Crypto Arbitrage Trading Is Dead: How Traditional Finance (TradFi) Perpetual Contracts Achieve 361.6% Yield

Core Summary (TL;DR)

- In this cycle, the funding rate arbitrage opportunities for mainstream kripto assets have been completely squeezed out by institutional basis trading capital.

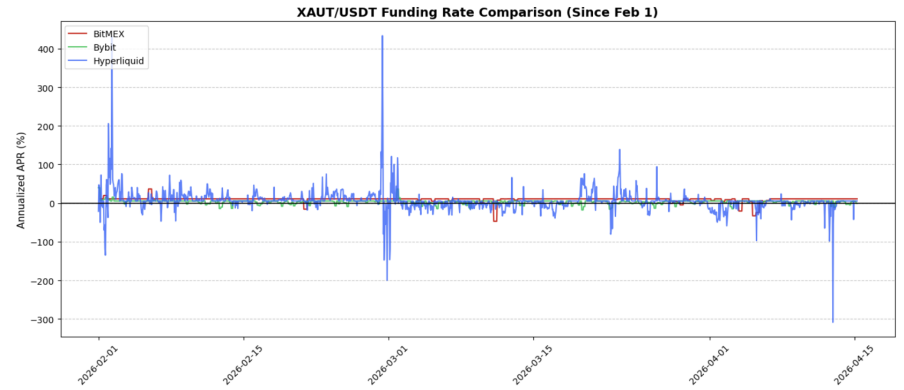

- On the XAUtUSDT pair, a simple “spot-perpetual” arbitrage on BitMEX achieved an approximate annualized return of 9.67% over the past 73 days, compared to 5.99% on Hyperliquid and 3.22% on Bybit.

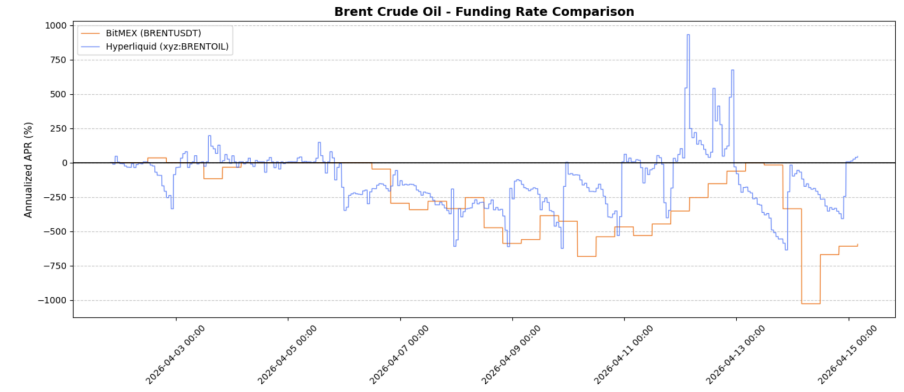

- The spread profit for Brent Oil is even more substantial: going long BRENTUSDT on BitMEX / shorting Brent on Hyperliquid yielded an implied annualized return of about 361.6% over 7 days, 220.7% over 14 days, and 103.0% over 30 days.

- Better opportunities now lie within BitMEX’s TradFi perpetuals—where assets are newer, capital flows are less mature, and the mispricing in funding rates remains significantly profitable.

Mainstream Crypto Arbitrage is No Longer Attractive

But that has changed. Since 2025, the pullback in funding rates for major coins has been severe, most notably impacting larger-cap assets more intensely. This indicates the old trading logic hasn’t broken down mechanically; it has simply been “competed away” by the arbitrage army. The easy profits have been swallowed by hedge funds, basis trading desks, and large structured players who now treat crypto arbitrage purely as a balance sheet business for large capital. Once funding rates rise to harvestable levels, big money quickly floods in and flattens them. The result is that funding rate returns today are no longer worth the effort traders must expend.

The Edge Has Shifted to TradFi Perpetuals

What has changed isn’t whether funding rate arbitrage exists, but where it exists. More interesting opportunities have migrated to TradFi perpetuals, where market structure remains young and capital flows are far from settled. These products occupy an unusual middle ground: they are macro financial instruments, but trade 24/7 on crypto infrastructure with a user base still learning how to price them correctly.

This is crucial because TradFi perpetuals behave differently from mature crypto contracts. They react to macro headlines, continue trading when underlying reference markets are closed, and are fragmented across platforms with vastly different participant profiles. This creates a more chaotic funding rate environment—and chaotic markets are where traders can capture outsized returns. Particularly on BitMEX, this opens a range of funding rate arbitrage opportunities far more attractive than the remnants left in mainstream crypto pairs.

Trading Opportunities: XAUt (Tether Gold) & BRENT (Crude Oil)

Trade Strategy 1: XAUtUSDT — A Purer, Steadier Arbitrage

The first opportunity is straightforward: buy XAUt spot on BitMEX while simultaneously shorting the XAUtUSDT perpetual on BitMEX, collecting funding in a delta-neutral structure. This is the classic arbitrage trade, simply applied to tokenized gold instead of mainstream crypto. Its appeal lies not just in the surface-level yield, but in the “quality” of that yield.

Over the past 1,759 hours (~73 days), the average annualized funding rate for XAUtUSDT on BitMEX reached 9.67%, easily outpacing Hyperliquid’s 5.99% and Bybit’s 3.22%. More importantly, BitMEX’s rate performance appears more stable. This is key because only an arbitrage trade you can hold is truly useful. Traders often focus on peak numbers, but the real value of a funding rate strategy lies in whether its behavior allows traders to realize profits without constant anxiety. Trades that look great on paper but swing wildly are difficult to scale and hold with confidence.

This is where XAUtUSDT stands out. It’s not the most dramatic trade in the market, but it’s more practical. At a time when most traditional crypto basis arbitrage has been compressed to insignificance, it offers a relatively clean, lower-maintenance version. For traders seeking steady yield strategies rather than tactical speculation, this is a more “civilized” setup.

Trade Strategy 2: Brent Crude Oil — A Higher-Octane Cross-Menukarkan Spread

The second opportunity is far more aggressive and explosive. On the Brent Crude Oil instrument, the funding rate differential between BitMEX and Hyperliquid has become one of the most visibly attractive cross-exchange spreads in the market today. The structure is simple: Go long BRENTUSDT on BitMEX while simultaneously shorting Brent on Hyperliquid.

The mechanics are equally simple. The funding rate for BRENTUSDT on BitMEX is frequently deeply negative, while the rate for Brent on Hyperliquid is typically positive. This creates a rare structure where traders can often collect funding on *both* sides of the trade. This is the “two-way funding capture” strategy traders once dreamed of in crypto markets, a golden age that has largely vanished in mature BTC and ETH ecosystems.

The data is extraordinarily strong. In a recent snapshot, BitMEX’s Brent funding rate was annualized at -594.585%, while Hyperliquid’s was 40.792%. Over the past 7 days, this spread implied an annualized return of approximately 361.607%, with 80.5% consistency. Over a 14-day period, the implied annualized return remained at 220.740%, and 103.012% over 30 days. In the 14-day and 30-day windows, BitMEX was the lower-cost platform to hold 65.4% of the time. These are not normal numbers for a mature market—and that’s precisely the point. Crude oil trading on crypto rails is still early, highly fragmented, and not yet fully arbitraged away, allowing spreads of this magnitude to persist.

Why Do These Opportunities Still Exist?

The deeper story is that TradFi perpetuals are still in the early stages of price discovery. They attract a different trading crowd than mainstream crypto, react more directly to macro and geopolitical news, and continue trading even when underlying reference markets are closed. This combination creates pricing distortions that simply wouldn’t survive in the crowded pools of mainstream coin arbitrage.

BitMEX is particularly interesting here because its TradFi perpetuals matrix is still young enough that these spread relationships haven’t been completely flattened by whale balance sheets. This creates an excellent hunting ground for traders. In essence, the market is still rewarding those willing to look beyond the obvious BTC/ETH funding trades for opportunities elsewhere.

Final Conclusion

The primary arena for traders seeking a genuine edge is no longer the old funding rate trades on mainstream crypto assets. That has become an intensely crowded institutionalized strategy, with competition compressing its returns to a point where they are no longer worthwhile relative to the risk and effort involved. Alpha hasn’t disappeared; it has simply relocated to corners of the market where structural inefficiencies still exist.

Right now, BitMEX’s TradFi perpetuals are one of the clearest places to find that Alpha. XAUtUSDT offers a purer, more stable arbitrage trade with ~9.67% annualized returns over the past 73 days; while BRENTUSDT, via the spread between BitMEX and Hyperliquid Brent contracts, offers a richer, more tactical spread opportunity with recent window data showing triple-digit annualized yields. The old arbitrage trade isn’t dead; it has just moved out of the market’s most congested lanes.

Artikel ini bersumber dari internet: Crypto Arbitrage Trading Is Dead: How Traditional Finance (TradFi) Perpetual Contracts Achieve 361.6% Yield

Related: Musk’s Terafab: One Man Challenges the AI Chip Dominance

Tesla, SpaceX, and xAI are jointly building Terafab—a $250 billion 2-nanometer chip fabrication plant. It integrates chip design, lithography, manufacturing, packaging, and testing all under one roof. The first product, Tesla AI5, boasts single-chip performance close to NVIDIA’s H100, with claimed inference costs 10 times cheaper. Sample chips are planned for late 2026, with mass production in 2027. Target capacity: 1 terawatt of AI computing power annually—50 times the current global total AI computing power. 80% of these chips will be sent into space, running AI on satellites and distributed back to Earth via Starlink. Only 20% will remain on Earth. Because the electricity required for 1 terawatt of computing power is simply beyond what Earth’s power grid can supply—space offers 5 times the solar radiation, higher vacuum cooling efficiency,…