The Endgame of Crypto Neo-Banks: Licenses, Stablecoins, and Super Apps—Who Will Prevail?

Original Compilation: Chopper, Foresight News

If you ask ten криптовалюта users what a neobank is, you might get the same answer: a card that allows spending with stablecoins. But if you ask ten developers, the answers could be all over the place. Some are developing non-custodial wallets linked to Visa cards; others are forking Aave and calling it a savings account; and still others are applying for full banking licenses.

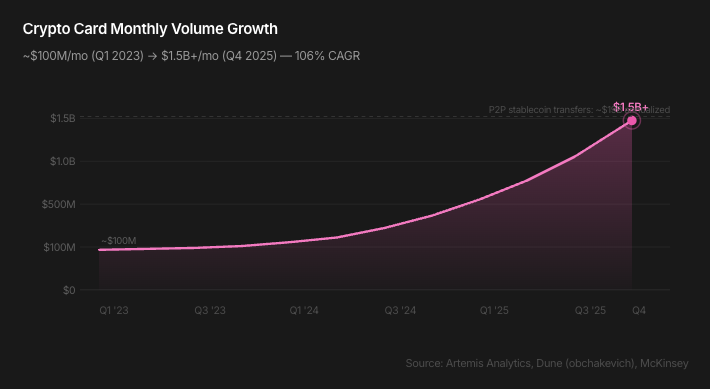

Monthly transaction volume for crypto debit cards grew from around $100 million at the beginning of 2023 to over $1.5 billion by the end of 2025 (a 106% CAGR), with the market’s annualized scale exceeding $18 billion. Card spending linked to stablecoins reached $4.5 billion in 2025, a 673% year-over-year increase.

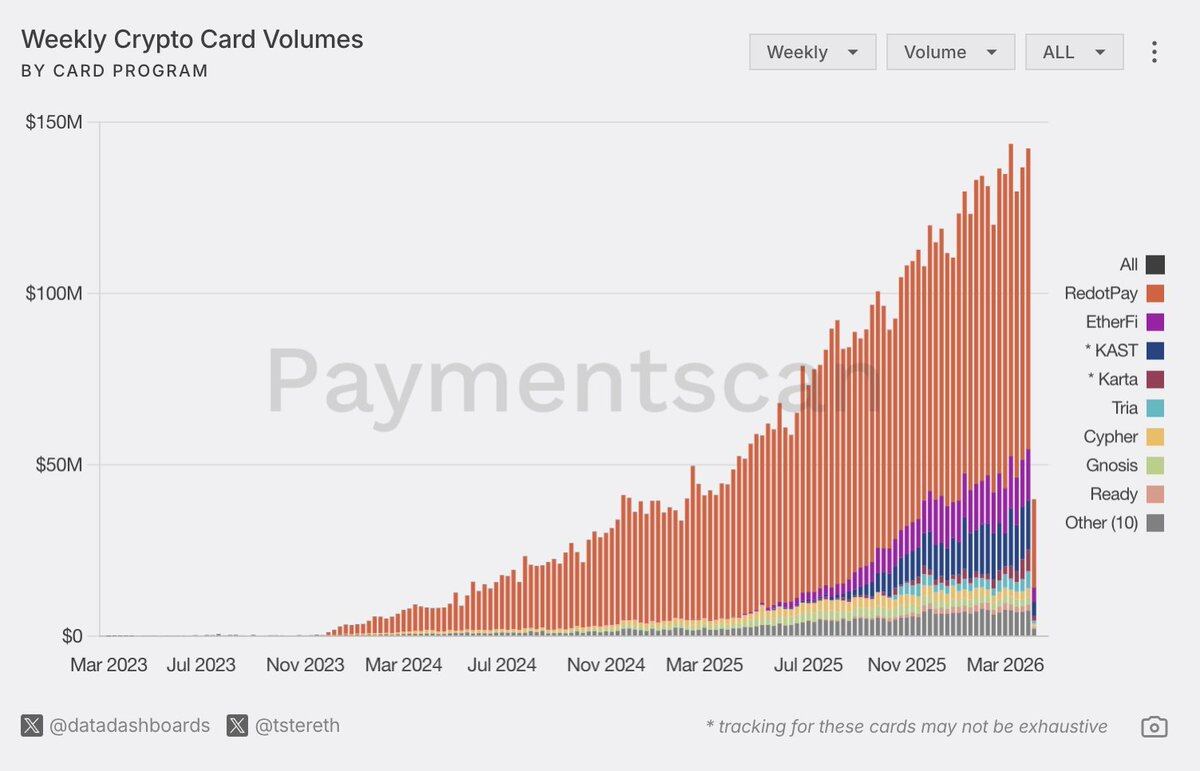

However, the entities actually processing this volume are highly concentrated. Data shows that RedotPay, a custodial platform based in Asia, commands a 60% market share, with transaction volume roughly four times the combined total of its next 13 closest competitors. On the transaction volume leaderboard, DeFi-native, self-custodial virtual banks are completely left in the dust.

Yet, the deeper trend is that crypto-friendly giants are accelerating their entry. Between December 2025 and March 2026:

- Coinbase applied for a US national trust charter

- Nubank received conditional approval from the US Office of the Comptroller of the Currency (OCC) to establish a national bank

- PayPal applied to establish PayPal Bank

- Revolut obtained a full UK banking license and is progressing with its US license application

- Kraken became the first crypto company to hold a master account with the Federal Reserve

Within 83 days, 11 companies applied to the OCC for trust bank charters, including Circle, Ripple, BitGo, Paxos, Fidelity, Bridge, Crypto.com, Morgan Stanley, Payoneer, Zerohash, and Protego.

Over 50 crypto neobanks have already launched. According to business research firms, the global neobank market size is projected to reach $552 billion in 2026. We attempt to map out the landscape of this sector, not only to understand who is building what, but also who has the capacity to survive.

A Tense Competitive Landscape

Two core contradictions define the competitive landscape in the neobanking space.

The first is economic. 76% of traditional neobanks are unprofitable. The eventual winners (Nubank, Revolut, SoFi) did not profit from card swipes but from credit businesses and net interest income. Transaction fees are just the entry ticket; credit is the core business.

Today, crypto neobanks are competing on transaction fees and cashback, precisely the failed profit model of the previous generation of fintech companies. Furthermore, stablecoins have further compressed the foreign exchange spread, pushing it close to zero.

The second point is user choice. The crypto community champions DeFi yields and non-custodial wallets, but the reality of on-chain card transactions paints a completely different picture: the vast majority of crypto card spending is completed through custodial platforms. This isn’t because users don’t understand self-custody, but because in a scenario where one just wants to buy a coffee, a smooth account opening experience trumps asset sovereignty.

History repeats itself: webmail preceded encrypted email, Dropbox preceded self-hosted storage, centralized exchanges preceded DeFi. Whether crypto neobanks will follow the same trajectory—where the convenience of custodial models first wins the mass market, and non-custodial solutions gradually catch up as tools mature—remains an open question.

Four Types of Neobanks

Rather than dividing them as “Web2 vs Web3” (which only reflects technology, not business models), a more valuable perspective is to examine a neobank’s moat, unit economics, and growth ceiling.

Crypto-Friendly and Banking-First

The strongest neobank economic model comes from credit and monetization, not just payments.

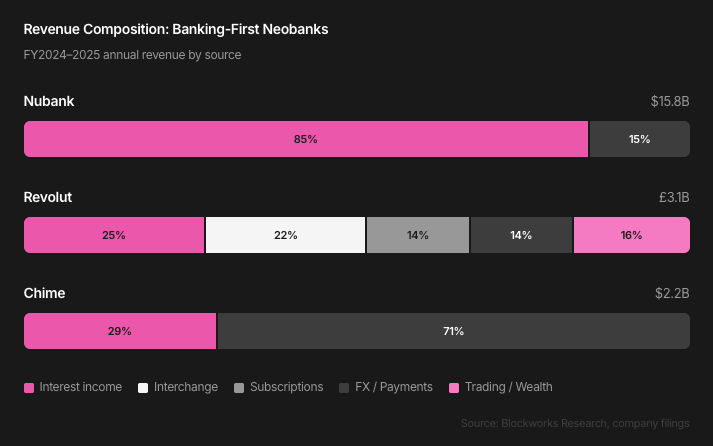

- Nubank’s FY2025 revenue was $15.8 billion, with 85% from interest income: $4.6 billion from credit card interest and $4.8 billion from loan interest. Monthly revenue per active user was $15, with a service cost of only $0.8, yielding a return rate of 19x.

- SoFi, which obtained a banking charter in 2022, saw its quarterly net interest income grow from $94.9 million to $617 million over four years. Its deposit costs are 181 basis points lower than warehouse financing, saving approximately $680 million annually.

- Revolut’s 2024 revenue was £3.1 billion, spread across five business lines, with no single line exceeding 30%. Its trading/wealth segment grew 298% year-over-year.

Licensed neobanks deliberately limit stablecoins to the payment stage because the profit core lies in credit business.

- Revolut does not offer yields on stablecoin balances. Its proprietary stablecoin, tested in the UK FCA sandbox in February 2026, is positioned as payment infrastructure, not a savings product.

- SoFi’s stablecoin (SoFiUSD, launched December 2025) is a settlement tool via the Mastercard channel.

This strategy is built on specific market conditions: current on-chain yields lack competitiveness. Aave v3 USDC’s recent annualized yield was only 2.6%, lower than SoFi’s savings account at 3.3% and Revolut Ultra at 4.25%. However, on-chain yields are significantly cyclical. During active DeFi periods, Aave USDC yields have reached 8%–10%, and Ethena’s funding rate-based yields have far exceeded that. This gap is cyclical; once it widens again, the competitive landscape will fundamentally change.

Commerce and Social Super Apps

MercadoPago, Grab, WeChat Pay, Alipay… They weren’t initially built to be banks but embedded finance within commercial applications. Their moat isn’t the product itself but their distribution channels and behavioral data, giving them superior risk control capabilities compared to traditional banks.

- MercadoPago’s credit income grew from $246 million in 2020 to $5.9 billion in 2025, a 24x increase over five years.

- Grab’s loan portfolio grew from $185 million in 2022 to $1.3 billion by the end of 2025, with financial services revenue reaching $348 million in FY2025.

Both platforms have experimented with stablecoins.

- MercadoPago launched Meli Dólar (MUSD) in Brazil and expanded to Chile and Mexico, but its circulating market cap is only $65 million, less than 0.4% of its $19 billion assets under management.

- Grab partnered with StraitsX for stablecoin settlement, allowing tourists to spend at GrabPay merchants in Singapore via Alipay, etc., with real-time settlement in XSGD stablecoin.

Neither has ventured into stablecoin yields, leaving a severely underestimated opportunity for crypto-native players.

Whop is worth watching. It’s not currently a neobank but a creator marketplace. After receiving a $200 million investment from Tether (valuing it at $1.6 billion), creators can receive USDT, hold stablecoins, and bypass bank settlements. Its integrations with Plasma and Aave can provide stablecoin yields, targeting 18.4 million users and $3 billion in annual creator revenue.

MercadoPago in 2003 wasn’t a neobank either, just a marketplace escrow service; financial relationships were gradually built around commercial scenarios. Whop is at the same starting point but built on crypto from day one.

For neobanks centered on payment cards, the most enduring financial relationships might not start with finance but with e-commerce.

Trading-First

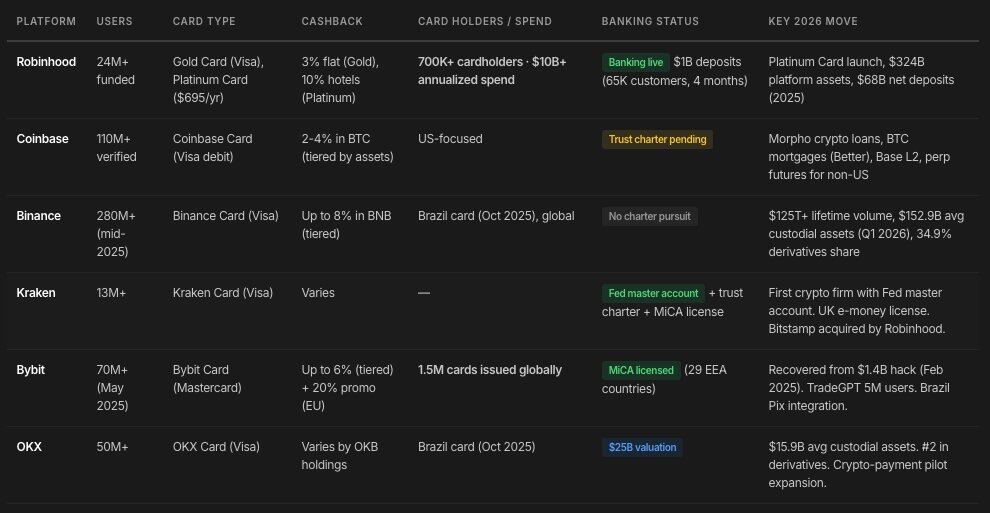

Robinhood, Coinbase, Binance, Kraken, Bybit, OKX… Starting from centralized crypto trading and expanding into crypto banking. All platforms in this camp are building a banking layer, aiming to create revenue streams independent of crypto bull markets.

- Robinhood is the most typical example: total platform assets grew approximately 70% year-over-year to $324 billion, with net deposits reaching a record $68 billion.

- Coinbase is fully entering the neobank space: it has its own L2 network Base, a wallet with card functionality, crypto-collateralized loans based on Morpho, Bitcoin-collateralized mortgages in partnership with Better, and is applying for a trust charter.

- Kraken already holds a trust charter and has obtained a master account with the Federal Reserve.

These platforms start from a scaled trading business and layer banking services on top. Stablecoin-first neobanks, however, go the opposite way: starting from thin transaction fees and trying to layer on other businesses, a significantly more difficult path.

Stablecoin-First

Dozens of platforms like Ether.fi, Gnosis Pay, RedotPay, KAST, Holyheld, Bleap, Ready, Tria, Cypher, Payy, etc. They leverage the lower operational costs brought by stablecoins and DeFi composability as backend product infrastructure, with a clear value proposition:

- Self-custody model

- DeFi yields (5%–15% APY in active markets, higher than traditional savings at 3%–4%)

- Near-instant cross-border payments via stablecoin rails with minimal fees

- Global accessibility, no geographical restrictions

Stablecoin-first neobanks possess the most obvious structural advantages in emerging markets and cross-border scenarios. But their weaknesses are equally prominent:

- None have yet achieved large-scale unsecured lending businesses

- Competing in the thinnest-margin transaction fee segment, using token subsidies for cashback to acquire customers

- They compress foreign exchange profits and settlement fees to near zero, eroding the revenue early neobanks relied on for survival.

The Infrastructure Layer

Most crypto neobanks are just frontends on top of shared infrastructure. Understanding the underlying architecture is key to assessing their moat.

Concentration Risk

Card Networks (Visa, Mastercard): Despite having a similar number of partnered programs (around 130 each), Visa, through early partnerships with crypto-native infrastructure providers, commands over 90% of on-chain card payment transaction volume. This is a single point of failure for the entire industry: if Visa adjusts its crypto project policies, halts expansion, or raises fees, the industry’s economic model could be rewritten overnight.

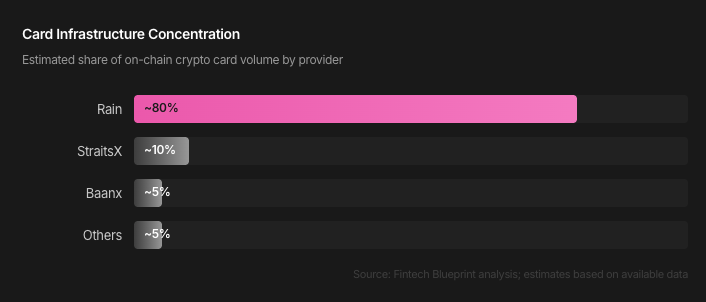

Issuing Processors (Rain, Reap, Baanx, StraitsX): Regulated bridges connecting on-chain and traditional finance. The most significant structural change is the emergence of full-stack issuing processors: directly holding Visa/Mastercard core membership, combining program management and card issuance, bypassing traditional sponsor banks.

Most crypto neobanks share the same backend. Rain powers Ether.fi, RedotPay, Avalanche Card. If Rain experiences technical failures, regulatory issues, or a strategic pivot, the entire industry is affected. A Solus Partners report covering 19 platforms listed infrastructure concentration and vendor dependency as systemic risks.

The Threat of Wallet-Native Stablecoins

An often-overlooked competitive variable: major wallets are issuing their own stablecoins, specifically for card payments, building closed-loop ecosystems to capture value that would otherwise belong to independent neobanks.

By the end of Q3 2025, MetaMask launched mUSD and Phantom launched CASH, both as funding sources for their own debit card products. Wallets no longer rely on users holding USDC or USDT; instead, they build closed loops where users convert assets into the wallet’s native stablecoin for card spending.

Early data shows divergent trends:

- Phantom’s CASH grew steadily from around $25 million in September to about $100 million in circulation by the end of December.

- MetaMask’s mUSD peaked at nearly $100 million in early October before falling back to around $25 million, a 75% decline.

Through this model, wallets can capture transaction fees, spreads, and reserve yield—value that would otherwise flow to stablecoin issuers. Independent crypto neobanks could lose a significant portion of their core value as a result. MetaMask, Phantom, and Coinbase Wallet directly control user relationships; adding banking features is just a product line extension, not a new business.

The Unit Economics Dilemma

76% of traditional neobanks are unprofitable, and crypto-native players are inheriting this failed model, with stablecoins making matters worse.

The lesson from banking-first companies is clear: payments are distribution, not the business itself.

Nubank’s 85% revenue from interest and SoFi’s reliance on its charter to expand net interest margins prove this point. Crypto neobanks that treat card spending as their core revenue engine are building on sand.

The sustainable model is to treat bank cards as a user acquisition channel while profiting through higher-margin on-chain finance, including DeFi yields, exchange, structured products, and credit.

Five Things That Could Change the Game

On-Chain Credit Scoring

In crypto, wallet transaction history (DeFi usage, loan protocol repayment records, staking duration, transaction frequency, protocol diversity, etc.) can serve as risk assessment data. No crypto neobank has implemented this at scale yet. Whoever cracks this puzzle can unlock a neobank operating model on a permissionless platform.

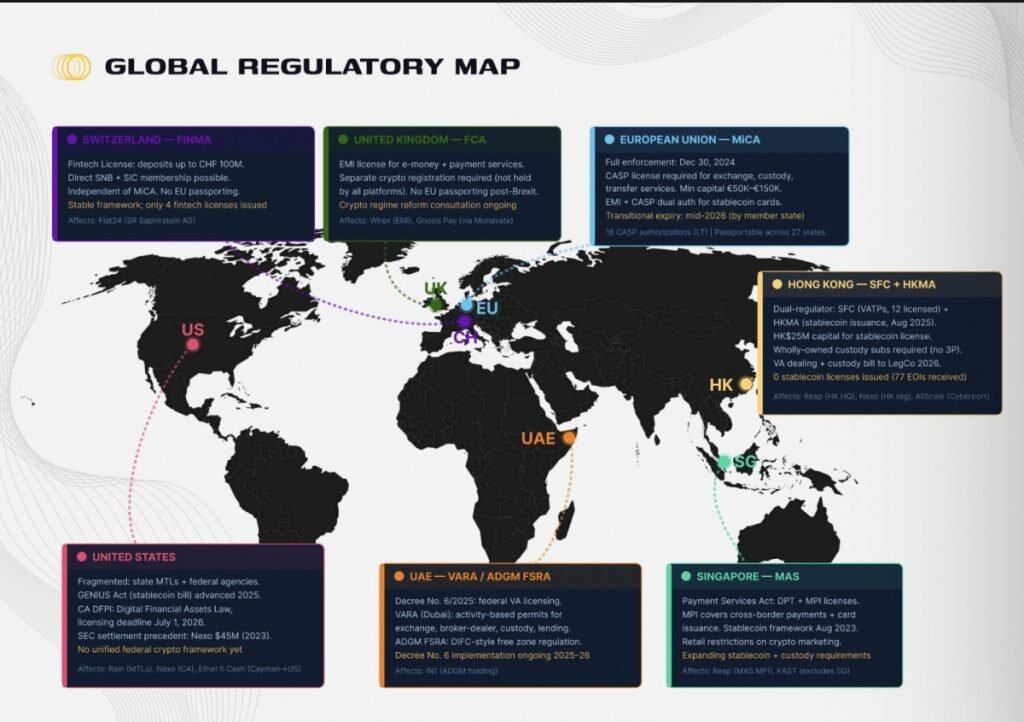

Full Banking Licenses for Crypto-Native Players

Not just custodial trust charters, but full licenses allowing deposit-taking and lending. This would allow crypto-native institutions to build credit businesses funded by stablecoin deposits at costs lower than warehouse financing.

Regulatory Clarity

Major markets are aligning on regulation: stablecoin issuers cannot pay yields. The US and Europe have drawn clear lines; major Asian markets like Japan, Singapore, and Hong Kong are also taking similarly conservative stances.

Agent-Driven Finance

Agents executing financial operations on behalf of users: portfolio rebalancing, yield optimization, payment management, cross-protocol strategy execution. Mastercard’s crypto partnerships grew from 6 in 2024 to over 25 in 2025; Visa launched Smart Business Connect, allowing AI agents to spend on behalf of consumers at global merchants. Whoever builds the best agent infrastructure on stablecoin rails will capture the next wave of e-commerce distribution.

Combining Self-Custody UX with On-Chain Abstraction

Crypto neobanks still rely on card network rails, but terminal technology to bypass them already exists: stablecoin-settled QR payments, NFC tap-to-pay independent of Apple Pay/Google Pay, physical card swipes settling directly on-chain. Projects like OpenPasskey (built on Base) have validated feasibility: possessing an ISO-assigned Issuer Identification Number, P-256 encryption, fully non-custodial crypto cards.

Who Will Win?

The answer is unknown, but key nodes have emerged.

- Licensed neobanks have a proven economic model and hold an advantage in credit-driven developed markets.

- Stablecoin-first neobanks offer globally accessible dollars, local stablecoins for emerging markets, and DeFi yields, but data shows users still prefer convenience over crypto-native ideals.

- Commerce-embedded players may have the deepest moats because they already control traffic distribution. But layering crypto onto mature infrastructure is costly, requires user education, and is highly dependent on regulatory clarity.

- Infrastructure (issuing processors, custodians, fiat on/off-ramps, core banking, blockchain settlement, KYC/AML) is destined to capture more value than any consumer brand.

Over 40 stablecoin cards are competing by offering token-subsidized cashback, generally lacking real business moats and sharing infrastructure. In the next two years, most will be eliminated.

The crypto neobank landscape is at a critical inflection point.

Эта статья взята из интернета: The Endgame of Crypto Neo-Banks: Licenses, Stablecoins, and Super Apps—Who Will Prevail?

1. Top Токенs on CEXs Top 10 CEX Trading Volume and 24-hour Price Changes: BTC: -0.13% ETH: +0.99% SOL: -1.04% XRP: -0.16% BNB: -0.11% DOGE: -0.42% TRX: -1.78% ZEC: +7.57% NIGHT: +9.62% XAUT: +1.45% 24-hour Top Gainers (Data Source: OKX): RAY: +20.61% SKL: +20.06% ALGO: +18.69% ILV: +14.02% BLUR: +13.36% WET: +9.73% NIGHT: +9.23% MON: +8.40% ZEC: +7.60% QTUM: +6.95% 24-hour Top Gainers – Tokenized Stocks (Data Source: msx.com): DEFT: 57.31% VCX: 21.6% FLY: 21.21% SOXL: 21.2% CONL: 19% ABTC: 17.51% APLD: 16.67% BBAI: 16.45% SATL: 15.49% MRVL: 15.21% 2. Top 5 On-chain Meme Coins (Data Source: GMGN): CHICKY BIP360 Buddy BELIEVE 80085 Headlines White House Considers Extreme Contingency Plan for Oil at $150, May Use Emergency Powers to Curb Fuel Costs According to informed sources and individuals close to…