Original Translation: Chopper, Foresight News

For years, stablecoins have been searching for their core identity.

Initially, they served as a trading tool for moving dollar assets between exchanges. Then, stablecoins evolved into a savings instrument, held as a long-term asset rather than for daily spending. Now, the data points to a new direction: stablecoins are becoming a core global financial infrastructure.

The following nine charts illustrate the underlying trends driving this transformation.

Regulatory Clarity Accelerates 市場 Growth

For most of their development, regulatory uncertainty has long hindered institutional capital from entering the stablecoin market. With the passage of the GENIUS Act, the regulatory framework has become clearer. This legislation didn’t create the industry trend but rather accelerated it.

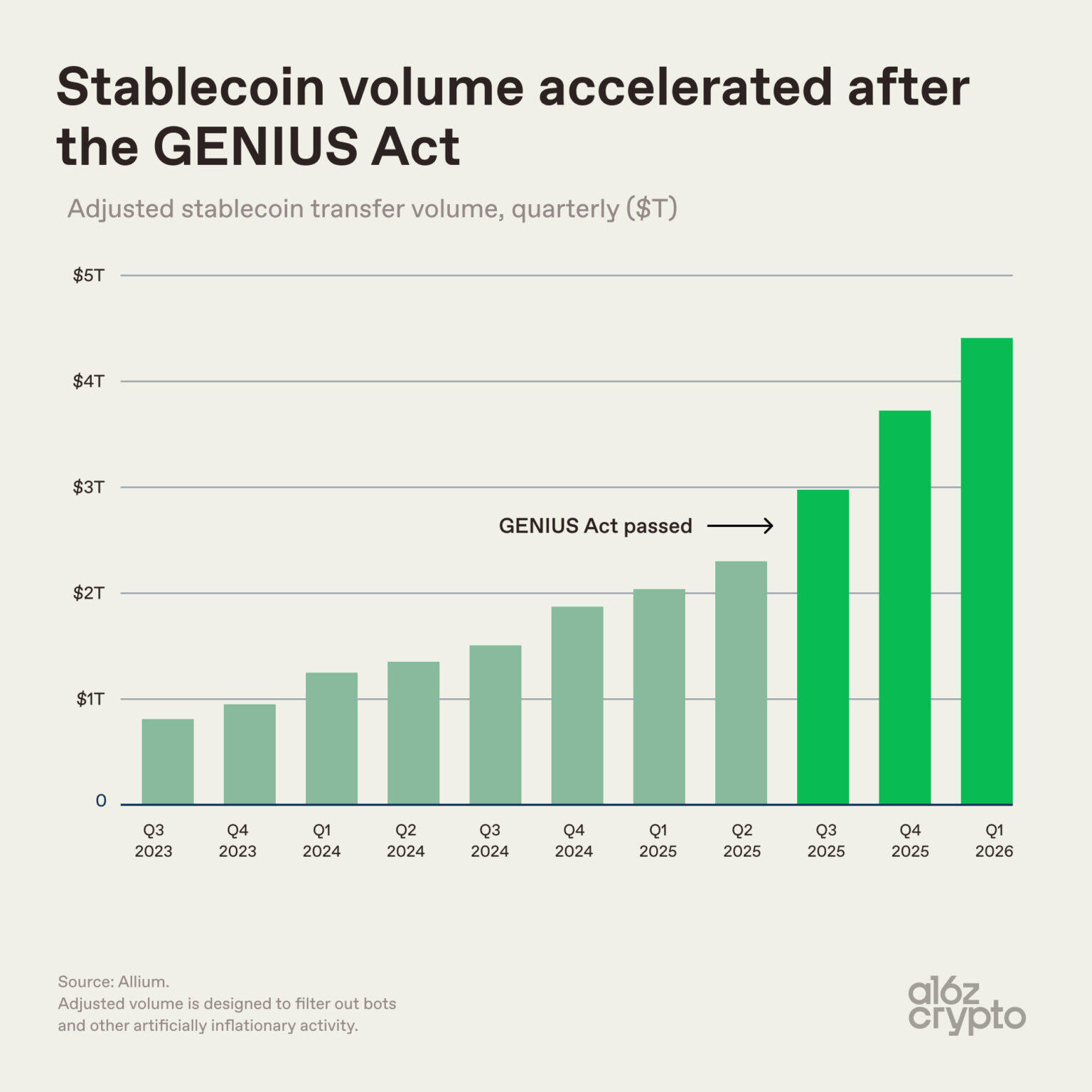

Stablecoin transaction volume before and after the GENIUS Act

The U.S. passage of the GENIUS Act established the first federal regulatory framework for stablecoin issuance. The data clearly reflects the policy impact: in the quarters leading up to the bill’s passage, adjusted stablecoin transaction volumes were already rising; after it took effect, growth accelerated further, reaching approximately $4.5 trillion in transaction volume in Q1 2026.

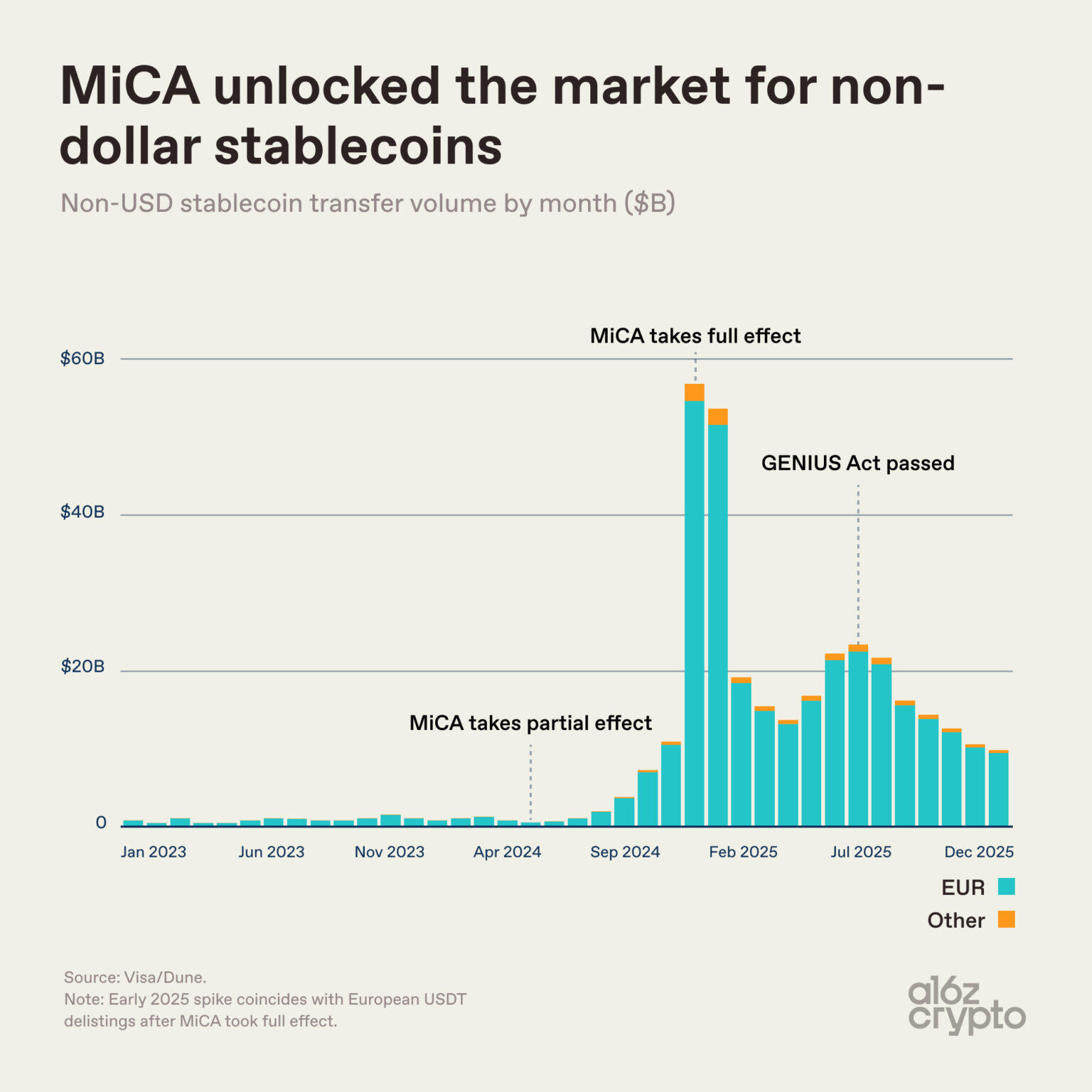

MiCA boosts the non-USD stablecoin market

The implementation of Europe’s Markets in Crypto-Assets Regulation (MiCA) presents a more complex picture. After MiCA came into full effect in late 2024, several major exchanges delisted USDT for compliance reasons, directly causing a short-term surge in non-USD stablecoin trading volume, peaking at over $40 billion.

Market transaction volume has since stabilized, but the overall base level is significantly higher than before MiCA, with monthly trading volume consistently between $15 billion and $25 billion. The new regulations have created a previously non-existent market for demand-driven non-USD stablecoins.

Stablecoin Commercial Payments Landscape Continues to Expand

Perhaps the most important shift in market structure lies in how people actually use stablecoins.

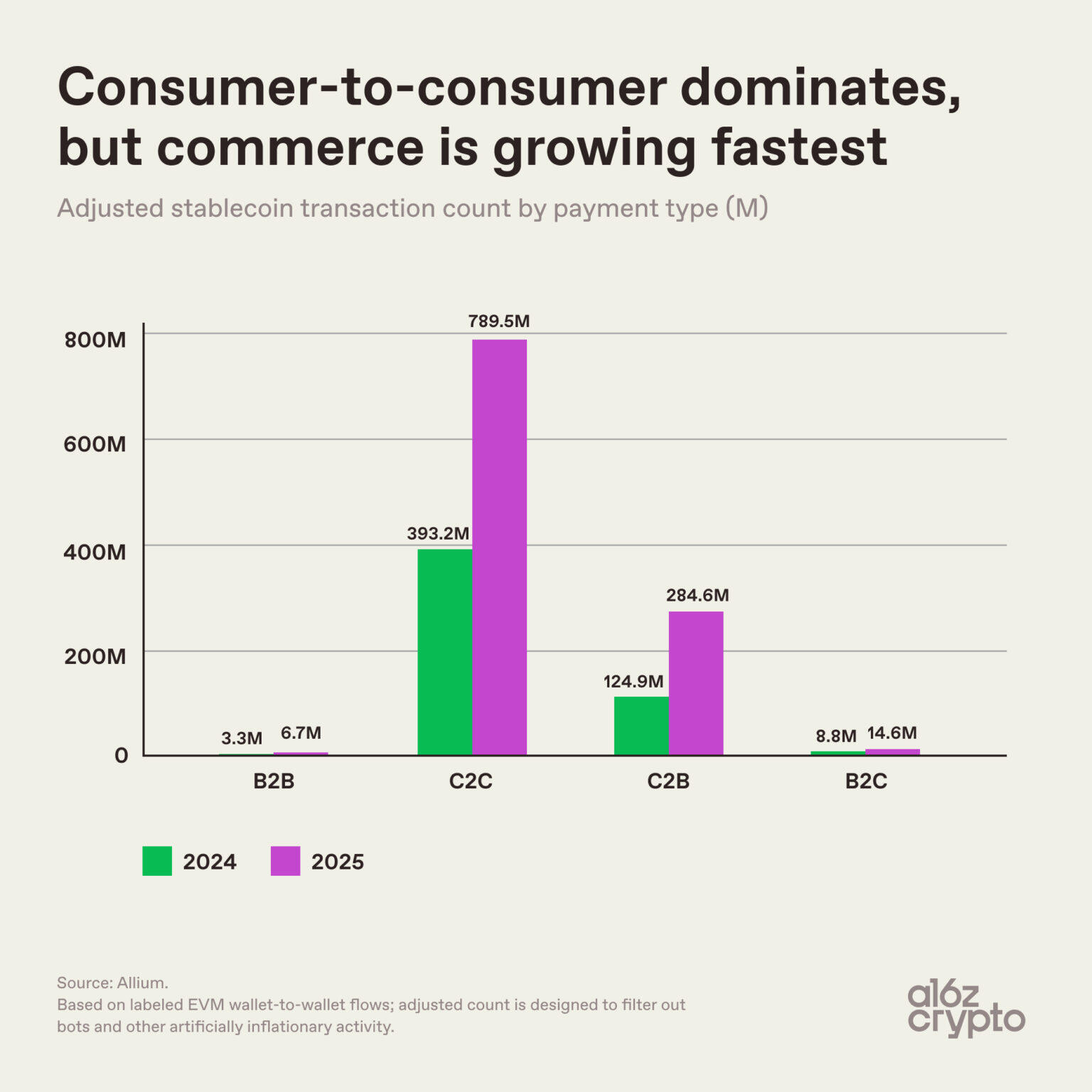

Stablecoin commercial payments concentrated in C2C

By transaction count, peer-to-peer (C2C) transactions are far ahead, reaching 789.5 million in 2025. Meanwhile, consumer-to-business (C2B) transactions saw the fastest growth, increasing from 124.9 million transactions in 2024 to 284.6 million in 2025, a year-over-year increase of 128%.

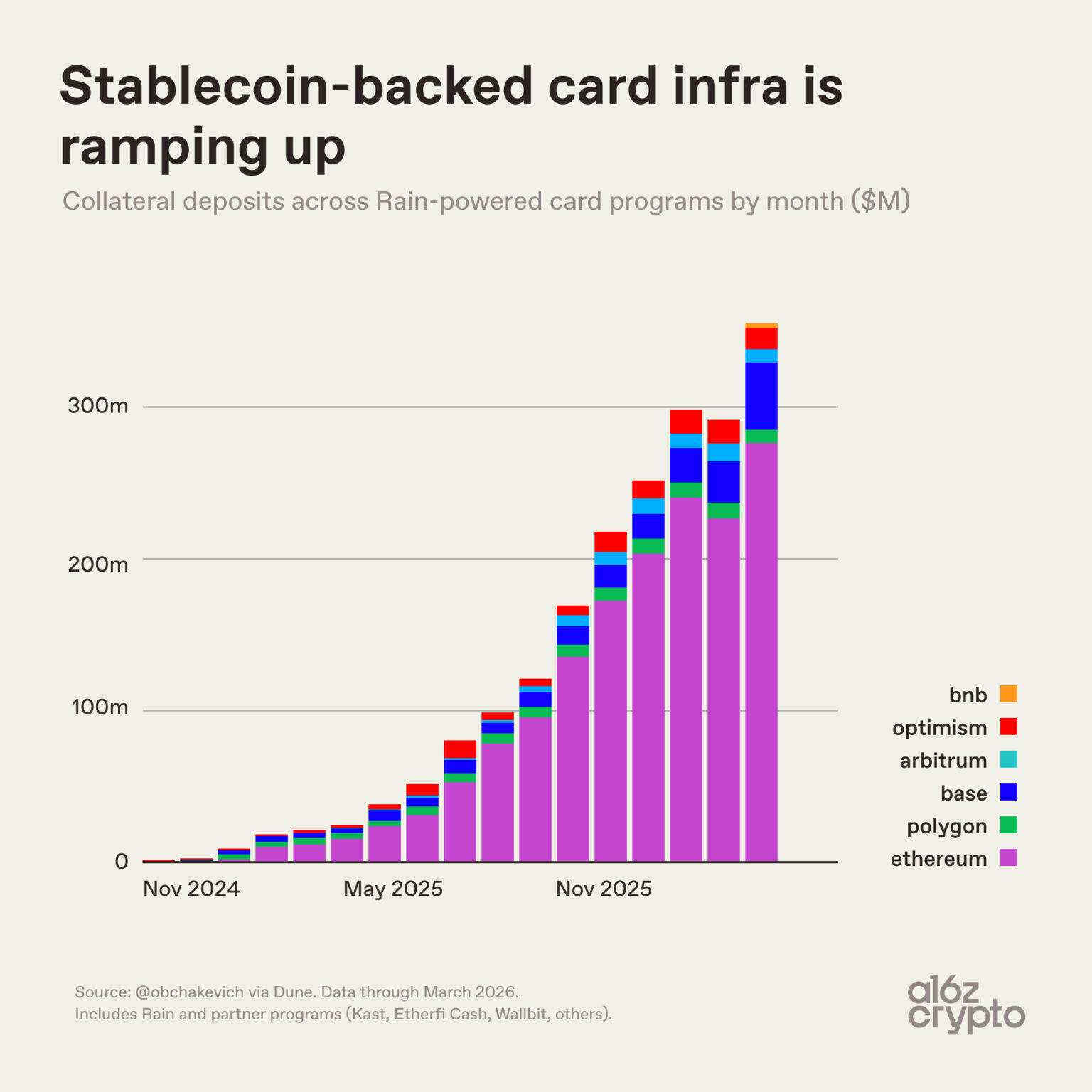

Growth trend of stablecoin payment card infrastructure

Data from stablecoin payment cards also confirms this trend.

Stablecoin payment card projects leveraging Rain technology (including Etherfi Cash, Kast, Wallbit, etc.) saw their monthly collateral deposits skyrocket from near zero in November 2024 to over $300 million per month by early 2026. While this capital serves as collateral for payment spending, not direct stablecoin consumption, its growth curve is highly indicative: the commercial payment use case for stablecoins is comprehensively on the rise.

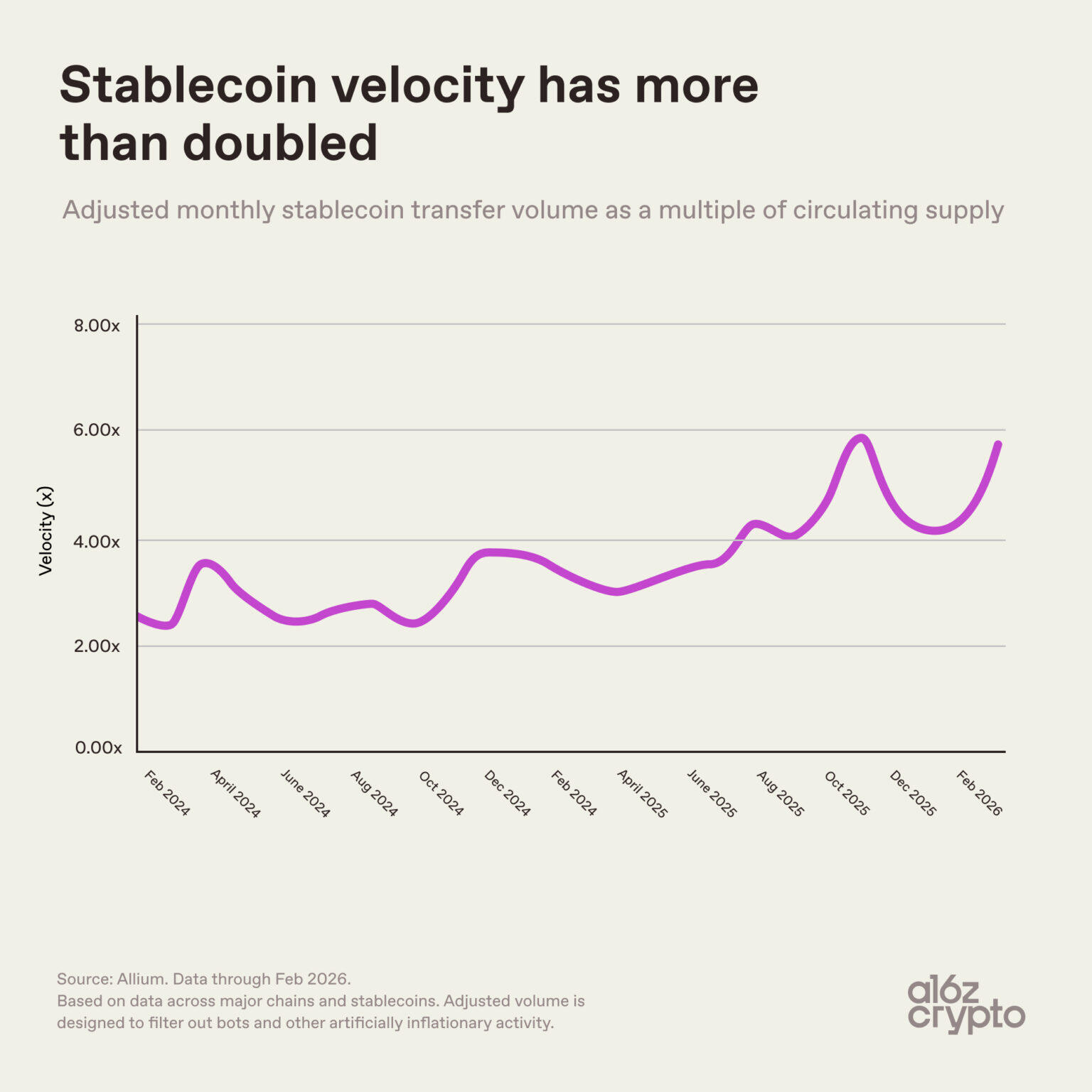

Stablecoin Velocity Significantly Increases

The circulation frequency of each dollar of stablecoin is constantly accelerating.

Stablecoin velocity trend

Since the beginning of 2024, stablecoin velocity (adjusted monthly transfer volume ÷ market cap) has nearly doubled, climbing from 2.6x to 6x. This increase signifies that the demand for stablecoin transactions is growing faster than the rate of new issuance, greatly improving the utilization efficiency of existing capital.

This is also a core characteristic of a mature payment network: the underlying currency is used frequently, rather than simply held passively.

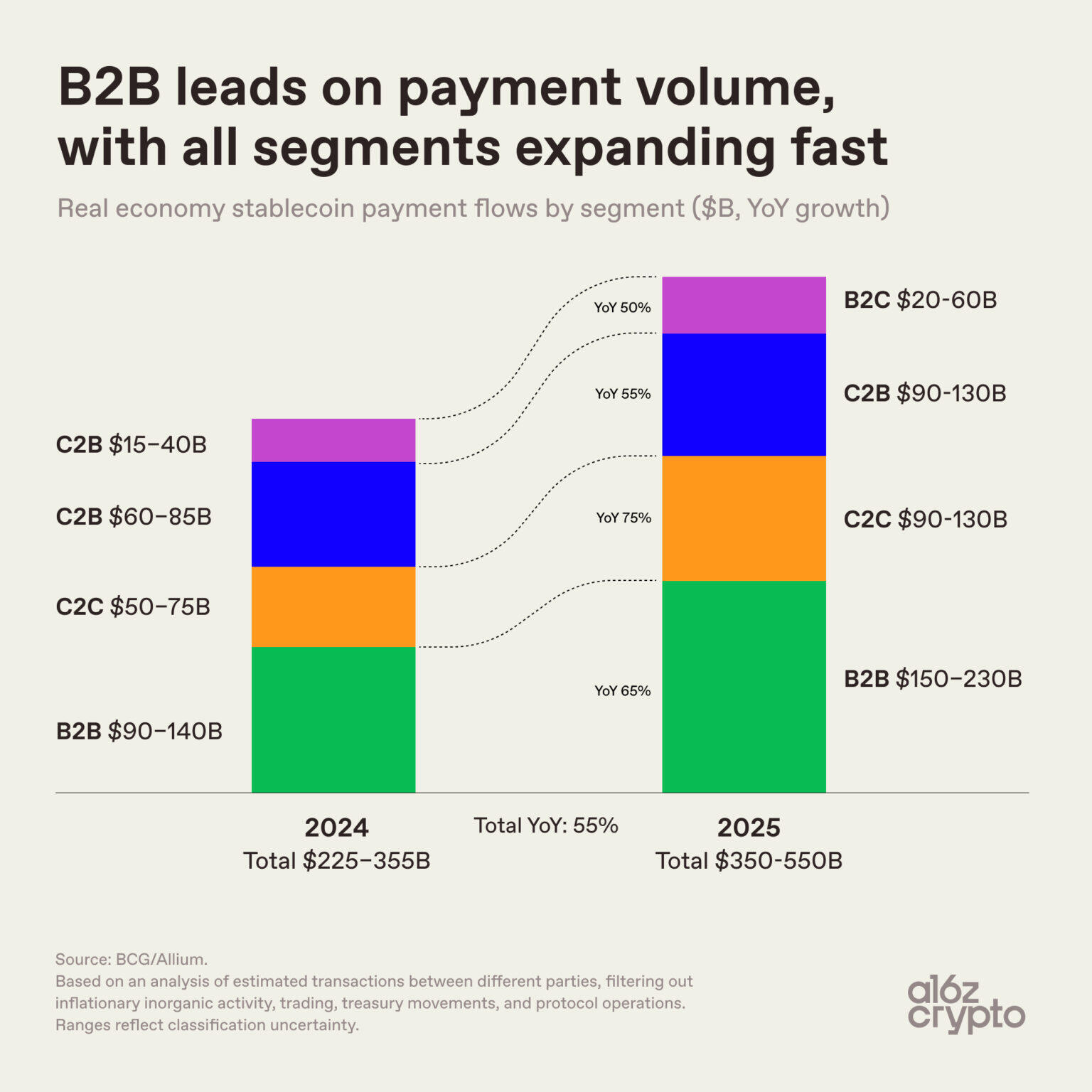

Shifting Transaction Structure Highlights Payment Utility

Excluding activities like trading, fund flows, and exchange mechanisms (which constitute the majority of stablecoin transactions), the estimated payment volume between different parties last year was between $350 billion and $550 billion.

B2B stablecoin payments dominate

Business-to-business (B2B) remains the cornerstone of stablecoin payments, holding the top position in volume. At the same time, specific segments like personal transfers and merchant payments are expanding rapidly.

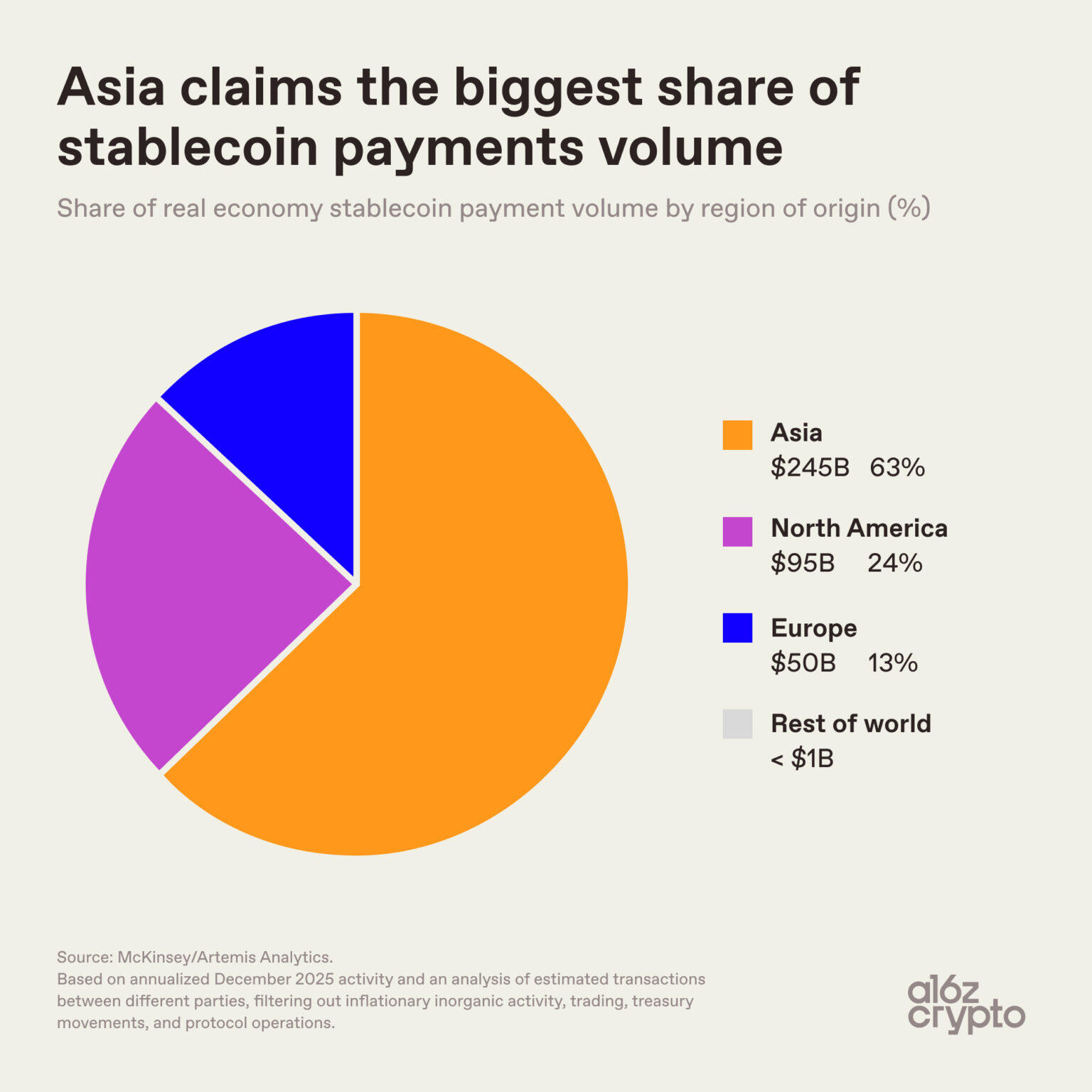

Geographic Concentration of Stablecoin Payments is High

Geographically, stablecoin payment activity is not evenly distributed.

Asia is the primary region for stablecoin payments

Nearly two-thirds of the transaction volume originates from Asia, primarily from Singapore, Hong Kong SAR, and Japan.

North America accounts for roughly one-quarter of the volume, and Europe about 13%. The combined size of Latin America and Africa is minimal, totaling less than $1 billion.

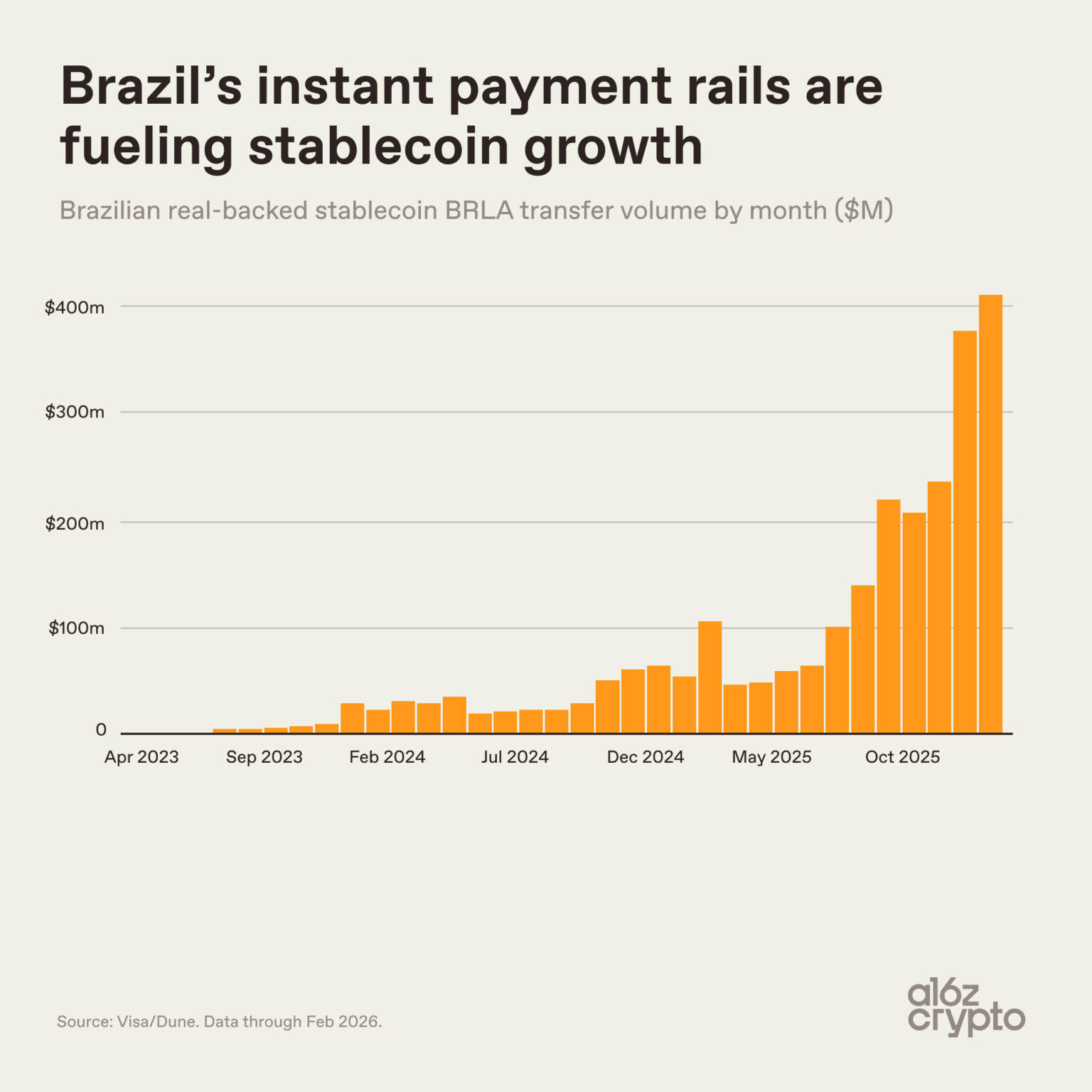

Local Stablecoins Operate on Global Underlying Networks

The rise of non-USD stablecoins is not unique to Europe; they are also rapidly gaining traction in emerging markets, driven by different motivations.

Monthly transfer volume of Brazilian Real-pegged stablecoin BRLA

Brazil is a clear example. The monthly transaction volume of the Brazilian Real-backed stablecoin BRLA grew from near zero in early 2023 to approximately $400 million by early 2026. Integration with Brazil’s instant payment network, PIX, has significantly boosted BRLA’s adoption.

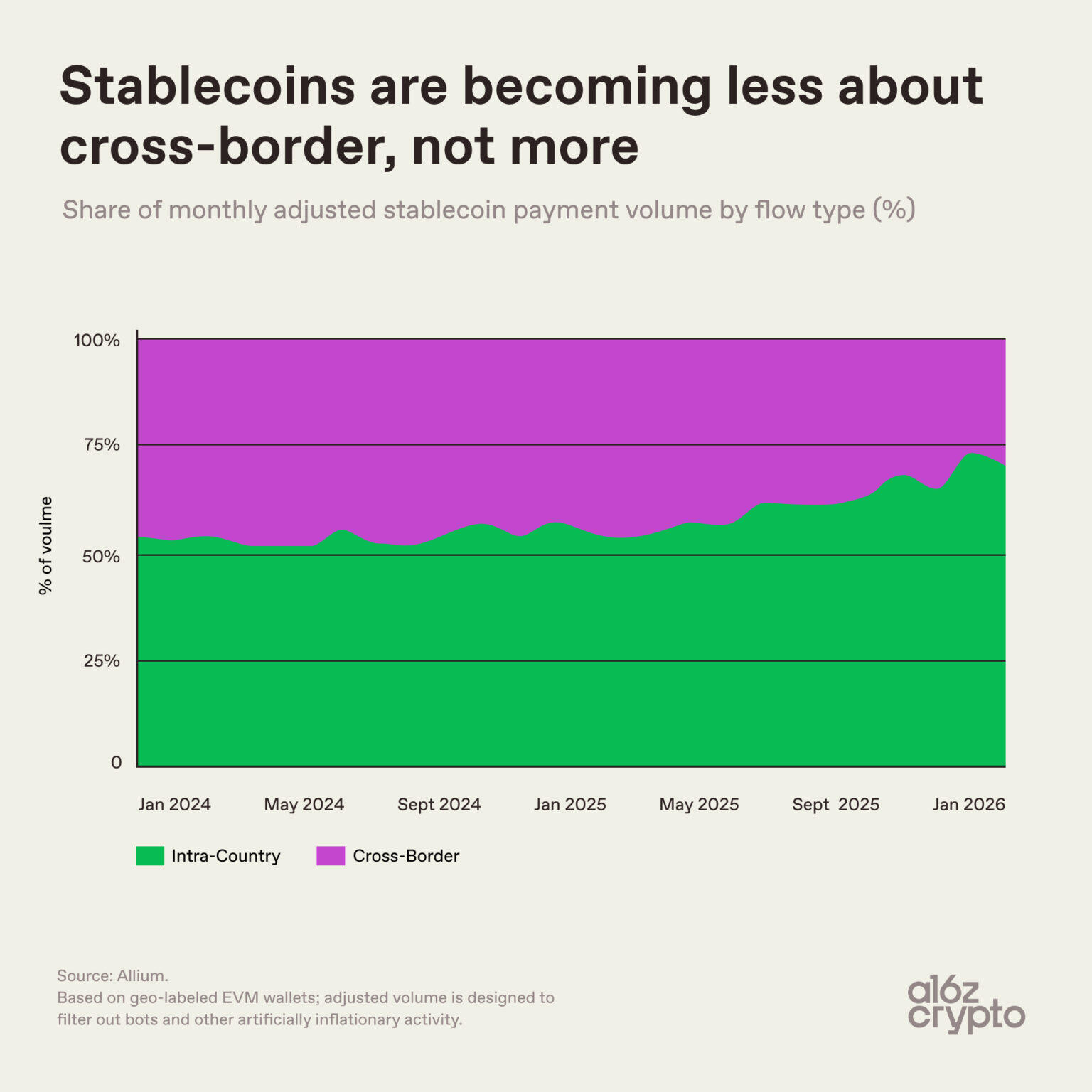

The cross-border payment attribute of stablecoins is diminishing

For a long time, stablecoins have been widely 德菲ned as a cross-border tool, but the actual proportion of cross-border transactions is steadily declining.

The share of domestic, on-chain transactions rose from about 50% in early 2024 to nearly 70% in early 2026. This change sends a clear signal: the core value of stablecoins is no longer limited to cross-border remittances and currency exchange. They are gradually transforming into localized everyday payment tools, leveraging global underlying networks.

結論

Taking all the data together, a clear industry picture has emerged, starkly different from past expectations: the consensus was that the core value of stablecoins lay in cross-border transfers. The reality is quite the opposite; stablecoins are becoming deeply localized. While USD-pegged stablecoins currently dominate, non-USD stablecoins backed by local fiat currencies like the Euro and Brazilian Real are steadily increasing their market share.

Although peer-to-peer transfers remain the primary use case for stablecoins, the proportion of daily commercial payments is steadily rising.

Data from each successive quarter reinforces this: stablecoins are progressively evolving into a universal public payment infrastructure. They were born with a global nature, yet their practical application is becoming increasingly localized.

The industry is still in its early stages, but the final form and developmental landscape of stablecoins are becoming increasingly clear.

本文源自網路: a16z: Understanding the Future Direction of Stablecoins Through 9 Charts

Author|Azuma (@azuma_eth) The threat of quantum computing to 加密貨幣currencies has once again become a focal point of discussion on international platforms. The so-called “quantum threat” refers to the possibility that sufficiently powerful quantum computers in the future could break the cryptographic foundations that currently secure cryptocurrencies, potentially destroying their security models. In November last year, when Vitalik discussed the quantum threat at the Devconnect conference, Odaily published an article titled “Is the Quantum Threat Resurfacing, Shaking the Foundation of Cryptocurrencies?”. The core argument of that article was that while the quantum threat objectively exists, first, there is still some time before a real threat materializes; and second, cryptocurrencies can be upgraded to incorporate post-quantum algorithms, thereby completing a “lock change”. In other words, it was a matter of “worthy of…