At the beginning of 2026, we were all set up by Wintermute

At the beginning of 2026, the sharp fluctuations in Bitcoin’s price have once again thrust the kripto market maker Wintermute into the spotlight.

During the New Year holiday, a window of notoriously thin global market liquidity, Wintermute frequently made large deposits to Binance, sparking intense community speculation about “institutions secretly dumping.”

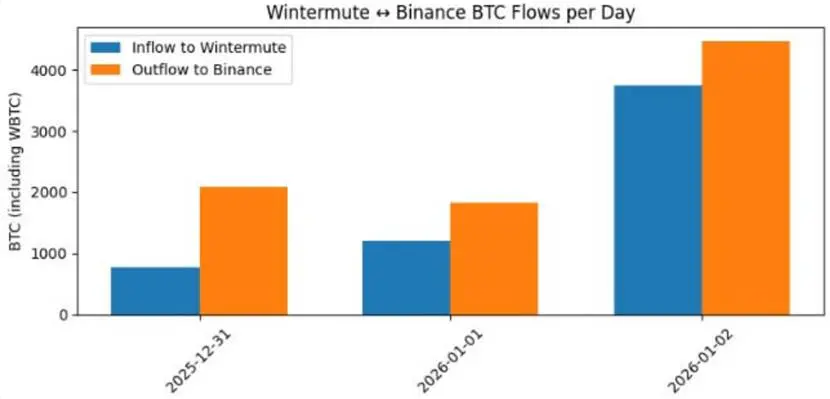

On New Year’s Eve, December 31st, Bitcoin’s price hovered around $92,000. On-chain monitoring data revealed that Wintermute made a net deposit of 1,213 BTC (worth approximately $107 million) into Binance that day.

The timing of these transfers coincided with the late-night rest period for European and American traders and the tail end of the Asian trading session—a widely recognized liquidity vacuum. Possibly impacted by this selling pressure, Bitcoin’s price quickly broke down, falling below the $90,000 mark.

For the following two days, Wintermute maintained a high frequency of net deposits. On January 1st and January 2nd, the institution net deposited approximately 624 BTC and 817 BTC into Binance, respectively.

Over just three days, it deposited a cumulative 4,709 BTC into Binance and withdrew 2,055 BTC, resulting in a staggering net deposit of 2,654 BTC. Concurrently, Bitcoin’s price accelerated its decline on January 2nd, touching a near-term low around $88,000.

This series of actions has once again plunged the market into questioning the role of market makers. Investors supporting the “manipulation theory” argue this is a precise hunt by institutions leveraging their technical advantages against retail traders.

Malicious Dumping or Routine Inventory Management?

In fact, this is far from the first time Wintermute has been caught in a whirlwind of controversy.

Looking at its historical track record, Wintermute’s capital movements have repeatedly appeared on the eve of major market shocks. For instance, on October 10, 2025, the crypto market experienced an epic-scale liquidation event amounting to $19 billion. Just hours before the crash, Wintermute was monitored transferring a massive $700 million in assets to exchanges.

Furthermore, from the SOL crash in September 2025 to the earlier governance proposal controversy surrounding Yearn Finance in 2023, this leading market maker has faced multiple accusations of “pump and dump.”

Regarding accusations of market manipulation, Wintermute and its supporters hold a starkly different position. The core point of contention lies in precisely defining the red line between “legitimate market making” and “malicious guidance.”

Critics argue that market makers deliberately choose illiquid holiday windows to inject spot assets, aiming to artificially create selling pressure and precisely trigger cascading stop-loss orders from retail long positions.

Leveraging deep partnerships with major exchanges and insights into market microstructure, market makers can easily create volatility during low-liquidity periods by placing large orders, profiting from the ensuing washout.

However, Wintermute CEO Evgeny Gaevoy dismisses this as “conspiracy theory.” He has emphasized in interviews that today’s market structure is incomparable to the period of the Three Arrows Capital and Alameda bankruptcies in 2022. The current system boasts higher transparency and more robust risk isolation mechanisms, with institutional capital movements primarily aimed at inventory adjustment or risk hedging.

Gaevoy stated that when severe imbalances occur between exchange buy and sell orders, market makers must transfer positions to maintain liquidity supply. While such actions may objectively amplify short-term volatility, the subjective intent is certainly not to harvest profits.

In reality, the persistent controversy stems from the crypto market’s lack of a universally accepted benchmark for judgment.

In traditional securities markets, using capital advantage for spoofing or deliberate price manipulation constitutes a clear criminal offense. But in the 24/7, highly algorithmic crypto world, how can one prove whether an institution’s large transfer is intended to stabilize the market or for arbitrage?

This absence of a definitive judgment framework leaves top market makers like Wintermute perpetually caught in a dilemma—viewed both as a cornerstone of market liquidity and as an undeniable “invisible hand.”

Menukarkans and some industry analysts tend to view market makers as a “necessary evil” within the market ecosystem. Without such major players providing two-sided quotes, cryptocurrency volatility could spiral out of control, potentially triggering systemic slippage disasters.

However, from the perspective of ordinary investors, institutions possess overwhelming advantages in capital, algorithms, and information. In an environment lacking rigid regulatory constraints, such advantages inevitably risk becoming tools for seeking undue profits.

The “Cyber Prisoner’s Dilemma” Spawned by Transparency

Beyond analyzing Wintermute’s micro-operations, this New Year controversy has actually exposed a long-standing, almost paradoxical contradiction in the crypto world: the absolute transparency we pursue is increasingly becoming a vulnerability in institutional games and a source of market noise.

In traditional finance, position adjustments, inventory management, and internal fund transfers by institutions like BlackRock or Goldman Sachs remain largely opaque to the outside world unless revealed in quarterly reports or regulatory disclosures.

But in the blockchain world, the veil of privacy has vanished.

The foundational principles of blockchain are openness and immutability, designed to prevent fraud and enable decentralization. However, as we’ve witnessed, every inflow and outflow from BlackRock’s ETF-related addresses, every transfer from Wintermute to Binance’s hot wallet, resembles a public performance in a transparent glass room.

Institutional giants must accept that their every operational move is parsed by monitoring tools into highly suggestive “dumping warnings” or “accumulation signals.”

Has this transparency truly brought fairness? The crypto world has long championed “equality before data,” but the reality is that this extreme transparency has instead fostered more misinterpretation and collective panic.

For retail investors, the internal matching engines and order book logic of institutions within CEXs are difficult to discern. They can often only infer outcomes from on-chain traces. Precisely due to this information asymmetry, any anomaly on-chain can be interpreted as a conspiracy, further exacerbating irrational market volatility.

Kesimpulan

When the entire market is fixated on the wallet addresses of BlackRock and Wintermute, what we are trading may no longer be the intrinsic value of Bitcoin itself, but rather suspicion and emotion.

The information gap is dead; the cognitive gap is eternal. For investors, although today’s market features more mature risk isolation and is no longer prone to chain-reaction implosions, the sense of powerlessness from “seeing the data but not the truth” seems never to have disappeared. Trading in the extreme, deep waters of crypto博弈 requires building an independent cognitive framework that penetrates surface-level volatility to find one’s own certainty.

Artikel ini bersumber dari internet: At the beginning of 2026, we were all set up by Wintermute

Related: Fed Rate Cut Expectations: Why Employment Data Isn’t a Key Factor

While news headlines often focus on whether the employment data “exceeded” or “fell short” expectations, this reporting style overlooks a more important point. Monetary policy is not based on a single data point. More importantly, the non-farm payroll report is just one of many factors considered in the Federal Reserve’s decision-making process, and it is not the most influential one. To understand what the data actually means for interest rate expectations, it’s helpful to look at the issue from a more macro perspective. Background of the latest non-farm payroll data Yesterday’s jobs report was not released monthly, but rather combined data from October and November due to a data gap caused by the US government shutdown in October. This alone means that the data needs to be interpreted with more…