Fed Rate Cut Expectations: Why Employment Data Isn’t a Key Factor

While news headlines often focus on whether the employment data “exceeded” or “fell short” expectations, this reporting style overlooks a more important point. Monetary policy is not based on a single data point. More importantly, the non-farm payroll report is just one of many factors considered in the Federal Reserve’s decision-making process, and it is not the most influential one.

To understand what the data actually means for interest rate expectations, it’s helpful to look at the issue from a more macro perspective.

Background of the latest non-farm payroll data

Yesterday’s jobs report was not released monthly, but rather combined data from October and November due to a data gap caused by the US government shutdown in October. This alone means that the data needs to be interpreted with more care than ever before.

Several details stand out.

First, the October employment data was revised significantly downward. Nonfarm payrolls fell by approximately 105,000 that month, a significant deterioration compared to previous estimates. However, shutdowns and production stoppages during the pandemic may have affected data collection and reporting, resulting in lower reliability of the October data compared to usual.

Secondly, 64,000 new jobs were added in November. While slightly higher than market expectations, the increase was far from robust. Meanwhile, the unemployment rate rose to 4.6%, a multi-year high, also exceeding widespread market expectations.

Third, new job creation remains highly concentrated. The majority of new jobs are in healthcare and construction, while growth in other sectors—particularly certain service sectors—is far less robust than in these two areas.

Overall, the report paints a picture of an economy that is still creating jobs, but with uneven and slowing growth.

What information does the data actually reveal about the labor market?

The most important significance of this report lies not in whether the final data exceeded expectations, but in the patterns behind the data.

The job market has clearly cooled, but it hasn’t collapsed. There is currently no evidence of mass layoffs or a sudden surge in unemployment claims. Instead, the labor market appears to be entering a phase of gradual weakening.

This dynamic is typical of economies transitioning from the late stages of a cyclical expansion to a slowdown. Businesses face rising costs—including wages, financing expenses, and input prices—while revenue prospects become uncertain. However, the current situation is not sufficient to justify large-scale layoffs.

Therefore, companies typically adopt a more moderate approach. Hiring slows, vacancies remain unfilled, pay raises become more difficult, and bonuses are reduced or even eliminated. These adjustments weaken the demand for labor but do not trigger a sudden employment shock.

Industry-specific data corroborates this view. Healthcare hiring remains robust, primarily driven by structural demand rather than cyclical growth. Construction hiring reflects the momentum of ongoing projects and infrastructure development, rather than an overall economic acceleration. The sluggish employment growth in non-essential services is particularly noteworthy.

From this perspective, a 4.6% unemployment rate is not worrying—but it does confirm that the labor market is gradually returning to a state of weakness.

Stagflation dynamics and policy tension

This jobs report is closely related to a broader macroeconomic theme: the increasing risk of stagflation.

On the one hand, inflationary pressures remain high. Business input costs remain high, and price stability has not yet fully recovered. Under normal circumstances, this would typically mean a need to tighten monetary policy.

On the other hand, economic growth momentum is weakening. Hiring is slowing, growth expectations are moderateing, and business confidence is weakening. These factors typically imply a need for easing financial conditions.

This tension explains the growing divisions within the Federal Reserve. Policymakers face a trade-off between controlling inflation and avoiding unnecessary economic damage. The latest jobs data has not resolved this dilemma; rather, it has confirmed it.

Importantly, this is precisely why the market interpreted the report as slightly positive for risk assets. It’s not because of strong job growth, but because the data supports the view that the economic slowdown is manageable rather than a hard landing.

Why does non-farm payroll data have a limited impact on interest rate cuts?

Although non-farm payrolls are closely watched, they are not the primary driver of interest rate decisions.

The Federal Open बाज़ार Committee (FOMC) meets approximately every six to seven weeks, for a total of eight meetings per year. In contrast, most macroeconomic indicators—including inflation and employment data—are released monthly. Therefore, the weight of any single data point is limited.

More importantly, the Federal Reserve assesses a range of indicators. While employment is important, it is not the most critical factor in deciding on interest rate cuts.

From a policy perspective, the relative importance of key indicators is usually ranked in the following order:

- Personal consumption expenditure (PCE) inflation

- Consumer Price Index (CPI)

- Non-farm payrolls

- Weekly initial jobless claims

- Purchasing Managers’ Index (PMI)

- Quarterly GDP

Besides GDP, all these indicators are released monthly. They often send conflicting signals. Overemphasizing any one of them—especially wage data—can lead to misleading conclusions.

This is why trying to predict interest rate cuts based on a jobs report often leads to disappointment.

The real driving factor: the path of interest rate cuts, not the meeting itself.

One of the most common mistakes investors make is treating each Federal Open Market Committee (FOMC) meeting as an isolated event. In reality, the market is more focused on the direction of policy than on the outcome of any single meeting.

A one-off rate cut is largely meaningless if there are no subsequent easing policies. Conversely, even without an immediate rate cut, expectations of future easing cycles will significantly impact asset prices—especially in the क्रिप्टोमुद्रा बाज़ार।

Therefore, while employment data is important, it is secondary. It helps to construct a broader narrative, but rarely determines policy independently.

Ultimately, the key question is whether inflation will continue to slow as economic growth slows to a level sufficient to support continued loose monetary policy. Determining this requires months of data, not just a single set of figures.

Let the market play its greatest role

Another point that is often overlooked is that individual investors do not need to replicate the work of professional macro trading departments.

The market is not driven by isolated opinions or social media comments, but rather by the collective expectations of institutions managing trillions of dollars in assets, backed by teams of economists, strategists, and data analysts.

Instead of manually weighing each data point, it is often more effective to observe the convergence of these expected outcomes.

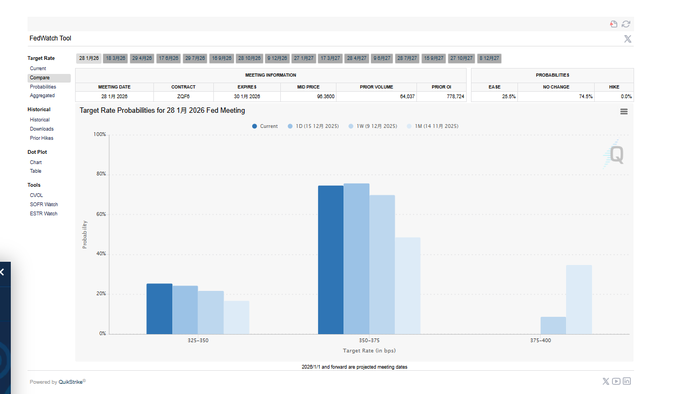

This is where tools like CME FedWatch become very valuable.

Track interest rate expectations using CME Fedwatch

The CME FedWatch tool aggregates real-time pricing of interest rate futures to estimate the probability distribution of market reactions to an upcoming decision by the Federal Reserve.

Instead of speculating whether the Federal Reserve will cut interest rates and by how much, investors should look at how the market positions itself.

The tool also allows users to track changes in expectations over time, providing insights into whether emotions shift gradually or react to short-term noise.

For anyone looking to understand interest rate expectations, this approach is more effective and reliable than reacting to individual data releases.

This tool can be obtained here:

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

See beyond appearances to the essence

The latest nonfarm payrolls report has achieved its intended purpose: it confirms an existing trend rather than creating a new one.

Job growth has slowed, but not collapsed. Inflationary pressures persist, but economic growth is weakening. Policy trade-offs have become more complex, not simpler.

In this context, making investment decisions based on just one month’s employment data is not very meaningful. It is more important to focus on the long-term interplay between inflation, economic growth, and policy expectations.

For investors willing to step back, use the right tools, and focus on policy direction rather than news headlines, the signals are far clearer than the noise suggests.

The above viewpoints are all referenced from @Web3___Ace

यह लेख इंटरनेट से लिया गया है: Fed Rate Cut Expectations: Why Employment Data Isn’t a Key Factor

Compiled by Odaily Planet Daily ( @OdailyChina ); Translated by Azuma ( @azuma_eth ) On Wednesday night of the mission, U.S. Space Force Captain Gordon McCulloh was sitting in a military propeller plane, hovering in the calm, dim night sky of New Mexico, when his squadron’s group chat suddenly erupted. The squadron members—some on the ground, some in the air—are collecting data related to electromagnetic warfare while also keeping their investments in mind. Google’s stock price just surged in after-hours trading. Upon landing, McCulloh saw the messages: a ground officer posted a screenshot of a news article; another replied, “To the moon.” This day was becoming exceptionally lucrative for McCulloh and his brothers. The U.S. military may be the world’s most lethal “investment club,” and they are making a fortune…