cloud/AI revenue per GW, 2026-2030: AWS ~$10-10.6 billion, Google Cloud ~$15.2-17 billion, Meta conservative assumption ~$12 billion.

For Meta, what can truly change market perception is not announcing yet another larger data center plan, but showing investors what revenue this capacity can generate. Specifically, the proportion of enterprise AI sales, product form, and revenue disclosure are currently insufficiently clear.

The Cheapest Asset, Also the One That Needs to Prove Itself Most

Meta appears to have the cheapest AI capacity valuation among the three companies, but cheapness itself is not an answer.

The first constraint is power. The US Department of Energy webpage previously cited EPRI estimates that data center power consumption could reach up to about 9% of total US electricity usage by 2030, up from approximately 4% in 2023. Recent research ranges from EPRI and Lawrence Berkeley National Laboratory are even higher, suggesting power pressure may continue to rise. Power access, transmission lines, local permitting, and energy prices will all affect whether planned GW of capacity can be brought online on time.

The second constraint is chip supply and construction delivery. GPU availability, networking equipment, power infrastructure, and civil engineering timelines will all impact the pace of going live. An upward revision in capex does not mean capacity comes online immediately, nor does it mean revenue is immediately recognized.

The third constraint is customer willingness to pay. Enterprise AI demand is still growing, but the scale at which customers are willing to pay consistently for inference, training, and agent services requires further validation from financial reports. For Meta, if enterprise AI revenue cannot be clearly disclosed, the market will find it difficult to value its data center capacity by cloud provider standards.

Thus, Bank of America’s report does not conclude that ‘Meta has already realized AI value,’ but rather presents a more direct valuation contrast: against the backdrop of all three internet giants continuing to expand AI capex, the market prices Meta’s data center capacity the lowest. It also has the most to prove: not only must it build the capacity, but it must also convince investors that this capacity can translate into visible revenue.

Related: 3 Billion to 10 Million: Messari Still Sold at a Bargain Price

On June 12, Blockworks, a leading platform at the intersection of crypto data and capital markets, announced the acquisition of its long-time competitor Messari for over $10 million. Messari, which was valued at approximately $300 million in 2022, sold at a significant discount, highlighting the survival pressures faced by high-valuation startups and the consolidation wave in the data infrastructure sector during a prolonged bear market. Blockworks co-founder Jason Yanowitz stated in the official announcement, “For eight years, Messari has provided the industry with transparency, market intelligence, and comprehensive data coverage for every crypto asset, building the industry’s most comprehensive dataset. This integration will combine Blockworks’ strengths in issuer disclosure, investor relations, and compliance workflows with Messari’s advantages in data breadth and API capabilities to build a ‘single source of truth’…